Expert View

29 Nov 2024

Investors and banks are voting for the infrastructure transition with their dollars

The US election’s outcome will undoubtedly have consequences for the infrastructure transition, but rumors of its death are overblown. While the market may face challenges, these challenges will prompt a flight to quality investors and assets.

Expert View By Edward Bossange and Jonah Goldman

Infrastructure investors with strong track records, specialized expertise, attractive returns, large pipelines, and operational and investment experience will continue to garner the backing of large investors and banks. Steel will still go in the ground to build the sustainable infrastructure assets that have created real economic value in communities across the country.

The Policy Outlook

Evaluating how a second Trump administration will shape the infrastructure transition requires understanding how federal policy interacts with economic markets. We are now in a phase of the infrastructure transition where what was once theoretical is now real. Money promised by the Inflation Reduction Act (IRA) is flowing, and that money is showing up in states and districts across the country. Those projects were built by real people, in real communities, and they are powering real homes, schools, hospitals, and grocery stores. In short, it’s now a fixture of the real economy.

The infrastructure transition’s tangibility makes it more resilient to policy shifts. Policy often has a symbiotic, mutually reinforcing relationship with flows of capital. Productive policy leads investors to put steel in the ground, jobs on the board, and helps communities of voters thrive – which begets more policy and more capital from the public and private sectors, to expand those successes. Fundamentally, this relationship keeps economic shifts durable across political fluctuations. This is where the rhetoric of politics diverges from the reality of policy – in August, eighteen Republican House members wrote a letter defending the IRA and vowing to vote against it. Fourteen won reelection.

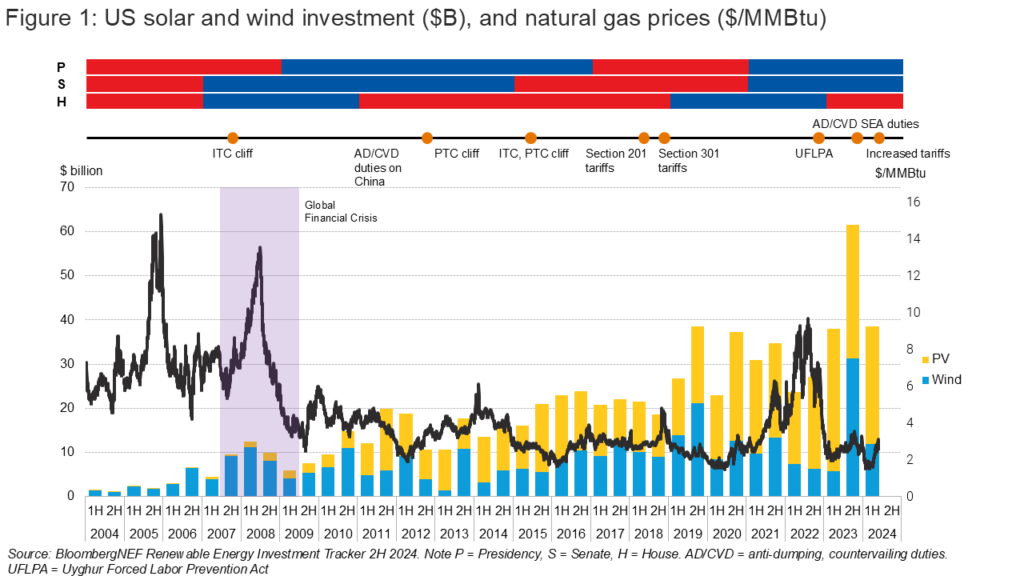

The new administration will change the contours of the transition in the short term – what gets invested in, where those investments are made, and with what public support – but it won’t stop the transition. As shown in Figure 1, the transition has already weathered several cycles of red and blue waves, as well as major economic events and policy regimes including the global financial crisis, fluctuations in gas prices, and varying approaches toward tariffs. When mapped against investment in the US wind and solar industries, the resulting chart illustrates how the clean energy industry has grown steadily despite changing political realities.

