Expert View

31 Jan 2025

A new way for tax credits to power communities

Federal tax credits are an essential component of financing renewable power projects. These credits have proven incredibly resilient over decades, despite changes in US administrations and congressional control. The support from policy makers across the country is not surprising – these projects are connecting communities with affordable power that keeps the air clean and the lights on.

Expert View By Ryan Miller

Though popular, the tax credits were historically cumbersome and complicated, which kept capital on the sidelines. Project developers were required to use complex tax equity structures to monetize these tax benefits efficiently. Tax legislation and guidance led to the emergence of novel financial structures such as the partnership flip, the sale lease-back, and the inverted lease, the execution of which became a core competency for project developers. In 2022, updates to the provisions fundamentally altered this landscape by permitting direct sales of tax credits to third parties, i.e., “transferability.” This change presented an opportunity to quickly scale and expand the market for renewable energy tax credits. But as market participants evaluated how to optimize these credits, complications arose that necessitated creative strategies to fully unlock the potential to build assets.

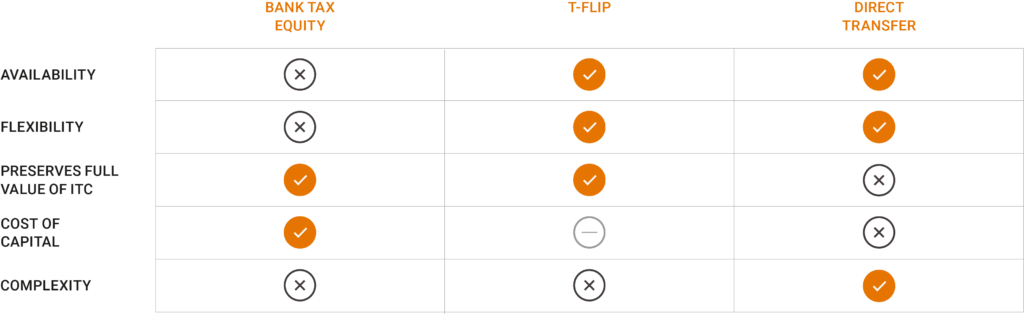

Recently, a new tax credit investment structure has begun to gain acceptance in the market. Called the transferability flip structure or “T-Flip,” it helps unlock attractive pre-tax returns for tax equity providers while preserving the full value of the tax credit. The T-Flip offers a flexible, accretive financing solution for developers looking for a tax equity solution beyond the existing – but limited – tax equity investor market. For investors, this approach offers attractive pre-tax returns in a senior position of the capital stack, typically reserved for risk-averse institutional tax equity providers. The Generate team has helped lead the charge by transacting on over $10 billion on both the sponsor and tax investor side of complex tax equity transactions.

