Expert View

31 Oct 2024

The middle-market 0pportunity

Global energy transition and climate investment rose to $2 trillion in 2023 according to BloombergNEF, roughly five times what it was a decade ago when Generate was founded.

Expert View By Logan Goldie-Scot

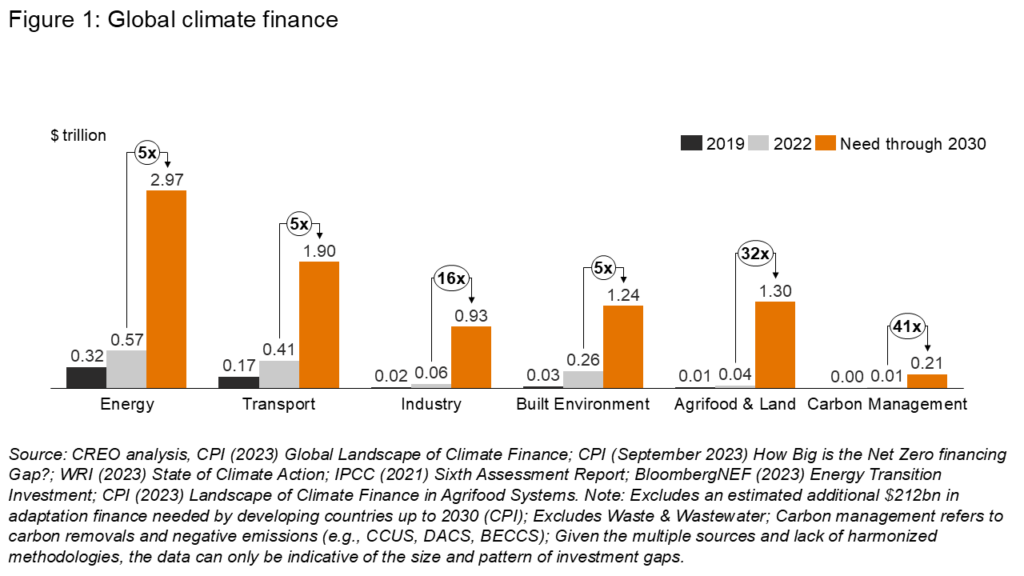

Looking ahead, to meet global climate targets, annual spending across energy, transport, and the built environment needs to increase fivefold through to 2030 (Figure 1). The required scale-up is even greater in areas like industrial processes where investment has yet to really get off the ground.

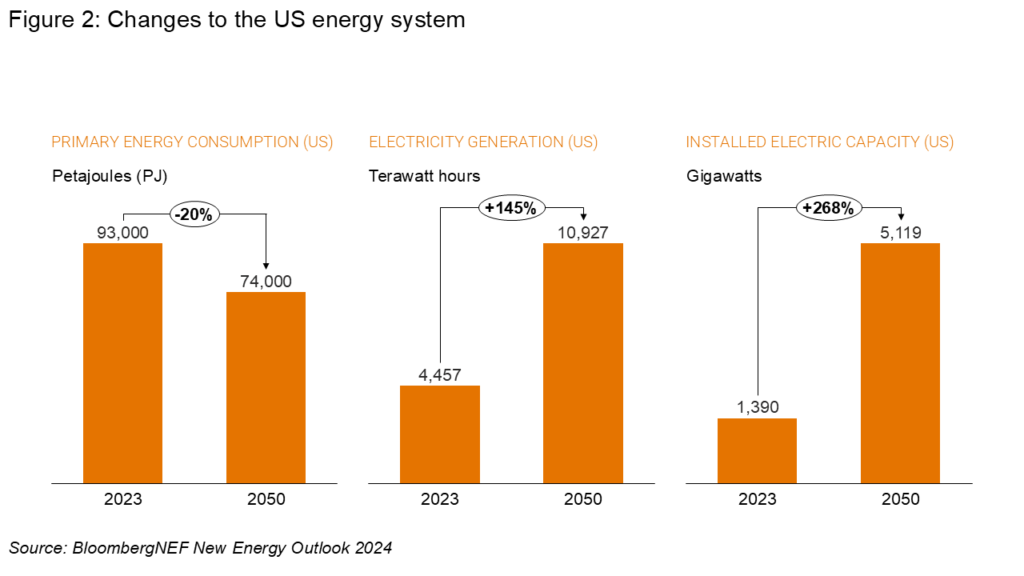

The trillions of dollars of investment both decarbonize and transform the system we know today. This results in a very different deal profile compared to earlier waves of infrastructure investment. For starters, the power system becomes central to our decarbonization efforts: widespread electrification results in a more efficient energy system and a much larger power system. In the US for instance, primary energy drops 20% by 2050 but required electric capacity increases 268% (Figure 2).

While gigawatt-scale nuclear facilities and interstate, as well as interregional, transmission capacity remain critical, the US power system is increasingly distributed. A scan of the 30,000 operating power projects across the country is illustrative here: the average size of a US coal facility is 404 MW, a natural gas project is 86 MW, and a solar project is just 17 MW (Orennia). Eighty percent of new capacity that came online last year was solar, wind, and storage, further entrenching this dynamic.

In terms of the capital environment, climate funds raised a total of $110 billion in 2023 (Pitchbook), 4.5 times what was raised a decade ago. While this marks progress, it falls far short of the scale of investment needed. Annual capital requirements across the six sectors shown in Figure 1 total $9 trillion through 2030, a stark contrast to recent records still counted in billions. We still have a long way to go.