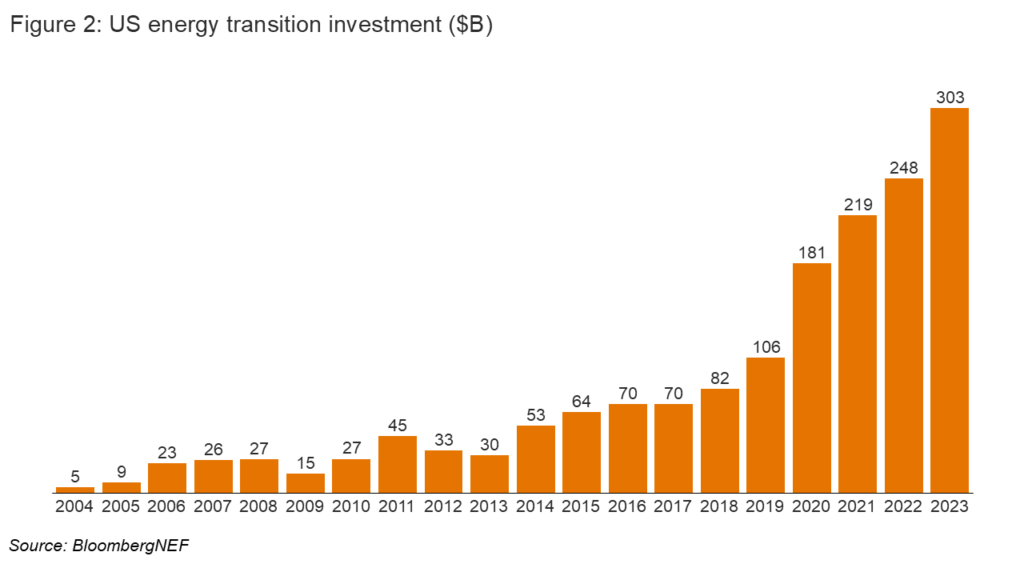

The situation was the same over the last 12 months. A Harris victory was never a foregone – or bankable – conclusion, and the prospect of Democratic control over the Senate, House, and Presidency was unlikely. Yet that hasn’t stopped investment from flowing into the sustainable infrastructure market, especially as energy transition assets become more mainstream. Last year garnered the highest-ever investment in the US energy transition, with $303 billion invested compared to $30 billion 10 years prior (BloombergNEF).