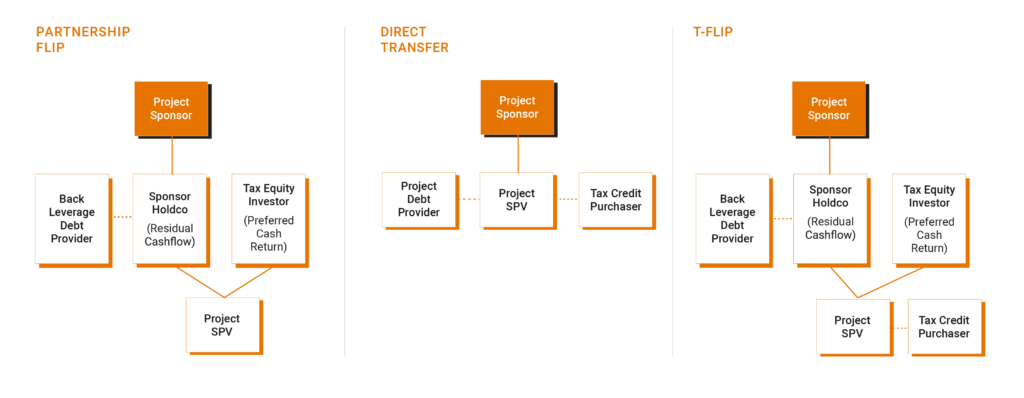

Traditional Tax Equity

In the past, individuals had to be the owner of renewable power projects in order to claim the tax credits. To monetize these credits, project sponsors typically entered “partnership flip” transactions with a limited number of large financial institutions and public companies with significant tax liabilities and extensive structuring expertise in these transactions. In a partnership flip transaction, the project sponsor and a tax equity investor contribute cash to a partnership, acquire a renewable energy project at fair value, and then disproportionately allocate the tax benefits of the project to the tax investor. The tax investor in turn has a senior claim to a small percentage of the project’s operating cash flows, but the primary source of its return is tax credits. Concurrently, the project sponsor secures bank debt on its equity interest in the partnership, such that the debt is structurally subordinated to the tax investor’s claim on project cash flow. Notably, this project acquisition mechanic facilitated a step-up in tax basis – and the value of the associated tax credits – from project cost to fair market value. These tax monetization transactions were complex, had significant transaction costs, and were not available to many sponsors or accessible for many potential tax credit investors.

Transferability

Policy changes made in recent years were designed to deliver more clean power to more communities by alleviating these issues by permitting the direct transfer of tax credits from the project owner to another taxpayer. These transferability provisions had the potential to greatly simplify renewable energy project capital structures and make it easier for project developers – especially newer and less experienced players – to access the tax credit market. This legislation was anticipated to have truly massive impact: before 2022, tax equity investment volume hovered around $20 billion, and market observers now predict total volumes would surpass $90 billion by 2030, with up to 60% to be monetized through transferability (Reunion).

However, transferability comes with its own challenges for sponsors. Most importantly, simple direct transfer of credits cannot maximize the value of tax assets because it doesn’t allow for a basis step-up.

Transferability Flip Structure (“T-Flip”)

In light of this structural limitation of direct transfer, the market has begun to coalesce around new structures to preserve the full tax credit value allowed under IRS regulations. In particular, the T-Flip structure preserves the value of the step-up while also allowing a project to access a much wider market of potential credit buyers – meaning more energy can be deployed in more places, financed by more players in the market. In operation it retains key elements of the traditional partnership flip, including the sale of the project to facilitate an increase in tax basis. But rather than monetize these credits through an extended hold period in a joint venture with the tax investor, the partnership sells the tax credits generated to a party who can more efficiently monetize them.

These structures have quickly taken hold in the market, with an estimated $17 billion in transaction closed in 2024 compared to $11 billion for traditional partnership flips (Norton Rose Fulbright). This shift in structure results in more attractive pre-tax returns for tax equity providers while preserving the full value of the tax credit. T-Flips also provide sponsors with greater flexibility in structuring, including timing of funding and allocation of tax and cash attributes. Traditional tax equity providers have also adopted T-Flips to optimize limited tax capacity while transacting on more deals. Given the complexity of these transactions, selecting an experienced, flexible financing partner is essential.

More insights

High Stakes at CERAWeek

It is not often - read "never" - that a CEO's decision NOT to attend a conference is a global headline but so it was this weekend when Amin Nasser, the veteran CEO of Saudi Aramco, withdrew from CERAWeek in order to attend to matters closer to home. Mr. Nasser's withdrawal underlines that the focus for all of us still heading to Houston will be on the Straits of Hormuz and its short, medium and long term consequences on gasoline prices. And all the while, the focus on high gasoline prices at CERA this week is likely to obscure the other energy price shock lurking in the shadows which is the inexorable rise of electricity prices across the United States. Unlike gasoline prices, once retail electricity prices rise, they almost never go down.

Read moreIndustrial Decarbonization: How Thermal Storage Can Electrify Heat at Scale

Investment in thermal energy storage has accelerated in recent years as technical progress and customer demand have improved project bankability. Since 2020, sector funding has grown and shifted toward later-stage investors, reflecting greater confidence in TES’s readiness for commercial deployment.

Read moreConsolidation: The Pathway to Enduring Impact

It is easy to be disoriented by the swing from exuberance to pessimism that has defined the clean energy sector in recent years. Yet these moments are precisely when opportunity is greatest. Beneath the headlines are clear indicators of tremendous potential in the U.S. energy transition. The challenge is to separate fundamentals from sentiment, to acknowledge and fix the mistakes that we have made, and to chart a path to scale rooted in discipline, operational excellence, and commercial reality.

Read more