Slop, affordability, reforms

Flying blind

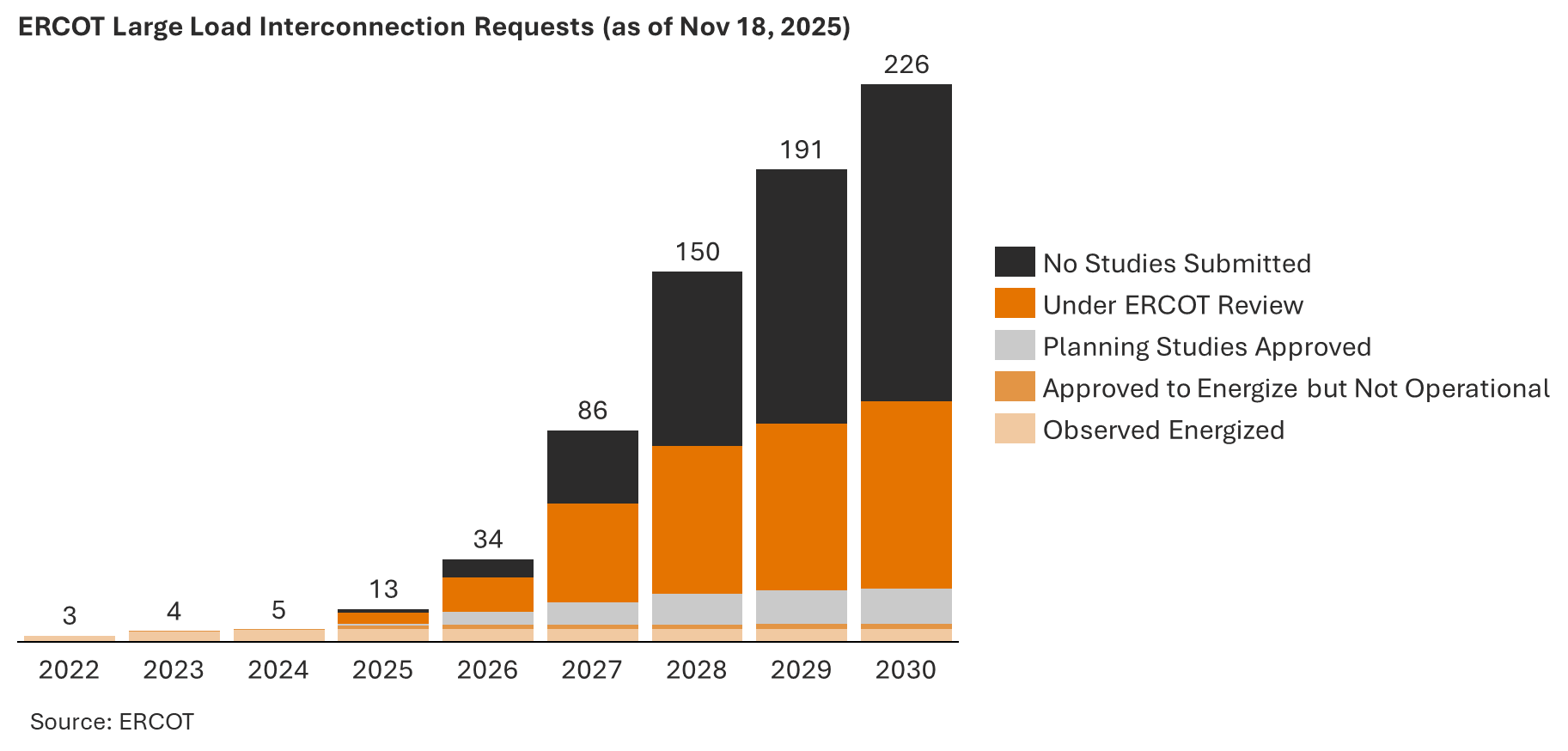

In 2025, the digital aspirations of data centers collided with the physical reality of the U.S. power system. Consider this: ERCOT is now tracking ≈226 GW of Large Loads seeking interconnection, versus 63 GW in December 2024 (ERCOT). 73% of requests are data centers, and 57% of the 2030 requests have yet to submit a study.

What is real? How much will materialize? When?

To find out, ERCOT intends to overhaul the process in early 2026. It hopes to improve visibility and weed out phantom or unviable projects. The likely end state is a large, but shrinked queue of more viable applications. Similar dynamics, of bulging queues then downward corrections, are visible elsewhere: Georgia Power’s pipeline of large load economic development projects shrank a net 6 GW from the second quarter to the third quarter to 50.9 GW (Utility Dive).

