Policy note

What the Senate’s reconciliation bill means for clean power

On Tuesday, the U.S. Senate passed a version of the reconciliation bill that is now on its way to final passage in the House. While the bill does not include some of the most onerous proposals that were circulating in the last hours, it still represents a significant shift in how renewables will be financed. The bottom line is that the Senate text will lead the U.S. to build less clean power, it will be more expensive, and power prices will rise. The grid will be less reliable, possibly leading to power shortages and blackouts for American households and businesses.

There’s still much that we do not know, and the required guidance on this front could take months for the U.S. Treasury to develop. Despite the challenges, the bill offers a path forward to safe harbor equipment over the coming year, to work with suppliers on sourcing strategies, with customers on offtake, and to provide flexible capital to partners who need it. The diversity of Generate’s portfolio is helpful here: while wind and solar generation took a huge hit, other important technologies fared better. Power scarcity and rising prices make microgrids and energy efficiency more attractive to customers, with the return of the ITC for fuel cells providing another boost. Battery storage retains the full tax credit through to 2033 and phases out fully by 2036. Technologies such as geothermal and nuclear similarly have a longer runway and we’re eager to help them scale.

One of the most promising pieces of the bill is the treatment of dairy waste as a source of energy. The Senate version extended deadlines where tax incentives could be claimed to turn manure into Renewable Natural Gas (RNG). That extension, plus clear language directing the Treasury department to recognize the contribution that RNG plays in reducing methane when pricing the credit, gives American farmers a meaningful chance to participate in domestic energy development.

The negative effects of the bill will not take long to show up for voters. Repealing clean energy technology-neutral tax credits could raise average U.S. residential electricity prices by nearly 7% by 2026, and by 10% for U.S. businesses according to a report from the Clean Energy Buyers Association. Reliability will drop: a Goldman Sachs June 2025 scenario shows that U.S. reserve margins could be near zero by 2029, and increasingly negative thereafter if renewable energy installations cease from 2028 onwards. And more projects that were going to be constructed will be cancelled. The North America Building Trades Union estimates that the bill threatens 1.75 million construction jobs and $148 billion in lost annual wages and benefits. Other leading trade unions such as the International Brotherhood of Electrical Workers (IBEW) issued similar warnings.

While the Tip O’Neil foundational political adage that “all politics is local” is often obscured in the age of social media and global information flows, at its core, it’s right. Access to affordable, reliable power and well-paying jobs (alongside healthcare and other core measures) has consistently remained high on voters’ priorities. Ultimately the impact of the bill will be to move decisions down the federal chain from Congress to states, counties, and cities. Because economies run on power, because voters care about their power bills, and there is no alternative. Projects are built locally, and state and local governments have a much closer relationship with the impacts on communities than Congress does. They are the first to experience power price shocks and the impacts of cancelled projects. They are less likely to frame policy making decisions in the generalities of “climate change” and more likely to anchor those decisions on the economic and social realities of their constituents.

Local officials have an opportunity here to provide the certainty that has evaded Congress. Investors crave certainty. The whiplash of drastic policy changes to the core tax provisions that help finance physical infrastructure make future U.S. investment decisions across all asset classes and sectors more difficult. Budgets are tight and we cannot expect states and local communities to fully make up for the lost financial support. We need these policymakers to focus on minimizing the friction in the system that prevents clean energy technologies from scaling even quicker, despite being cheaper.

Generate and many of our peers have a strong record of working with local regulators and communities to put steel in the ground. There are programs that can help attract investment and those should be pursued with long-term certainty. Across the country, many market policies and designs are not optimized for the modern energy system Americans need. Efforts exist such as through the Regulatory Assistance Project or PowerLines to modernize our utility regulatory system, but more support is required. Regions that creatively and quickly solve these challenges will in return attract projects and investment and mitigate the worst outcomes of Congress’ actions. Remove this friction and the underlying fundamentals of our industry will speak for themselves.

A decade ago, the industry may have withered in the face of this assault. Today, the lack of available, scalable, and cost-competitive alternatives will ensure that investment in clean energy technologies continues, even if the economics and deal structures change. A decade ago, the goal was to bring these technologies down the cost curve. Today the focus must be to remove the friction on the ground. There are cost savings to be found across the industry as federal support winds down. A single-minded focus on delivering affordability and reliability will make the sector more efficient, more scalable, and more investable. It will reset the terms of the energy transition in a way that is ultimately impossible for policymakers to dispute.

By the numbers

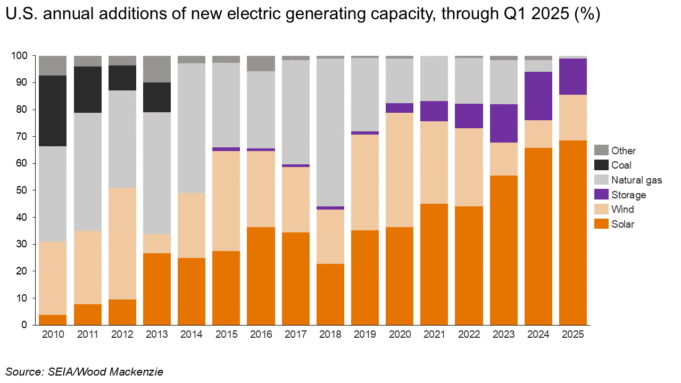

U.S. solar market shows its worth, again

U.S. solar installations totaled 10.8 GWdc in Q1 2025, the fourth largest U.S. quarterly installation number on record (SEIA). Solar accounted for nearly 70% of capacity added to the U.S. electricity grid in Q1, with wind and storage the bulk of the remainder. Hamstringing these industries makes it harder to keep pace with power demand and to maintain a reliable grid with affordable power.

