By the numbers

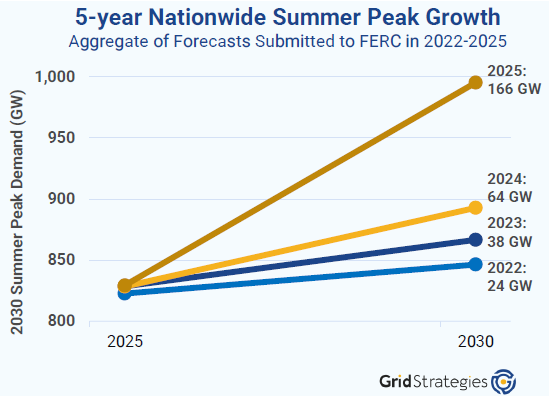

Five-Year Load Growth Up Six-Fold

U.S. electricity usage is forecast to grow by an average of 5.7% per year over the next five years, with peak demand growth forecast at 166 GW, a 3.7% annual rate. By comparison, average U.S. annual energy use growth was a lowly 0.8% in the 2000s and 0.2% in the 2010s. This is the latest from Grid Strategies’ annual report on load growth. A few highlights here, but really, read the report.

Data centers are the largest, but by no means only, driver of demand and energy growth, accounting for about 55% of demand growth in utility load forecasts over the next five years. Utility forecasts overstate national data center demand by roughly 25GW, which would shrink the proportional share further.

Electricity use is forecast to increase more quickly than peak power demand. By 2030, forecasts indicate that total electricity use will increase by 32%. The higher growth rate for electricity use likely reflects high load factors of data centers as well as forecast changes in off-peak energy use by other customers.

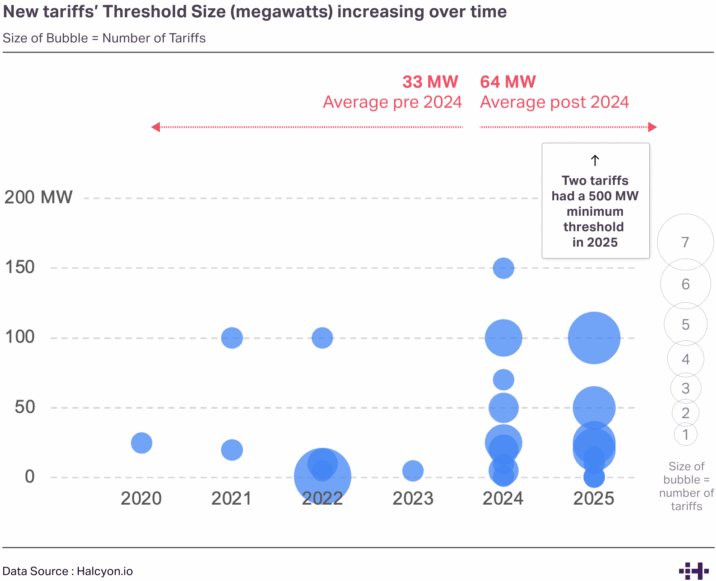

Large loads are getting bigger

As we cover in our Policy Section, Democrats won a spate of elections this month by focusing on affordability and shifting increasing costs to large loads like data centers. Protecting ratepayers from unfair cost burdens is a longstanding challenge but today’s acute pressures are driving a shift in strategy. Large load tariffs have begun to more frequently set higher threshold sizes and minimum contract lengths are increasing in size. For more, see Halcyon and RMI’s review of 65 state-level large load tariffs.

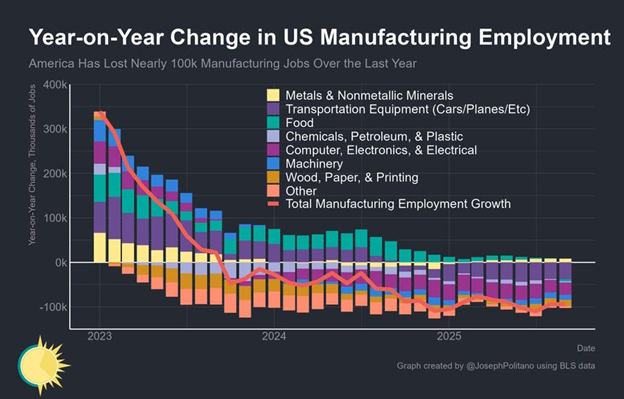

Domestic manufacturing is hurting

Employment in goods-producing industries has fallen steeply since “Liberation day”. The auto industry in particular has swung from expansion under Biden to contraction under Trump, in large part due to tariffs (Noahpinion). Annual construction spending, on a seasonally adjusted basis, also fell to $220 billion in August 2025, down from a high of $240 billion a year earlier (Federal Reserve Bank of St. Louis).

