Expert View

30 Apr 2025

Investing in U.S. infrastructure for a decade of demand

Like many across the industry, Generate’s teams are busy navigating the immediate challenges posed by economy-wide tariffs that are wide-ranging in both likelihood and potential impact.

Expert View By Logan Goldie-Scot

Despite the near-term uncertainty, the fundamentals of the U.S. infrastructure and energy markets remain attractive for long-term investors. Structural tailwinds such as the need to replace ageing infrastructure, generational load growth, and compelling economics define the landscape. In this environment, renewable energy, distributed generation, and energy storage are essential solutions. For investors focused on long-term value creation, the current environment presents an opportunity to lean in, not pull back.

An ageing system in need of investment

The U.S. power sector is grappling with decades of underinvestment. In its 2025 Report Card, the American Society of Civil Engineers estimates that bringing U.S. infrastructure to a state of good repair – up from a C to B grade – would require $9.1 trillion in investment from 2024 to 2033 (link). The U.S. energy sector is in particular need of investment and received a lowly D+. Some 300GW of operating U.S. generation assets, roughly a quarter of the total, are over 40 years old and will need to be replaced in the coming years. Indeed, 43GW of coal and gas is scheduled to retire by 2028.

Load growth is real, and durable

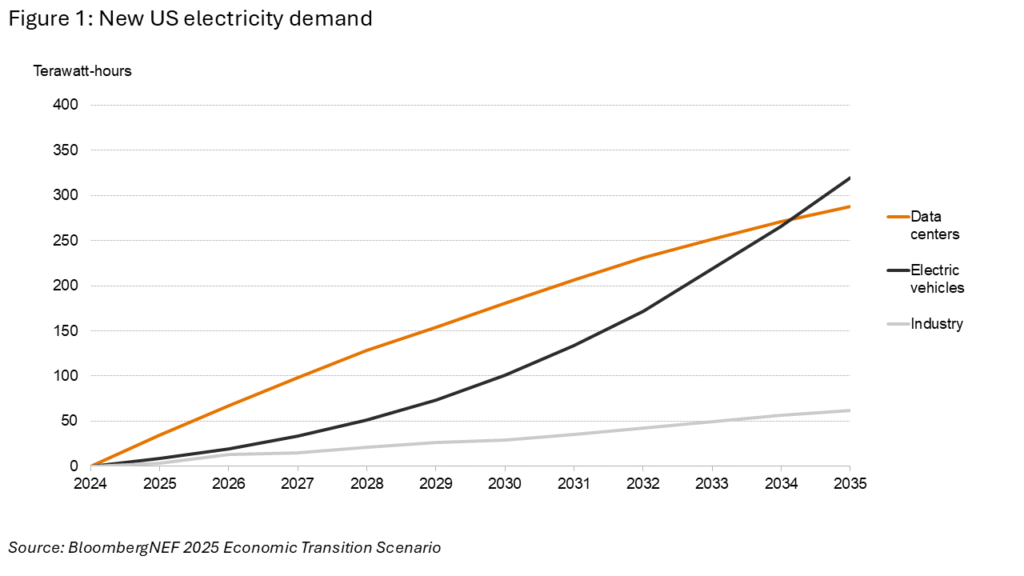

On top of this, U.S. electricity demand is growing at a pace not seen since the 1980s. Data centers form the bedrock of this demand but manufacturing, electric vehicles (EVs), and broader electrification play important supporting acts over the next 10 years (Figure 1). This growth is resilient to a slowdown in the broader U.S. economy, as major technology firms push forward with multi-billion-dollar investments in data centers and AI infrastructure. Of lower impact, but directionally aligned, EV uptake is holding up. Nearly 300,000 new EVs were sold in the first quarter of 2025 in the U.S., according to the latest report from Kelley Blue Book, an increase of 11.4% year over year.

Only solar and storage can meet this demand

There is no near- to medium-term way to meet this demand growth without renewable energy and battery storage. Wind, solar, and storage made up 94% of electricity generation capacity additions in 2024 for a reason. They are the fastest technologies to deploy, they are cost competitive, and they shield buyers from natural gas prices.

