Expert View

19 Jan 2025

Open letter to climate and energy transition leaders

One CEO’s outlook on what we need to do, together

Expert View By Private: Scott Jacobs

The last three years have made for a crucible moment in the energy transition. The transition has seen incredible momentum, propelled by large capital commitments over the last decade, historic policy support and tons of steel in the ground in projects around the world generating energy from clean sources. Now, we’re entering a new year and era, and the current macro environment has its fair share of challenges. How entrepreneurs and investors respond to this moment will determine their viability and separate the best from the rest.

Looking for clues for how the macro environment is affecting “climate tech” is often not an effective way to understand where we are in the transition to a decarbonized industrial economy. There are, however, several macro factors that make this a tough environment to build things. When the environment is tough for building everything, it’s particularly tough for building newer things. And the energy transition depends on building new things.

These macro factors include:

- Interest rates: Grew from near zero in 2021 to ~5% in 2024; sticky inflation likely to prevent further cuts

- Investor pullback: Over 75% decline in climate tech investing from 2021-2023. Later stage and proven parts of the ecosystem are faring better.

- Policy uncertainty: US elections, major changes in governments of most of the G7

- Geopolitical strife: Conflicts in the Middle East, Ukraine, and threats in Asia disrupt energy markets and global supply chains

- Bad news: Persistently negative and worsening news cycle on climate and climate tech

- Inflation: Reached >8% levels in 2022 in many countries; supply chains disrupted by pandemic

Unlike conventional, fossil-based infrastructure, the sustainable infrastructure sector can’t wait for cycles to come back. Instead, we need to outcompete the alternatives by building strong businesses able to withstand our industry’s continued uncertainty. Inertia favors incumbents, so we need to be even better than the current solutions to win. While there is certainly cause for concern, in the face of these challenges, good deals and good investments will find capital.

Ahead of my trip to Davos, I’ve reflected on a few ideas that I believe help illuminate what these macro factors mean for the sustainable infrastructure sector and how our sectors’ leaders can respond. As a (recovering) management consultant, I’ve naturally put these in PowerPoint form. For my full deck, click here.

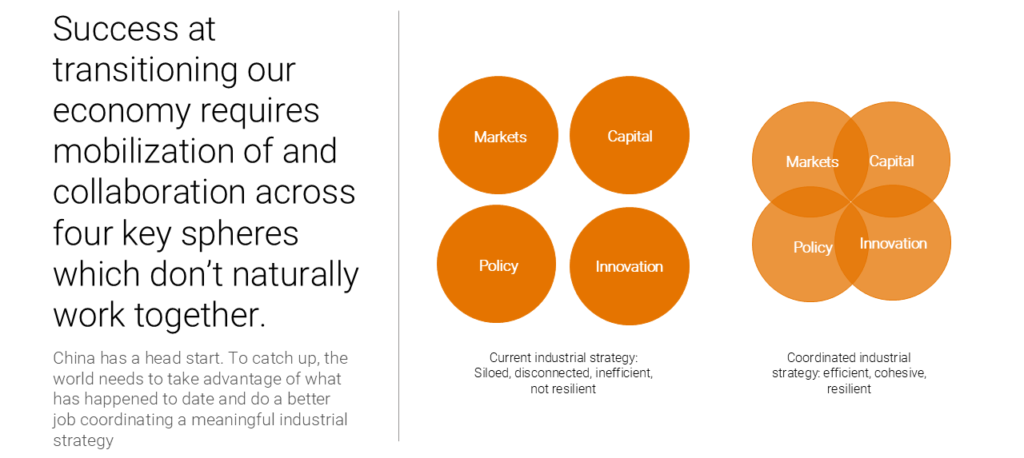

1) Success depends on mobilizing and collaborating across four key spheres: We cannot transition our economy with siloed markets, capital, policy, and innovation landscapes. These spheres don’t naturally work together and that lack of coordination leads to incumbents having a leg up. The only way we manage through the chaos of this time and continue to build the resource revolution is to build a productive industrial strategy by better coordinating these critical economic forces.

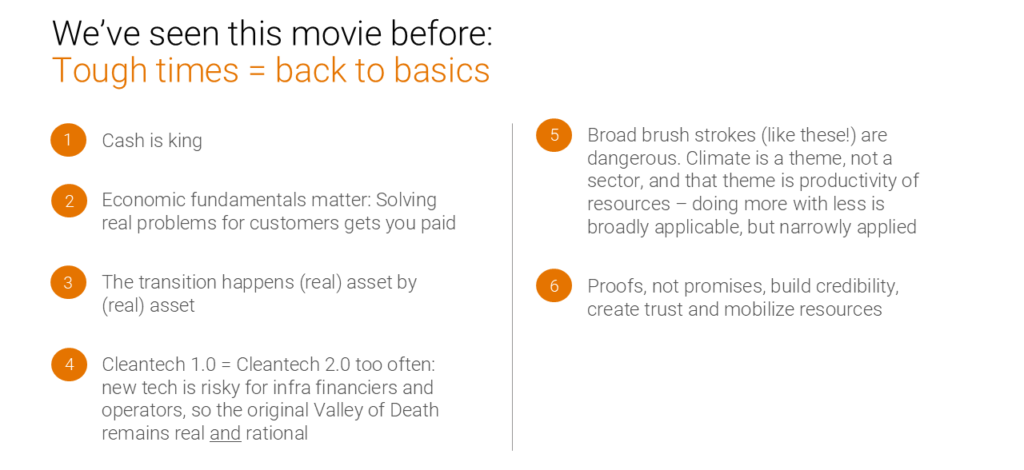

2) What’s always been good is still what’s good: The recipe for building and funding successful companies is simple, clear, and consistent. It’s the first lesson in every course in business school. However, “back to basics” principles get obscured when money is easy to come by, and they feel difficult when money is not easy to come by.