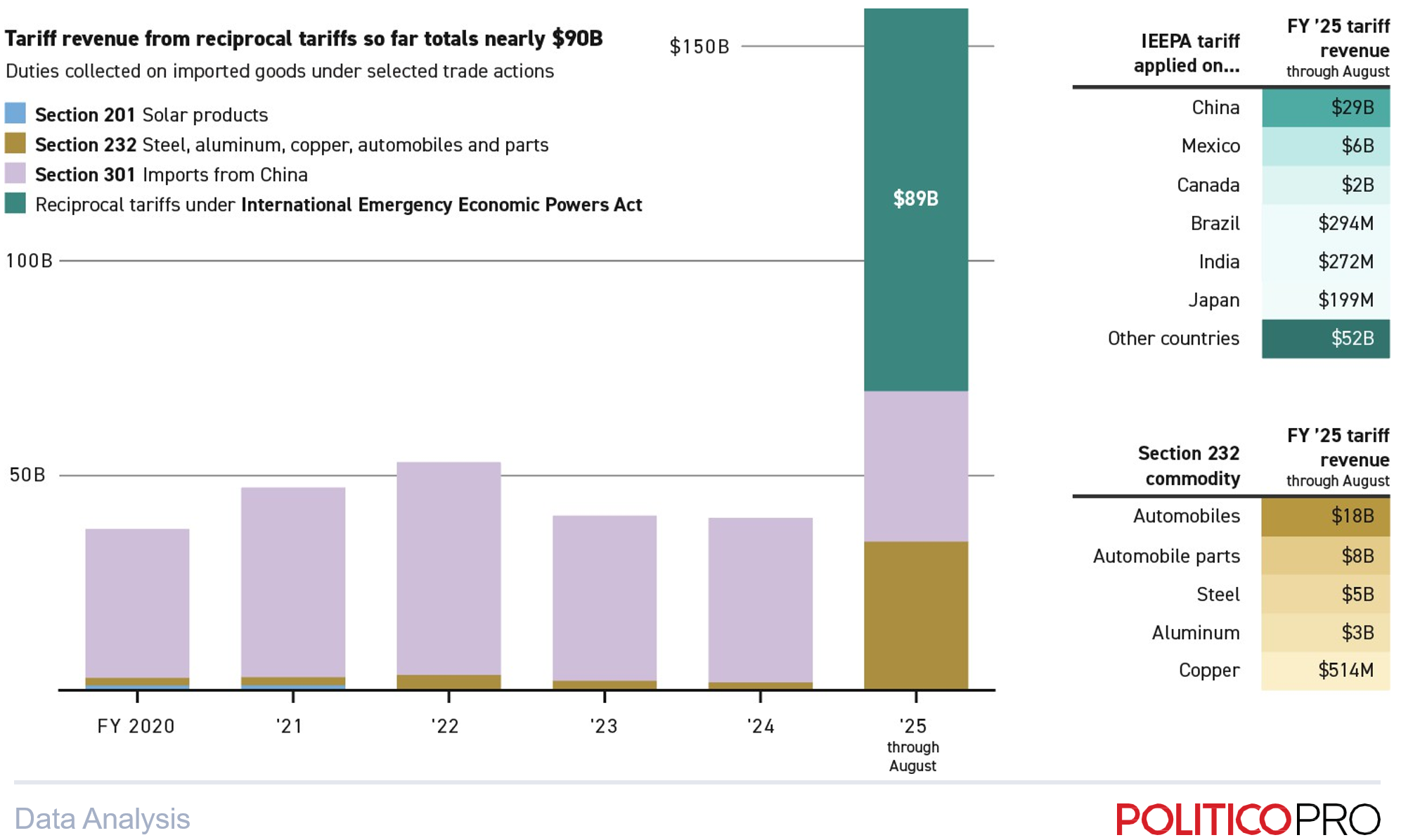

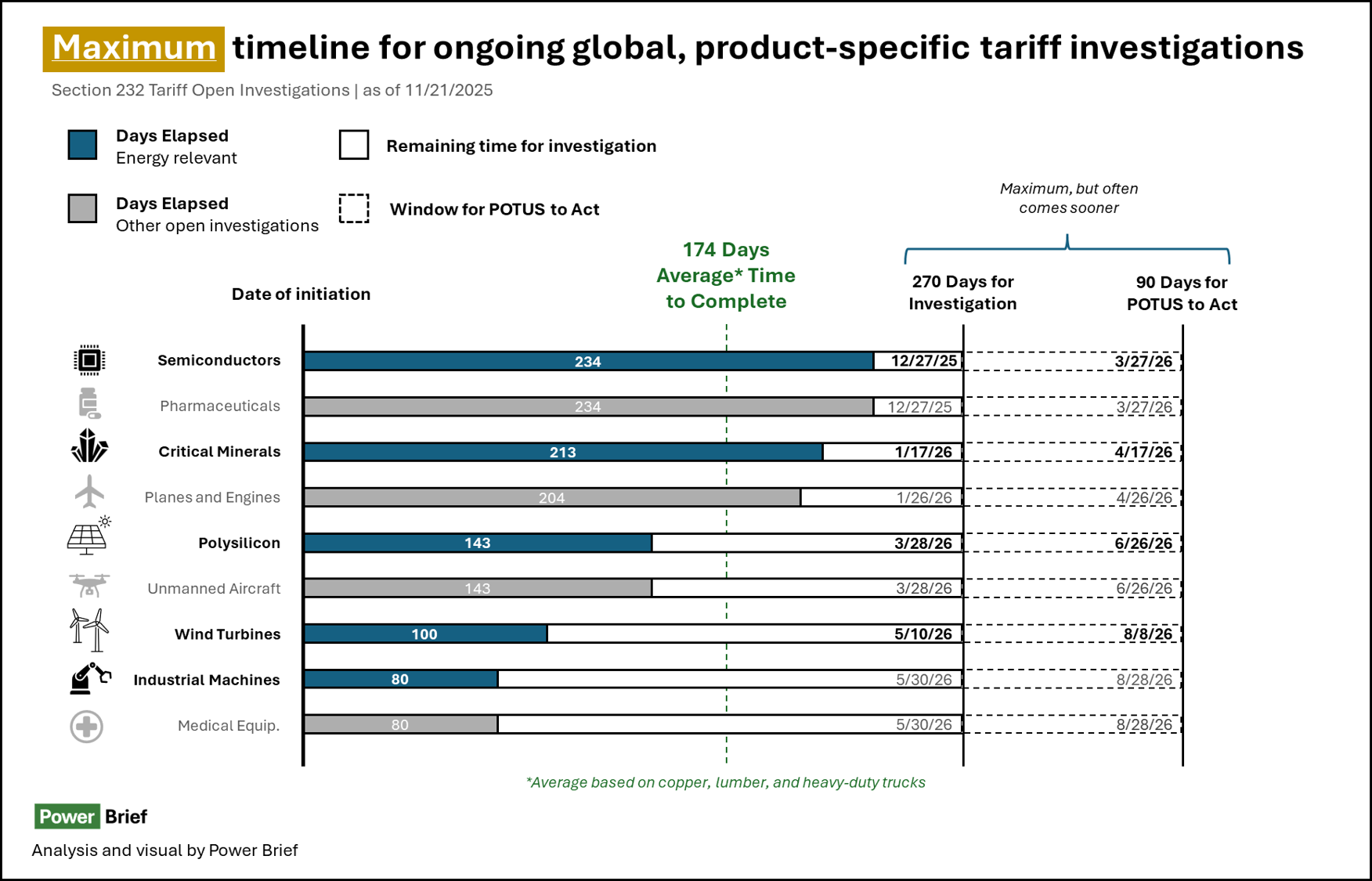

The government collected nearly $160 billion in tariff revenue in the first 11 months of fiscal 2025. About $89 billion of that revenue came from IEEPA tariffs, which the administration may have to reimburse to importers should the Supreme Court strike them down (PoliticoPro). The Supreme Court appeared skeptical of the “reciprocal” tariffs in oral hearings earlier in November. While Trump’s country-specific tariffs face potential annulment, his set of product-specific measures are here to stay. There are currently a handful of open Section 232 investigations which are due to wrap up over the coming months at which point it passes to the President to act.

A near-term change in tack appears unlikely but as affordability becomes a priority, these barriers could be re-examined. The U.S. first imposed tariffs on PV cells back in 2012 and has expanded and increased tariffs on imported clean energy equipment every few years. These efforts push up electricity costs yet have failed to date to build a meaningful competitive domestic industry.