The Funding Environment

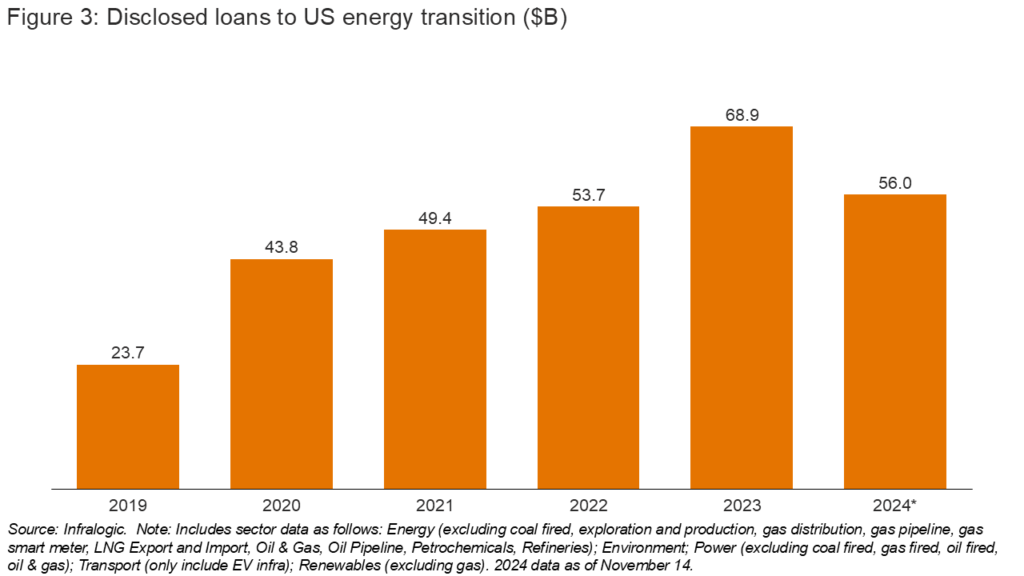

These investment figures underscore how the sustainable infrastructure market has grown into an established market able to withstand headwinds and secure capital from prominent and respected capital providers. Back in 2014 when Generate was founded, the infrastructure transition was seen as a risky, emerging market, with skepticism around the viability of its theory of the case. In the succeeding 10 years, anchors of the financial industry have backed it with their dollars. Commercial banks have loaned $125 billion to US energy transition projects and companies since the beginning of 2023, and 2024 totals as of mid-November already exceed 2022 levels.

We do not expect the funding environment for sustainable infrastructure projects to be imperiled now that the market is experiencing more headwinds. Rather, we anticipate a flight to quality. In environments where capital is more constricted and investors and lenders therefore have a lower appetite for risk, performance records are critical. There are, and will continue to be, capital and investment opportunities available to serious sustainable infrastructure investors and operators capable of delivering commercially. These firms have the expertise and pipelines needed to adapt and take advantage of existing opportunities, withstand scrutiny, and inspire investor and lender confidence. Key among the proof points for these firms are the ability to raise capital from the most respected and rigorous investors and secure loans from the best banks.

Generate is proud to be considered one of these trusted firms. Earlier this year, Generate announced our $1.5 billion fundraise from investors including CalSTRS, Hesta, QIC, and others (link). Most recently, we secured a $1.2 billion corporate credit facility from JP Morgan, BMO, Scotiabank, and 11 other lenders (link). These financings substantiate Generate’s reputation as a long-term player in the infrastructure transition, built to withstand economic and political cycles. We continue to raise and secure capital by remaining targeted and focused on building assets, providing real value to communities and customers, and using our market knowledge to take risks and structure deals creatively, such as through our tax equity (link) and credit strategies (link). And so the cycle continues. Policy will drive investments, and good investments will support good policy. The firms that can navigate both will be successful in both the fat times and the lean times.

Amid the confusion stemming from our current political landscape, large investors and banks continue to vote with their dollars – and the numbers show they have voted in favor of the infrastructure transition. These funders have demonstrated their confidence in firms like Generate to continue building sustainable infrastructure projects and markets, and we are committed to proving their case.

Contributors

Edward Bossange

Chief Capital Formation Officer

Jonah Goldman

Chief Strategy Officer

SECTIONS

More insights

High Stakes at CERAWeek

It is not often - read "never" - that a CEO's decision NOT to attend a conference is a global headline but so it was this weekend when Amin Nasser, the veteran CEO of Saudi Aramco, withdrew from CERAWeek in order to attend to matters closer to home. Mr. Nasser's withdrawal underlines that the focus for all of us still heading to Houston will be on the Straits of Hormuz and its short, medium and long term consequences on gasoline prices. And all the while, the focus on high gasoline prices at CERA this week is likely to obscure the other energy price shock lurking in the shadows which is the inexorable rise of electricity prices across the United States. Unlike gasoline prices, once retail electricity prices rise, they almost never go down.

Read moreIndustrial Decarbonization: How Thermal Storage Can Electrify Heat at Scale

Investment in thermal energy storage has accelerated in recent years as technical progress and customer demand have improved project bankability. Since 2020, sector funding has grown and shifted toward later-stage investors, reflecting greater confidence in TES’s readiness for commercial deployment.

Read moreConsolidation: The Pathway to Enduring Impact

It is easy to be disoriented by the swing from exuberance to pessimism that has defined the clean energy sector in recent years. Yet these moments are precisely when opportunity is greatest. Beneath the headlines are clear indicators of tremendous potential in the U.S. energy transition. The challenge is to separate fundamentals from sentiment, to acknowledge and fix the mistakes that we have made, and to chart a path to scale rooted in discipline, operational excellence, and commercial reality.

Read more