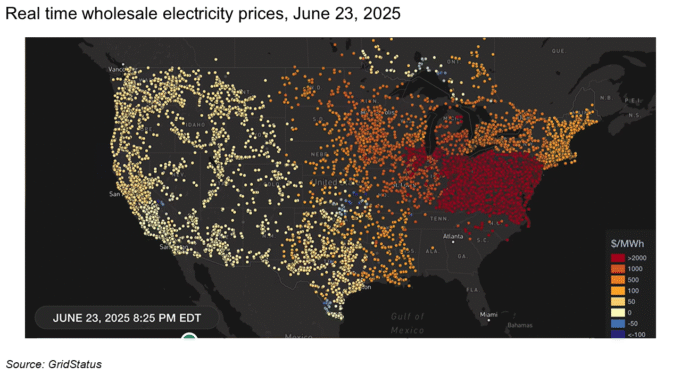

Record temperatures, record power consumption

Data centers are not the only driver behind rising U.S. power demand. A heat dome brought sweltering temperatures to the eastern half of the U.S. last week, and with it rising power demand and prices. PJM, NYISO, ISO-NE, and IESO exceeded last summer’s peak demand, and did so before July. See Grid Status’ time lapse of real-time electricity prices throughout the 72-hour heat wave (link).

Policy changes take toll on U.S. EV market forecast

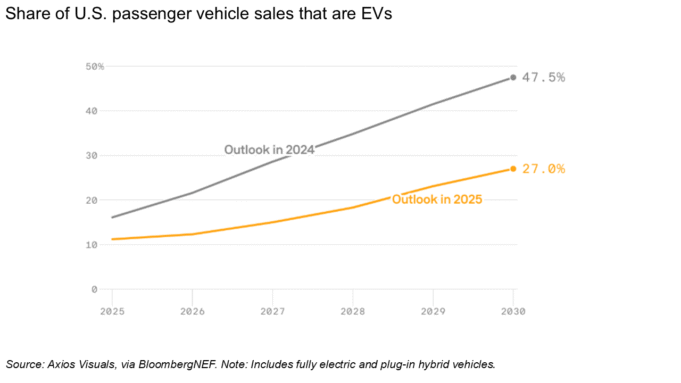

As written, the budget reconciliation bill will materially and negatively affect many industries beyond power, including mobility. Recent challenges from the Trump administration and U.S. Supreme Court to California’s vehicle emissions policies will dampen U.S. EV sales significantly (PoliticoPro 🔒, Axios). Amid these headwinds, BloombergNEF released a new outlook that sharply slashes its 2024 forecast for EVs’ share of U.S. car sales by 2030, dropping its prediction from 48% to 27% (BNEF).

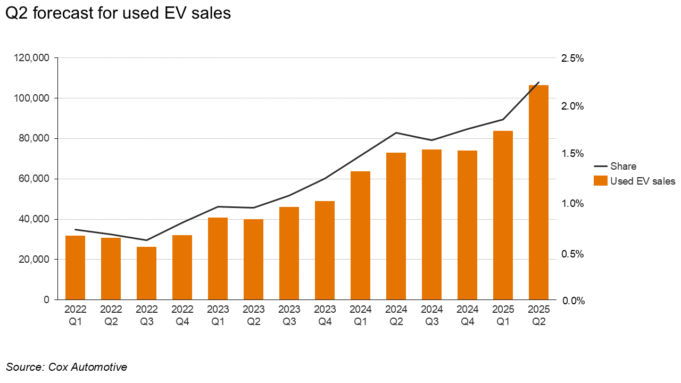

The report also shows how this slowdown puts the U.S. on a remarkably different trajectory to the EU and China. BNEF expects almost 22 million passenger EV sales this year, up 25% from 2024. China accounts for nearly two-thirds of those sales, followed by Europe with 17% and the U.S. with just 7%. U.S. sales will remain flat this year, in line with Cox Automotive’s mid-year review findings (link), but there remains grounds for optimism. The mid-year report tracks 75 electric models in the U.S. in 2025, up from just 17 in 2020. Additionally, model prices are falling, and Q2 was a record quarter for used EV sales. A healthy global EV market makes it possible, even likely, that U.S. sales could swiftly accelerate once more favorable conditions exist domestically.

