Reflections from Climate Week

The community of investors, policy makers, energy professionals, buyers, and advocates trying to accelerate the transition have had a very busy few weeks. Starting under the hot sun and bright lights of Vegas, RE+ is the renewable industry’s annual trade, bringing together tens of thousands of industry professionals to golf, learn, deal and lament the state of the industry. Last week was Climate Week, the annual pilgrimage to New York City, held in conjunction with the UN General Assembly, that is a more investment and policy-oriented affair with many of the same players. We were at both and have some thoughts on the current vibes.

There is no shortage of optimism or of pessimism. In fact, whatever mirror you brought to these events was probably what you saw reflected. Pessimistic takes included the belief that the heyday is behind us, that capital is difficult to access, and that policy is shifting the tide away from transition technologies. The optimistists focused on the undeniable sense that the macro trends in the market now are so indelible that they will be an even more powerful force to counter the headwinds.

It’s a tension we’ve explored in depth in recent pieces (August, July, America Power at a Crossroads). As Jefferies’ Aniket Shah put it: update your priors. The numbers show the answer is somewhere in between. Annual U.S. energy transition investment stalled in 2024, and private and public capital is now retreating from the market. At the same time, customer demand, underlying prices and revenues, and the value of the underlying assets are growing.

As our new CEO said in a piece he wrote for Climate Week, the winners in this phase of the transition will recognize some of these trends and figure out how to operate, invest, and build through them.

We have seen this movie before and while it may feel new for our industry, these cycles have established a playbook for success. There will be consolidation, and from that consolidation will come strength. Investors need three skills to succeed: operational expertise, financing experience, and market understanding.

A recurring theme across both events was apprehension about access to capital. Some of the smartest conversations were focused on how capital could be formed to take advantage of the moment.

Equity alone can’t finance the trillions required. There isn’t enough, and it’s too expensive. Private credit provides structure, discipline, and the path to bankability. Our recent $100 million credit line to Soluna is a recent example (link).

Global energy transition investment totaled roughly $2.1 trillion in 2024 but needs to increase to roughly $8 trillion annually to achieve climate goals. Scale will come from crowding in institutional capital. The biggest pool of capital sits with insurance companies, pension plans and sovereign wealth funds. These companies are currently often limited in the scale they can invest in sustainable infrastructure assets, largely because they are limited to investing in investment grade credit. The industry must find a way to unlock this.

By the numbers

Who to blame for your electricity bill?