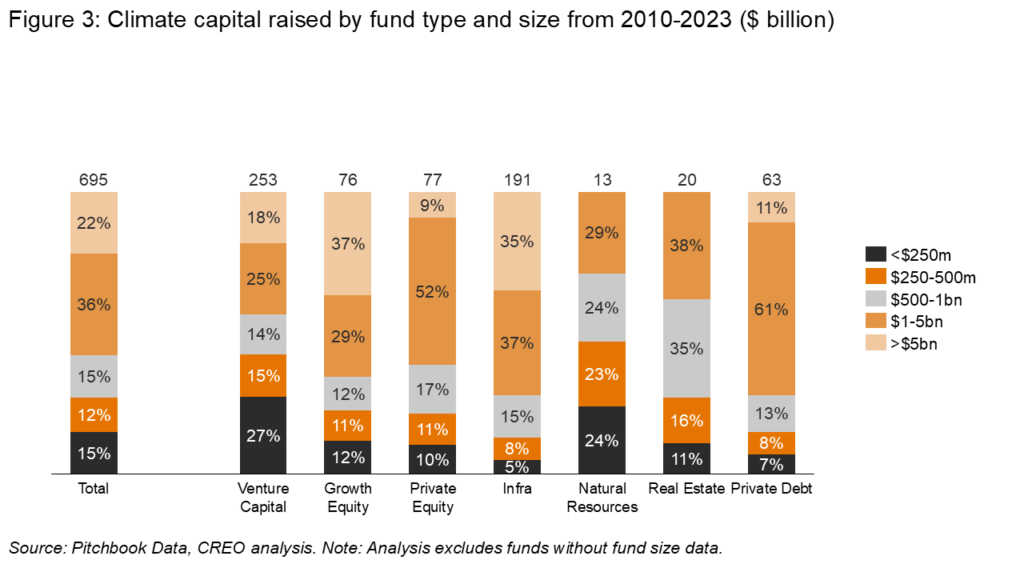

Much of the new capital flowing into the market is going into large, billion-dollar-plus funds. Only 13% of funds raised from 2010 to 2023 in infrastructure were below $500 million, with an additional 15% being sub $1 billion. We need all kinds of investment into all sizes of assets, but we must also understand that the nature of the system we’re building is different. Alongside large funds focused on big projects, we need to invest real capital into the middle market.

Some 80% of US energy transition deals by count (Infralogic) and 40% by amount had a deal value below $400 million. Deals larger than this typically have high transaction costs, are focused on monolithic assets, and benefit from asset-size economies of scale. In the new paradigm, the minimum efficient scale to deliver compelling customer value shifts downwards. As large infrastructure funds have shifted their focus to mega-deals, these smaller deals risk being overlooked.

This creates a significant opportunity for specialized managers who understand and can create value from smaller, distributed assets. Alongside the healthy deal flow, this asset class is also remarkably attractive. Technology costs have fallen dramatically, driven by manufacturing rather than asset economies of scale. Smaller assets are also less likely to face cost overruns, a challenge often seen in mega-projects (Professor Bent Flyvbjerg, How Big Things Get Done). The cost of coordinating these distributed assets has also fallen considerably while the value they deliver both to customers and to the broader system is on the rise.

Investors who understand this opportunity are already taking advantage of these dynamics. Success requires a deep understanding of these types of assets and how the size, technology profiles, and customer dynamics are different from their large-scale predecessors. Done well, the rewards can be meaningful: middle-market funds relative to large-cap funds have delivered between 150 and 250 basis points of better return on a risk-adjusted basis (Patrizia, Investing in mid-market infrastructure).

More insights

Communities Have More Leverage Over the AI Buildout Than They Realize

Communities are skeptical of data centers. They don’t know if they like the underlying technology, they certainly are not feeling the increase in power costs they attribute to this massive build, and they don’t feel like they need to provide tax assistance to the richest companies in the world. The companies needing to build are organizing fast through procurement standards, model legislation, financing structures, and political infrastructure to make sure their interests are represented at every level where decisions get made. Advocates need to help communities benefit from this moment, not be a reflexive “no” and convince communities they have nothing to gain. It isn’t true and it won’t help the people climate, environmental, and community organizing groups claim to represent. Communities that organize with equal seriousness, around what they want from this buildout rather than around whether they want it at all, will end the decade with infrastructure their grandchildren still benefit from. That infrastructure can be clean, affordable, and reliable. Communities that spend the leverage on saying no will get what they always have: whatever is left over after capital sets the terms. Developers that try to undercut productive efforts to build that kind of resilience in communities will end up losing. Both sides need to realize that the relationship can be productive and valuable.

Read moreHigh Stakes at CERAWeek

It is not often - read "never" - that a CEO's decision NOT to attend a conference is a global headline but so it was this weekend when Amin Nasser, the veteran CEO of Saudi Aramco, withdrew from CERAWeek in order to attend to matters closer to home. Mr. Nasser's withdrawal underlines that the focus for all of us still heading to Houston will be on the Straits of Hormuz and its short, medium and long term consequences on gasoline prices. And all the while, the focus on high gasoline prices at CERA this week is likely to obscure the other energy price shock lurking in the shadows which is the inexorable rise of electricity prices across the United States. Unlike gasoline prices, once retail electricity prices rise, they almost never go down.

Read moreIndustrial Decarbonization: How Thermal Storage Can Electrify Heat at Scale

Investment in thermal energy storage has accelerated in recent years as technical progress and customer demand have improved project bankability. Since 2020, sector funding has grown and shifted toward later-stage investors, reflecting greater confidence in TES’s readiness for commercial deployment.

Read more