Article

House Tax Bill: From Politics to Practicalities

The House passed a sweeping tax bill on May 22 that includes major changes to clean energy tax credits. It marks a significant step in GOP lawmakers’ efforts to move the tax legislation through Congress but nothing is final and there is a long way to go before anything is signed into law. The bill will now go to the Senate, where we expect it will be revised.

The tax credit changes themselves have been covered extensively in other outlets (see here, here) so we won’t recap the details here. As the Senate debates the details, there are a few things we know:

- If federal investments continue in line with the past few years, U.S. infrastructure faces a $3.7 trillion funding gap over the next decade (ASCE Report Card). As federal spending pulls back, this gap increases.

- The U.S. must build more power infrastructure, more quickly, in more places than it has in over four decades if it wants to establish and maintain a leading position in the AI arms race and deliver economic prosperity to American communities.

- To achieve the above reliably and affordably, we need power projects that are quick to bring online, economic, and flexible. You cannot meet this demand on time and cost competitively without a lot of solar and storage.

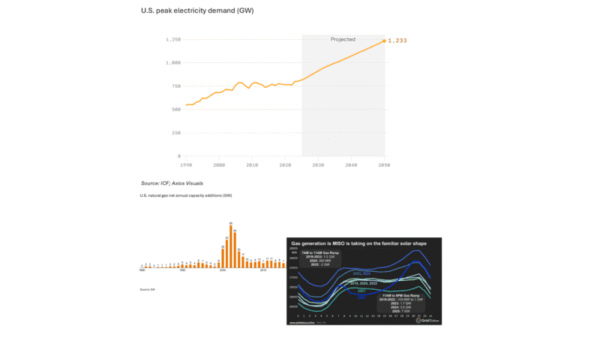

To put some numbers on this: A May ICF report estimated that U.S. electricity demand will increase 25% by 2030 (ICF).

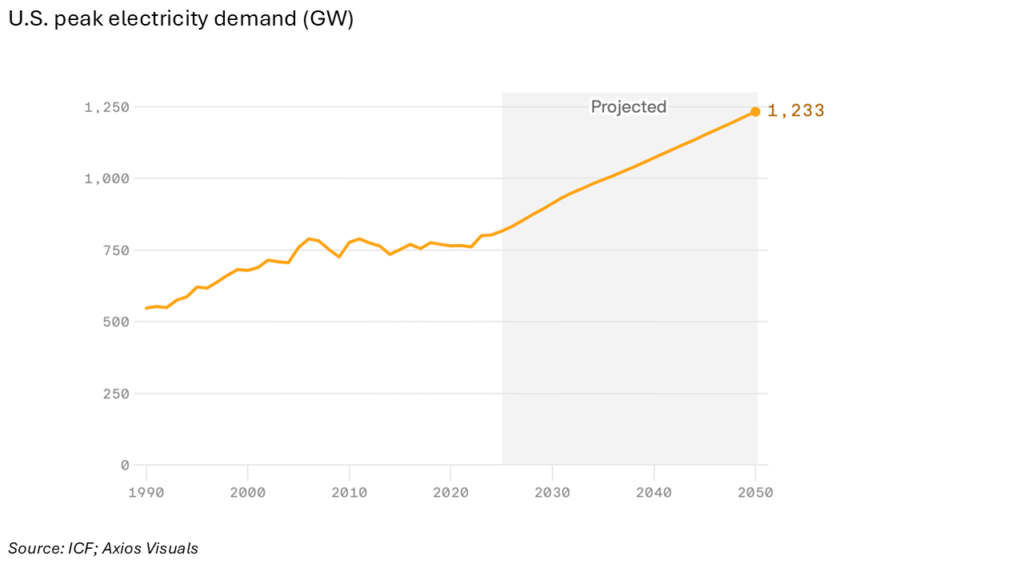

The authors estimate that this will require 80 GW of annual capacity additions, over double the average of net capacity additions over the last decade. Many news headlines suggest that natural gas will seamlessly step into this gap. Natural gas has an important role to play in the U.S. power system but the industry is simply not set up to meet this demand singlehandedly, even once you adjust for capacity factors.

Over the last decade, roughly 10 GW of net natural gas capacity has come online each year. Gas capacity additions will rise in the near term to help meet this new demand but turbine supply, pipeline capacity, workforce availability, rising costs, and long memories will all constrain this uptake. When the industry last approached this level of capacity growth, in the 2000s, independent power producers that had financed extensive gas‐plant portfolios suffered substantial write‐downs. By default, this leaves room for clean power technologies. BloombergNEF tracked 69 GW of wind, solar, and storage installations in the U.S. in 2024. And the industry has shown it can scale rapidly from year to year.