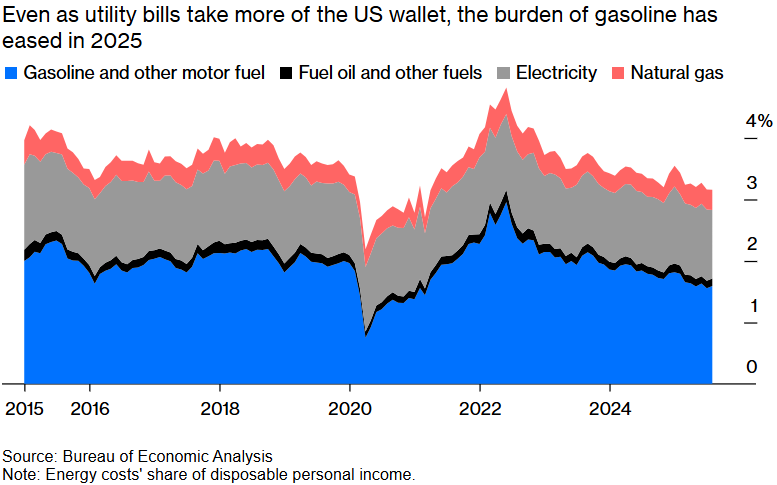

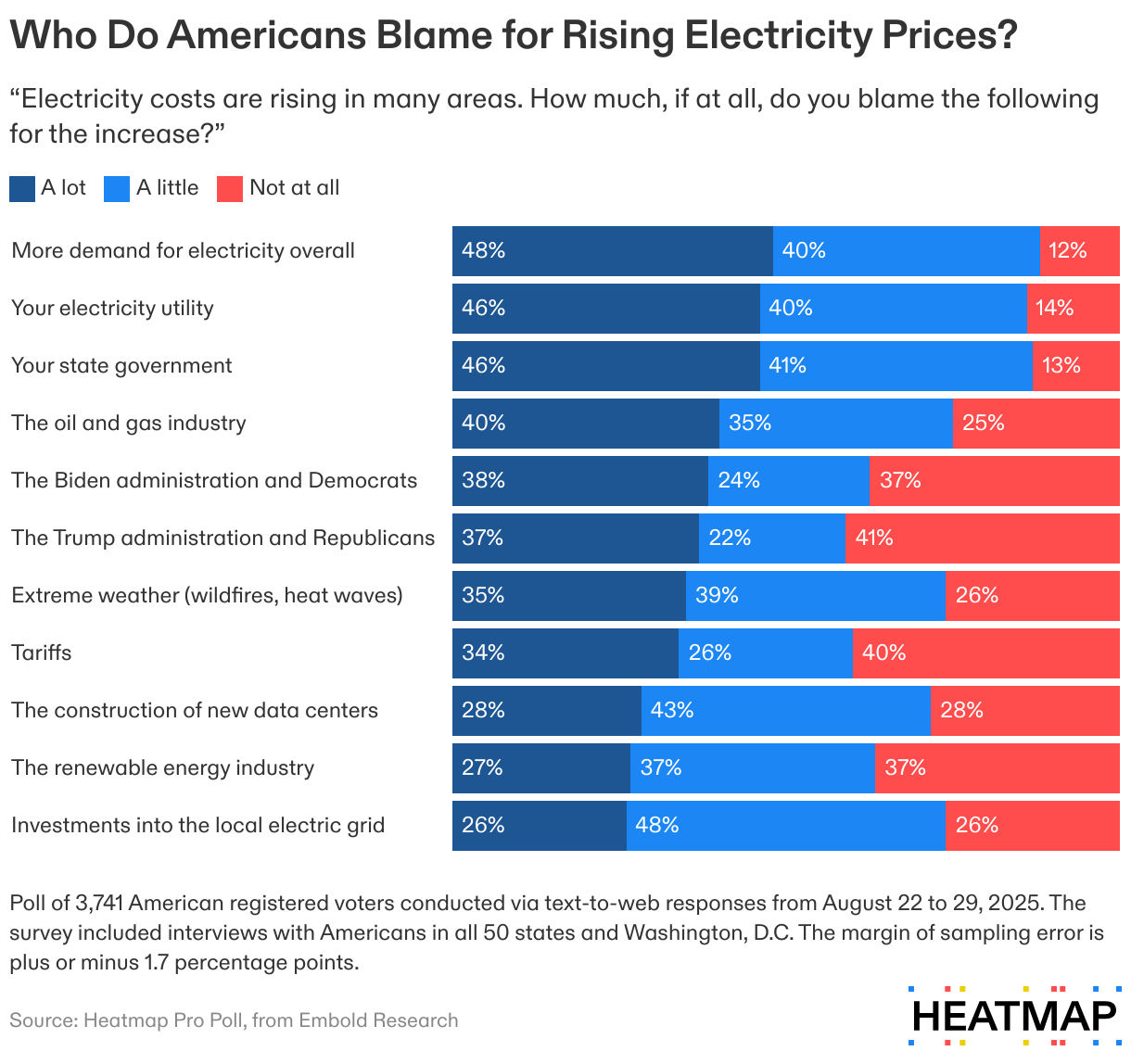

Cost of living concerns, in particular electricity prices, are front of mind for many U.S. voters but two issues make it a harder line of attack for Democrats. For starters, the average gasoline price is down 10% in real terms in 2025, which makes up for recent electricity price increases (Bloomberg). Secondly, voters don’t yet pin the fault for high electricity prices on Washington, D.C. (Heatmap). On a lighter note, and h/t to Bantam, this TikTok of a Texas man waxing Faulkneresque about his electricity bill is a gem (link).