Leaders in the infrastructure transition must do what it takes to return to these principles to be successful in this moment. This is no small task. It requires discipline and relentless commitment to foundational truths that eliminate unneeded risk and make things easy for investors.

3) Diamonds are more common when you look for the right things: There will continue to be more success stories, even in today’s more challenging market. Like in previous cycles, winners will emerge from the wreckage. Some will even dominate trillion-dollar sectors. They’ll do so by using the uncertainty of this moment to focus on how to scale. We may see new technologies emerge, but we have so much of what we need. Discipline means taking those things, getting the businesses right, and focusing on growing smart more than growing fast.

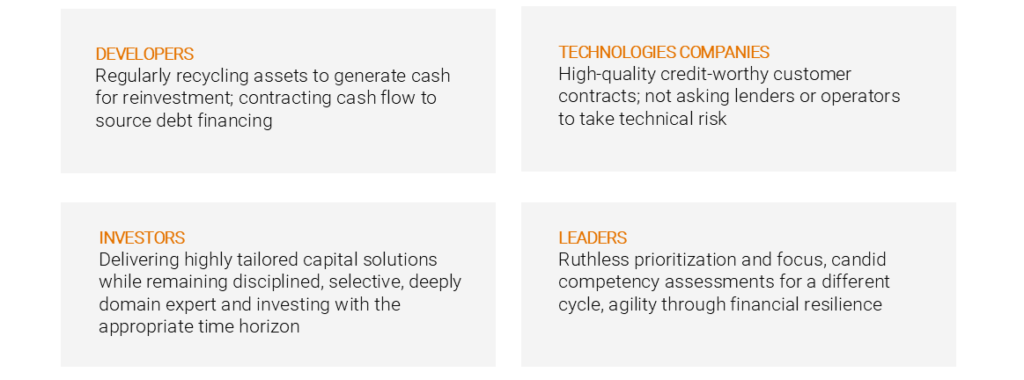

4) Resolve to the best in every necessary category: Challenging macro situations favor the companies that can solve problems most effectively for customers while being economic for investors. The best developers, technologists, investors, and company leaders have already found a way to pivot to ensure they can continue to prioritize what matters most. They did so through resilience, focus, and preparation.

My Generate team and I are committed to translating these insights into action. In the last year we announced our $1.5 billion equity fundraise and our $1.2 billion corporate credit facility. We’ve upheld our central mission to put customers first, helping finance and deploy community solar solutions for the state of New York (link), financing onsite power solutions that allowed Texas grocery stores to keep their lights on during Hurricane Beryl (link), and establishing our joint venture with Blue Bird to help school districts across the US purchase and operate electric school bus fleets (link), among other recent projects. As we enter the new year, we’ve renewed our commitment to discipline and to strategic and tactical planning. We will continue to work with our capital and operational partners towards our common cause of advancing the energy transition. As we say around Generate, no one crosses the finish line alone. It will take all of us… and more.

More insights

High Stakes at CERAWeek

It is not often - read "never" - that a CEO's decision NOT to attend a conference is a global headline but so it was this weekend when Amin Nasser, the veteran CEO of Saudi Aramco, withdrew from CERAWeek in order to attend to matters closer to home. Mr. Nasser's withdrawal underlines that the focus for all of us still heading to Houston will be on the Straits of Hormuz and its short, medium and long term consequences on gasoline prices. And all the while, the focus on high gasoline prices at CERA this week is likely to obscure the other energy price shock lurking in the shadows which is the inexorable rise of electricity prices across the United States. Unlike gasoline prices, once retail electricity prices rise, they almost never go down.

Read moreIndustrial Decarbonization: How Thermal Storage Can Electrify Heat at Scale

Investment in thermal energy storage has accelerated in recent years as technical progress and customer demand have improved project bankability. Since 2020, sector funding has grown and shifted toward later-stage investors, reflecting greater confidence in TES’s readiness for commercial deployment.

Read moreConsolidation: The Pathway to Enduring Impact

It is easy to be disoriented by the swing from exuberance to pessimism that has defined the clean energy sector in recent years. Yet these moments are precisely when opportunity is greatest. Beneath the headlines are clear indicators of tremendous potential in the U.S. energy transition. The challenge is to separate fundamentals from sentiment, to acknowledge and fix the mistakes that we have made, and to chart a path to scale rooted in discipline, operational excellence, and commercial reality.

Read more