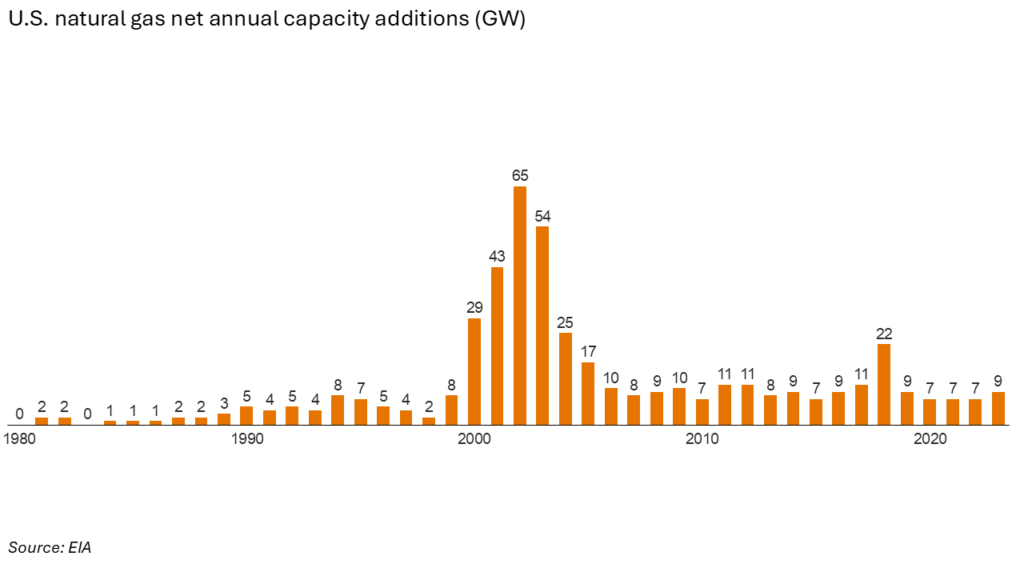

Even in markets dominated by gas and coal such as PJM and MISO, solar is now a notable percentage of generation. In an uncanny coincidence spotted by GridStatus, recent solar generation records for MISO and PJM each met 18% of load (link). This matters in absolute terms and also because as you add more solar to a system it then dictates the shape of other resources, such as gas. The gas that we do add to the system should therefore be flexible gas such as open-cycle gas turbines, not inflexible combined cycle projects.

Previous pockets of energy scarcity in the US have been short in duration, often weather or failure based. A failure to maintain, indeed to accelerate, clean power capacity additions will lead to more structural shortages. Affordability is also critical. The ICF report warns that rising consumption could raise retail rates as much as 40% by 2030 (link). Trying to meet demand primarily with natural gas, at a time when global turbine prices and US gas forwards are rising, threatens to exacerbate this.

What It Means: A Time to Move From Politics to Practicalities

Translating the U.S.’s power challenges into effective policy requires an understanding of what developers and investors need to add capacity and power communities. The tax bill is now with the Senate, meaning Congress still has time to consider the U.S.’s power needs and design policies accordingly. Policy will be most effective if it includes:

- Meaningful and predictable incentives that help investors make decisions about allocating capital and give developers the certainty necessary to build projects;

- “Commence construction” requirements that give investors certainty around the tax credit’s value prior to allocating capital;

- Flexibility, such as that offered by transferability, that streamline investment processes and maximize uptake.

This is not our first, and won’t be our last on headwinds in the space. See our April expert view for more infrastructure market analysis.

At times like these, it is natural for all eyes to focus on Washington D.C. Remember though that investment and procurement decisions are made across the U.S. by companies large and small, based on their needs. A core ethos at Generate is that customers’ needs drive markets. Our expert view this month explores how corporates are making energy and infrastructure business decisions, and what that means for the broader state of corporate decarbonization.

More insights

What the Senate's reconciliation bill means for clean power

The bottom line is that the Senate text will lead the U.S. to build less clean power, it will be more expensive, and power prices will rise. The grid will be less reliable, possibly leading to power shortages and blackouts for American households and businesses. There’s still much that we do not know, and the

Read moreTariff Updates: From Chaos to Convention

What We Know: The future of President Trump’s “Liberation Day” tariffs hit a significant obstacle last week. On May 28, the U.S. Court of International Trade (CIT) struck down core pieces of the so-called reciprocal tariffs, ruling that the President had overstepped his authority under the International Emergency Economic Powers Act (IEEPA) of 1977. Some of President

Read moreHouse Tax Bill: From Politics to Practicalities

The tax credit changes themselves have been covered extensively in other outlets (see here, here) so we won’t recap the details here. As the Senate debates the details, there are a few things we know: To put some numbers on this: A May ICF report estimated that U.S. electricity demand will increase 25% by 2030 (ICF). The authors

Read more