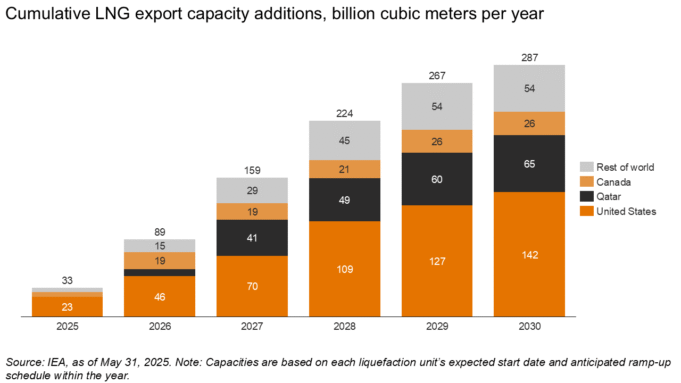

U.S. LNG capacity continues to rise

More capacity is set to be added to global LNG markets in the next five years than ever before. The current LNG export capacity is 670 billion cubic meters, and the IEA forecasts cumulative LNG capacity additions per year will reach nearly 300 billion cubic meters by 2030 (IEA). (Updated July 7 to clarify we were referring to export capacity and not current market.)

If production remains equal, scaling the U.S.’s natural gas export capacity will push up U.S. gas prices, since it will tie U.S. gas prices to structurally higher global prices (Energy Flux 🔒). Gas power plants set the marginal cost of electricity in many U.S. markets so this would further push up U.S. power prices. The Trump administration appears intent to tie America’s power system to natural gas. This will end poorly for consumers and businesses, and perhaps also for LNG exporters (Powering the Planet).

U.S. trade still affected from tariffs overhang

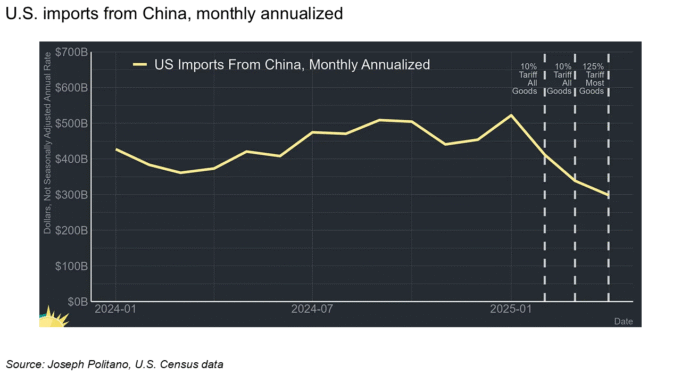

Though trade conditions have improved since the height of President Trump’s Liberation Day tariffs in April and the bulk of U.S./China tariffs remain paused, the U.S. is still operating in a tariff-uncertain environment. Trump doubled tariffs on steel and aluminum imports to the U.S. in June from 25% to 50% (BBC), and overall tariffs remain 7x higher than last year. Data from May shows China’s overall exports hit a three-month low (Reuters). U.S. imports from China fell 40% from January to April 2025, their lowest level since March 2020 (Apricitas Economics).

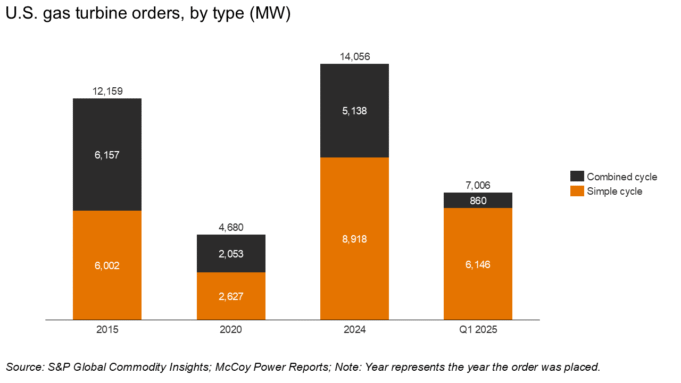

Gas and renewables trade roles

Trends in gas turbine orders illustrate how renewables have increasingly taken on a leading role in the U.S. power system. Nearly 90% of the gas turbine capacity ordered in Q1 2025 was for simple-cycle turbines, or peakers, which are designed to supplement the power grid during periods of peak demand. Where renewables were once supporting power sources, gas is now being used as a near-term supplement for a renewables-forward grid. Yet another example of how the reconciliation bill’s attacks on wind and solar are at odds with the present U.S. power system.

What we're reading

A new normal: The coming era of sustained, high capacity pricing (link)

Expected surge in turbine manufacturing complicated by rising costs, uncertain demand (link)

Grid costs are power law distributed (link)

ERCOT’s 4CP program is a bellwether for the shifting face of electricity demand and grid services (link)

Who should pay to keep Michigan coal plant running past its retirement date? (link)

Cox Automotive’s mid-year review (link)

Wind and solar: A parasite to the grid? (link)

It’s time for Abundance to get mad (link)

Charting out the new grand bargain for permitting reform (link)

Pew Center’s “Americans’ Views on Energy” poll (link)

More newsletters

June 2026 Newsletter - AGM Edition

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

Read moreApril 2026 Newsletter

After four years, PJM opened back up its generation interconnection queue. Gas is now the dominant technology in the queue compared to solar back in 2022.

Read moreMarch 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read more