A cool Texas summer

Peak demand has not reached 2023 or 2024 levels in ERCOT this year. Consumption however is higher in every single month this year compared to 2024 despite the less extreme heat this summer (Aurora Energy Research). This summer will likely end up in the top 25% for heat: far hotter than the average of the last 150 years or so, but far less hot than the last four summers which were all in the top 5% (link).

The ups and downs of flexible load

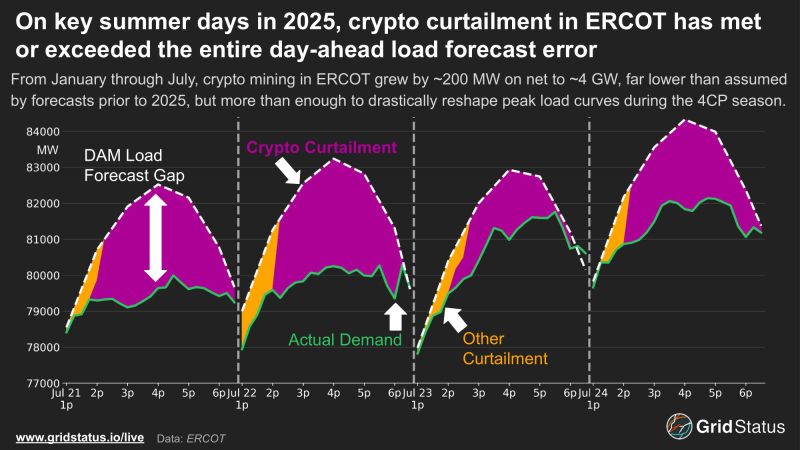

Staying in Texas, extremely flexible data center demand was also a major contributor to ERCOT’s flat peak load curve (link, chart below). Take a look at our Expert View on flexible data centers from earlier this month (link).

The approach to managing load is changing across the U.S. Some markets may incentivize load flexibility, while others may simply require it. This can prove controversial, as responses to PJM’s Non-Capacity-Backed-Load proposal shows (link, link, link). In response (and just sneaking into this newsletter), Amazon, Calpine, Constellation, Google, Microsoft and Talen floated a new proposal to address PJM’s capacity shortfalls on October 1 (link, h/t Tyler Norris)

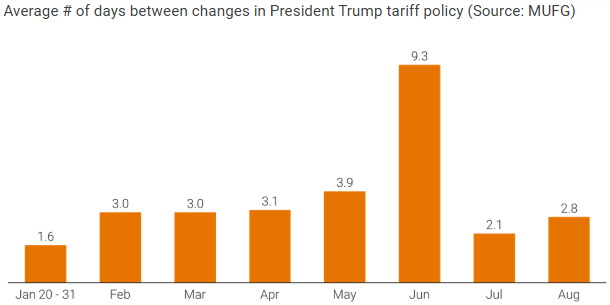

At several events this past month, I heard that data-center builders will prioritize construction outside the United States if current challenges to building here persist. This underestimates the U.S.’ resilience and dominance. Despite recent price hikes, U.S. electricity remains comparatively affordable; geopolitical risks and trade frictions are rising, complicating outsourcing overseas; and the U.S. now benefits from an unrivaled ecosystem of skilled labor, a well-developed supply chain, financing, and a dense customer base that is hard for other countries to replicate. Other markets also face many of the same challenges. Image courtesy of MUFG.