The U.S. power system is more distributed than ever: 66% of completed U.S. power, renewables, and environment transactions from 2020 to 2024 were under $300 million in size. Distributed generation assets are also protected, and even benefit, from rising capacity prices since part of their compensation typically includes generating bill credits equivalent to the local utility’s residential or small commercial supply rate.

Let’s run through the alternatives. Gas will continue to play an important role in the U.S. energy system. Nonetheless, it is becoming more expensive, plants are taking longer to build, and they have relatively poor interconnection queue positions. NextEra data shows the price of combined cycle gas turbine (CCGT) to be delivered in 2030 has risen to $2,600-2,800 per kW, more than three times the price in 2018. Furthermore, new gas pipelines have their own development and construction challenges to deal with.

Beyond gas, it’s necessary to see the signal through the noise. More geothermal and advanced nuclear is cause for excitement, and only strengthens the hand of decarbonization, but we should be mindful of their relative scale. The Department of Energy estimates that between 2-5GW of geothermal could come online by 2030. While great news, it pales in near-term significance to BloombergNEF’s estimated 587GW of wind, solar, and energy storage capacity additions forecast between 2025-30. Similarly, advanced nuclear is a story for the 2030s, not this decade.

In today’s discourse, technology decisions – like many others – are often reduced to overly simplistic, binary choices. Renewables versus fossil, centralized versus distributed, etc. But real-world power system modeling and build is both more complex and the results more nuanced. Again and again, these models show that a mix of high renewable energy penetration, battery storage, and natural gas delivers the lowest overall system costs. The underlying economics are clear: clean power is inevitable. Decarbonize power, electrify the economy.

Investing through volatility

At times like these, it’s important to be clear about what is certain and which decisions must be made even in the face of uncertainty. The science of climate change and resource scarcity remains solid and continues to be re-validated. Customer demand for electricity and for many energy transition solutions remains strong and growing. Diversity is an important risk mitigation tool. Infrastructure investments can be a source of stability and a hedge against inflation: the revenue infrastructure generates, such as from utility payments, typically rises in line with or above inflation. Now is the time for investors with conviction in the above statements, and capital, to lean in.

This note began as a slide deck. To see the underlying slides, click here.

More insights

Communities Have More Leverage Over the AI Buildout Than They Realize

Communities are skeptical of data centers. They don’t know if they like the underlying technology, they certainly are not feeling the increase in power costs they attribute to this massive build, and they don’t feel like they need to provide tax assistance to the richest companies in the world. The companies needing to build are organizing fast through procurement standards, model legislation, financing structures, and political infrastructure to make sure their interests are represented at every level where decisions get made. Advocates need to help communities benefit from this moment, not be a reflexive “no” and convince communities they have nothing to gain. It isn’t true and it won’t help the people climate, environmental, and community organizing groups claim to represent. Communities that organize with equal seriousness, around what they want from this buildout rather than around whether they want it at all, will end the decade with infrastructure their grandchildren still benefit from. That infrastructure can be clean, affordable, and reliable. Communities that spend the leverage on saying no will get what they always have: whatever is left over after capital sets the terms. Developers that try to undercut productive efforts to build that kind of resilience in communities will end up losing. Both sides need to realize that the relationship can be productive and valuable.

Read moreHigh Stakes at CERAWeek

It is not often - read "never" - that a CEO's decision NOT to attend a conference is a global headline but so it was this weekend when Amin Nasser, the veteran CEO of Saudi Aramco, withdrew from CERAWeek in order to attend to matters closer to home. Mr. Nasser's withdrawal underlines that the focus for all of us still heading to Houston will be on the Straits of Hormuz and its short, medium and long term consequences on gasoline prices. And all the while, the focus on high gasoline prices at CERA this week is likely to obscure the other energy price shock lurking in the shadows which is the inexorable rise of electricity prices across the United States. Unlike gasoline prices, once retail electricity prices rise, they almost never go down.

Read moreIndustrial Decarbonization: How Thermal Storage Can Electrify Heat at Scale

Investment in thermal energy storage has accelerated in recent years as technical progress and customer demand have improved project bankability. Since 2020, sector funding has grown and shifted toward later-stage investors, reflecting greater confidence in TES’s readiness for commercial deployment.

Read more