Some predictable, some surprising shifting gas trends

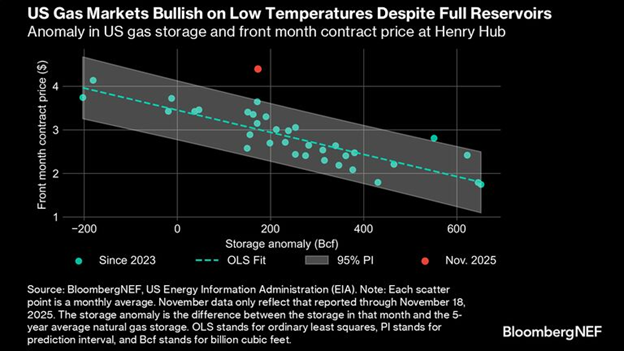

While the U.S. market rushes to contract new gas generation capacity, underlying fundamentals are shifting in ways both predictable and surprising. Let’s start with prices: Henry Hub gas rose above $4.50/MMBtu, their highest levels in three years. These prices are anomolous in the context of high gas storage levels and are tied to colder-than-average weather which could drive withdrawals early in the season (BloombergNEF). They are also buoyed by anticipated demand growth from the power sector and LNG exports.

The anticpated fuel demand will take time to materialize. In the near term, BloombergNEF expects 2025 power sector gas burn to fall by 4% year-over-year, as higher prices drive a shift toward gas-to-coal switching.

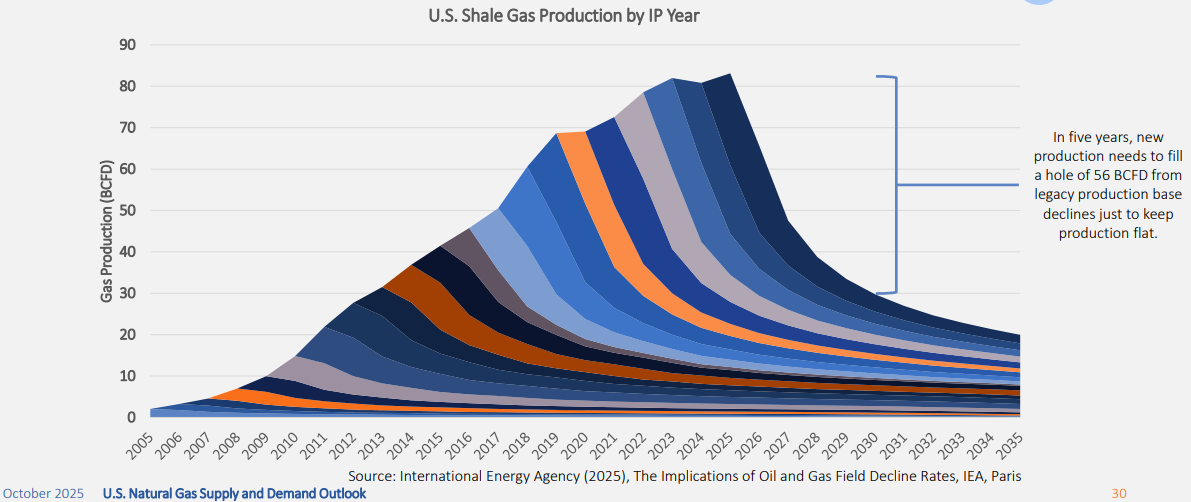

This takes us to production, a topic Seb Kennedy covers at length in a piece titled “US LNG Eats Itself“. In it he writes that increasing production by 20-22 Bcf/d in five years to ~126 Bcf/d to meet this demand is implausible without structurally higher Henry Hub prices to stimulate drilling activity. Crucially “Steep shale decline rates and doubts about the quality of undrilled acreage call into question the assumption that higher prices can overcome geological constraints.” U.S. energy markets have been shaped by the surprise emergence of shale in the mid-2000s, that led to the U.S. becoming a gas exporter by 2017. Faltering production growth at a time of accelerating demand would be mighty shock.

Policy Notes

Power Politics Take Center Stage

Historic power demand forecasts are reckoning with the regulators, politicians, and bureaucrats who determine what can connect, when, and for what cost.