Mixed signals for natural gas

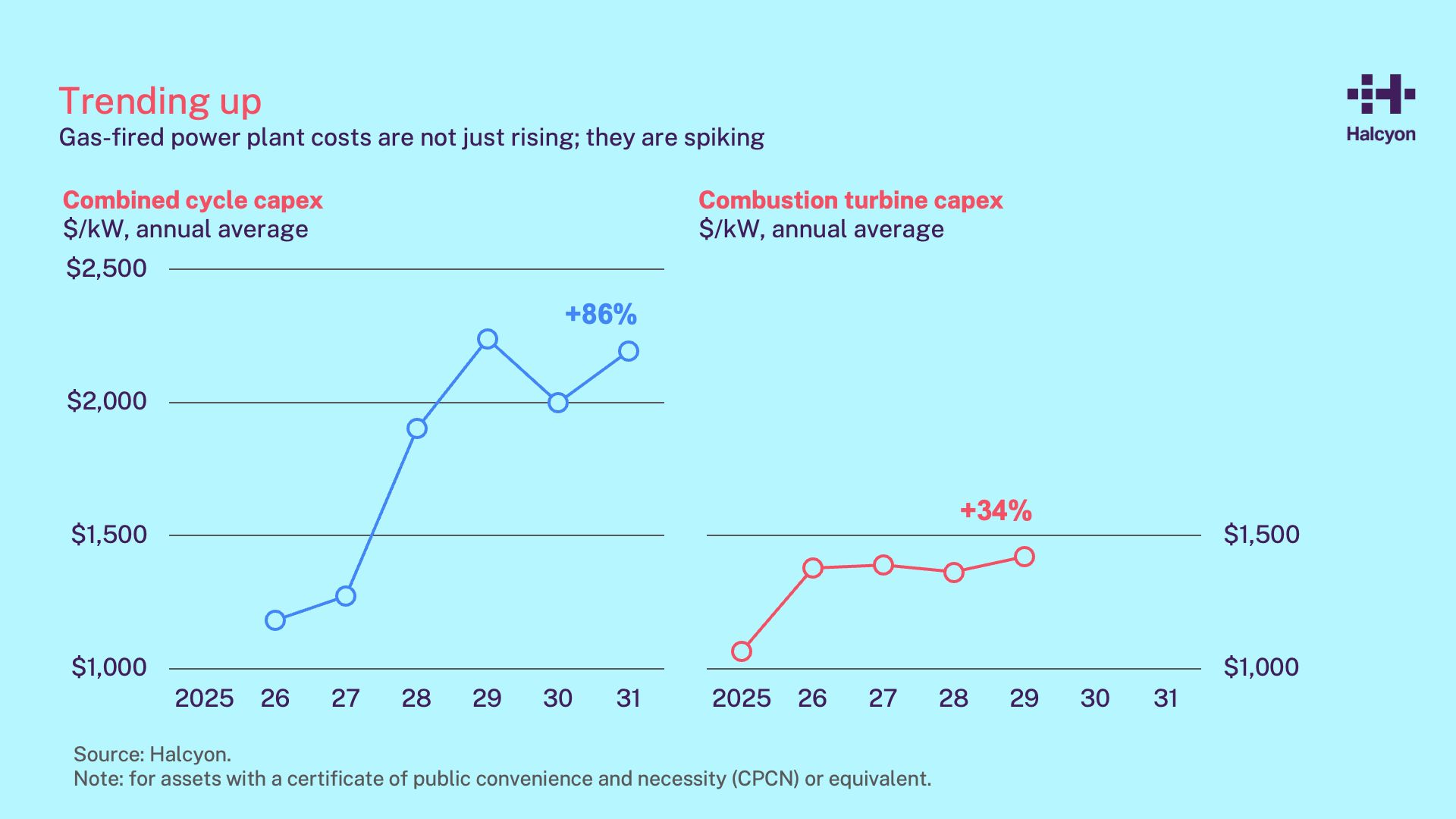

Mitsubishi Heavy Industries aims to double its gas turbine capacity in the next two years as demand for the equipment rises globally due to replacement and data center needs (link). The company emphasized though that its spending would remain judicious as it seeks to avoid over-investing. Gas-fired power plant costs are spiking (link) which increases the risk of investing in new thermal generation: turbines built at inflated near-term prices risk being outcompeted by cheaper, future turbines (link). The capacity value of these turbines is also rising but will be increasingly concentrated in narrow, infrequent windows of time making flexibility and availability key (link).

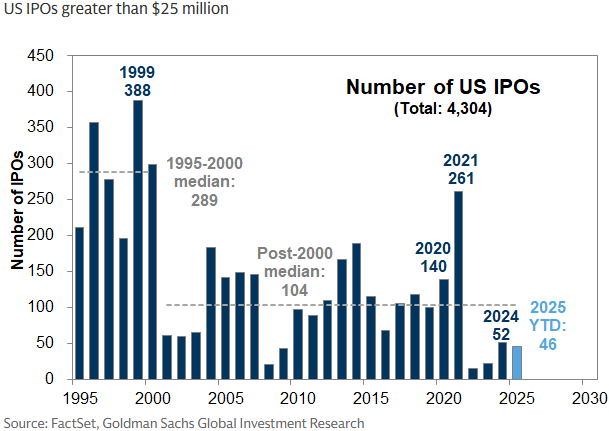

U.S. IPO activity picks up, but not in energy

2025 will likely represent the busiest year for IPOs since 2021 although activity remains substantially below average: there have been 46 US IPOs greater than $25 million YTD, an 18% increase compared with the same point in time last year but substantially below the annual median of 104 deals since 2000 (Goldman Sachs Investment Research). Likewise, IPO proceeds have totaled more than $24 billion YTD, a 28% increase vs. at the same point in 2024 but below the 25-year annual median of $28 billion. Activity has been concentrated in the Health Care, TMT and Financial sectors to date as opposed to in energy and infra. Why? “IPOs are best done into positive sentiment, and right now the market isn’t craving green stories.” (link)

Everchanging tariffs but on a trajectory to stability

On August 29, the U.S. Court of Appeals for the Federal Circuit held that the International Emergency Economic Powers Act (IEEPA) does not authorize former President Trump to impose sweeping tariffs on nearly all imports. Technically from August, but this one missed the cut for last month’s newsletter. The Supreme Court will hear arguments on the legality of IEEPA tariffs in November. This does not include sector-based (Section 232) tariffs. The administration has made a new tariff policy announcement every 3-4 days on average since inauguration but appears to be on a trajectory to increased stability and process.

Policy Notes

As Congress was unable to strike a deal overnight, we now face our first federal government shutdown in nearly seven years. The non-partisan Congressional Budget Office on Tuesday said it expected about 750,000 workers could be furloughed this time, at a cost of roughly $400mn a day (link). The energy system would continue to function but nearly all Federal Energy Regulatory Commission staff and about 60% of Department of Energy full-time equivalent staff members could be furloughed (link). Non-essential activities such as permitting, rulemaking, grant programs, and clean energy R&D would be paused.

The U.S. Department of Energy on Monday announced $625 million in funding aimed at retrofitting and recommissioning coal plants, and offered millions of acres of federal land for new mining (link). Keeping existing plants online will prove a lot easier than capacity additions.

Many left-leaning states are pursuing policies to expedite clean power development. California passed a sweeping energy package including AB1207 which extended the state’s cap-and-trade program; AB825 which starts the process of establishing a regional electricity partnership across the West; and SB 254 which would lower the cost of capital for transmission projects. Funding for the state-run VPP program didn’t make the cut, for now (link).

Elsewhere, New York State’s renewable solicitation prioritizes shovel-ready projects to capture expiring federal tax credits, lower costs and accelerate construction timelines (Infralogic). Pennsylvania Governor Josh Shapiro’s “Lightning Plan” aims to “streamline energy siting decisions” by creating a Reliable Energy Siting and Electric Transition Board. Colorado’s Governor Jared Polis issued executive action to prioritize deployment of clean electricity projects (link). Arizona Governor Katie Hobbs signed an Executive Order to “cut away the bureaucracy and red tape” for energy development on state land (link).

Governors from both parties threatened to pull their states out of PJM due to soaring electricity costs and slow interconnection approval processes (link).

What we're reading

The Pragmatic Climate Reset II (link)

Is AI a bubble (link)

Oracle and Animal Spirits (link)

JP Morgan, Power Rewired (link)

Renewables valuations? (link)

Reigning in California’s Runaway Electricity Rates (link)

The Obscure Philosophical Battle That Could Reshape the Clean Energy Economy (link)

How Climate Polarization Swallowed Bipartisan Energy Policy (link)

More newsletters

June 2026 Newsletter - AGM Edition

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

Read moreApril 2026 Newsletter

After four years, PJM opened back up its generation interconnection queue. Gas is now the dominant technology in the queue compared to solar back in 2022.

Read moreMarch 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read more