Elections in New Jersey and Virginia, as well as less reported on but important elections for the Georgia Public Service Commission, put power prices and utility bills at the center of a political race for the first time in recent memory. Across the country, Democrats won with a message that focused on affordability and shifting increasing costs to large loads like data centers. That message marked a flip in messaging with Democrats now being the “all of the above” camp while Republicans, led by the White House, dig in with a “fossil or bust” message that excludes wind and solar. Democratic leaders’ support for a handful of high-profile natural gas projects are a way to build durable support for the energy transition as opposed to evidence of its abandonment.

In New York, Governor Kathy Hochul announced an intention to approve a natural gas pipeline and a gas-fired power plant permit, and temporarily delay a mandate to fully electrify new buildings. Despite opposition from environmental advocates, many members of the party see this as a necessary interim step to deliver on affordability while developing more robust plans to achieve the state’s targets.

In Pennsylvania, Governor Josh Shapiro’s bipartisan budget deal to withdraw from the Regional Greenhouse Gas Initiative (RGGI) reflects that participation has become more a partisan flashpoint than a meaningful climate policy tool. Shapiro says he will pursue policies that expand clean energy and lower costs, but specifics remain to be seen.

Governor Newsom in California approved a bipartisan energy affordability package earlier this fall that more directly bundles flexibility on fossil fuels with reaffirming climate targets. The bill extended the state’s cap-and-trade program through 2045, while also allowing for increases in oil production in Kern County to stabilize fuel supply.

Other states are moving forward with identifying ways to advance clean energy development post-OBBBA. The Minnesota Climate Innovation Finance Authority is actively identifying the best way to support renewable energy development in the state, and the Governor of Oregon issued an EO directing state agencies to accelerate permitting and grid infrastructure in support of climate goals.

Politicians Take the Headlines, Regulators (try to) do the Work

Regulatory processes designing new rules to add large loads to the grid are grappling with the competition between the interests of large load customers and the core function of power market regulators to focus on reliability and affordability.

Comments in two key proceedings related to meeting surging electricity demand were due in late November: DOE’s Speed to Power RFI sought input on how to accelerate large-scale transmission and generation; and FERC’s ANOPR on Interconnection of Large Loads to the Interstate Transmission System sought input on developing national load interconnection standards.

The ANOPR is of particular interest as it is poised to inform the trajectory of energy policy over the next decade and has the potential to advance near-term policy discussions across the country. This comes at a time when governments at all levels are grappling with rising demand, aging infrastructure, and increasing electric rates.

A range of organizations intervened or submitted comments in the docket including transmission owners, large load customers, electric utilities, generation providers, grid operators, state PUCs, state AG offices, consumer advocates, and public interest organizations. These filings offer promising solutions for managing large-load generation, and reveal an emerging jurisdictional struggle between FERC and state regulators.

One level down, America’s largest power market, PJM Interconnection, has been in discussions since late this summer to develop a market-specific proposal to manage large load interconnection bottlenecks. Earlier this month stakeholders were unable to reach the necessary two-third agreement to recommend a single proposal for large load interconnection to the PJM board. While proposals that received the most votes had similar themes around flexibility and self-sufficiency, they differed on approach – price responsive demand, “bring your own generation”, temporary curtailment – and whether these attributes should be mandatory or rewarded. The PJM independent board is still expected to put forward a proposal later this year, likely focusing on these areas of emerging consensus.

Stay tuned. Other markets, states and regulators are both developing their own processes, and watching to see how PJM navigates these issues.

What we're reading

How DOE’s Proposed Large Load Interconnection Process Could Unlock the Benefits of Load Flexibility (link)

Aligning transmission investment with development reality (link)

The fall of permitting reform (link)

NERC 2025/27 Winter Reliability Assessment (link)

No more PJM data centers unless they can be reliably served: market monitor (link)

Dispatchability, Not Vibes: What PJM Market Monitor Gets Right—and Misses—on Data Centers Flex (link)

Contributors

Logan Goldie-Scot

VP, Strategy

Maya Kelty

Director, Regulatory Affairs

More newsletters

July 2026 Newsletter

The data center industry continues to surprise both in terms of how quickly the status quo can change, and how resolutely many stakeholders assume the current status quo is now fixed. Eighteen months ago, fully islanded projects were more speculative than real, hyperscalers’ decarbonization bona fides were still mostly intact, and permitting was largely a formality if you followed process. Each looked settled right up until it wasn't, and expecting stability now is a curious leap.

Read moreJune 2026 Newsletter - AGM Edition

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

Read moreApril 2026 Newsletter

After four years, PJM opened back up its generation interconnection queue. Gas is now the dominant technology in the queue compared to solar back in 2022.

Read more