Improving utility and system operator’s approach to forecasting will help plan, as papers from E3 and the Energy Systems Integration Group show, but to an extent we remain in the unknowable phase of this cycle. Acknowledging this will lead to better outcomes. As Benedict Evans articulates in his latest annual presentation (see the slides for the full picture):

How will the new thing work? We don’t know

Noise, hype, anti-hype

This often brings bubbles

But when the dust settles, the world has changed

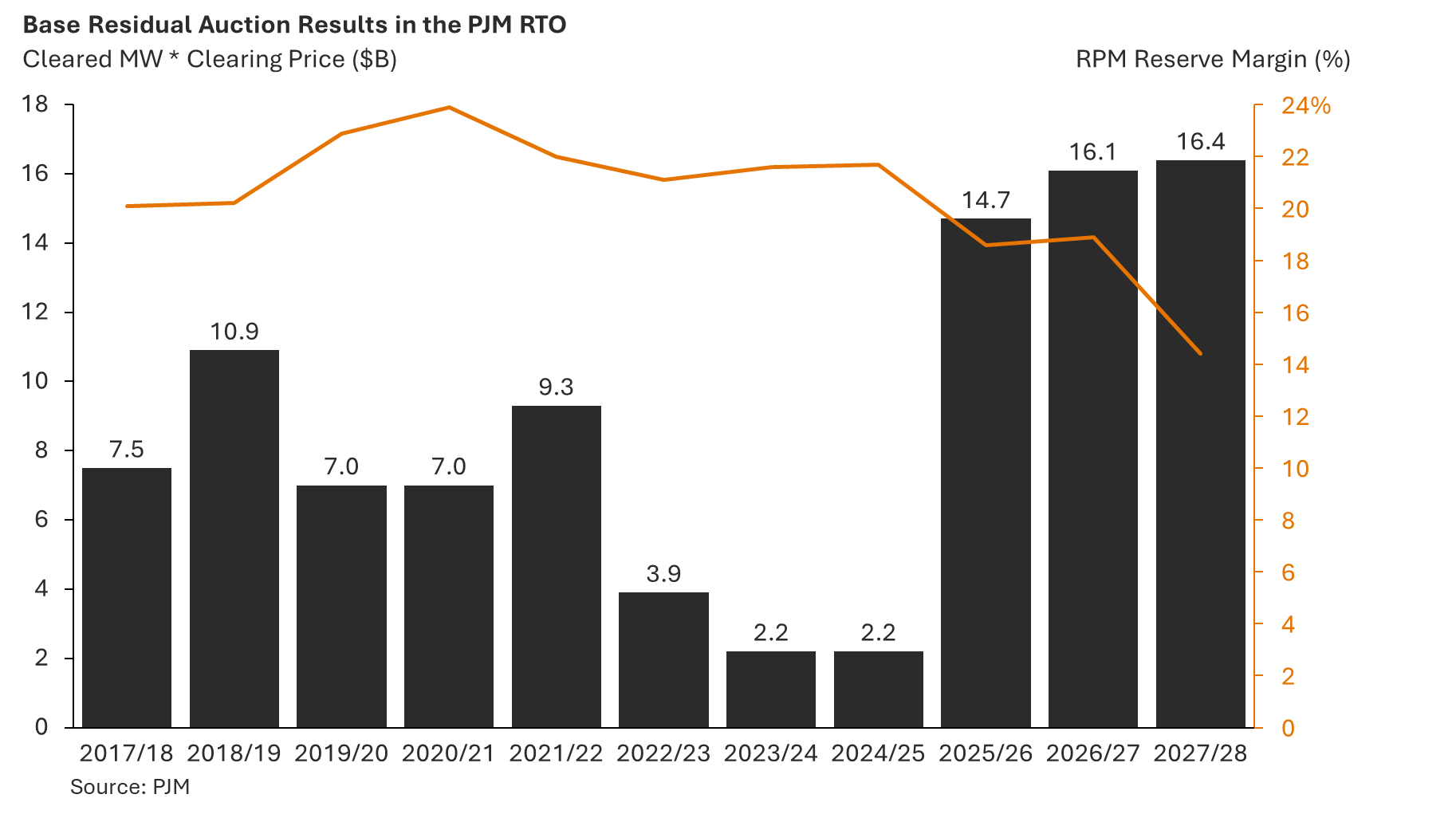

Amid this uncertainty, how should power sector stakeholders engage. Eagerly, but with discipline. The impact on the US power system today is evident, and measurable. Capacity prices in PJM’s latest capacity auction hit the price cap of $333.44/MW-day, setting record prices for the third auction in a row. PJM estimates that the capacity price would have risen to nearly $530/MW-day without the temporary price cap put in place in agreement with Pennsylvania Governor Josh Shapiro (Utility Dive). As we wrote last month: “Across the country, Democrats won with a message that focused on affordability and shifting increasing costs to large loads like data centers.” In 2025 we saw signs of how policy makers, regulators and other stakeholders will try and resolve these conflicts, and there’s more to come in 2026.

Necessity is the mother of invention

The U.S. power sector has undergone multiple transformations since the commissioning of Pearl Street Station in 1882, but changes have often been evolutionary not revolutionary. Reforms can drag for years, die in committee or be enacted and yet fail to achieve their often modest aims. There are real signals that is about to change. We are facing a historic convergence of increased prices for consumers, national security demands of AI supremacy, and continued strain on an already aging grid. As we discuss below, that has led to policy and regulatory processes that are moving at a pace we haven’t seen for generations. Large load energy demand is proving a forcing function for accelerated reform. In 2025 we began to see the fruits of longer-standing reforms, paired with a flurry of new efforts. 2026 looks to continue that trend.

Before diving into the reforms, what are we solving for? Two myths are commonly deployed in the discussions around how best to serve data centers on the grid. The first is that it needs to provide five nines availability and reliability. The second is that data centers will only use clean power when it can deliver 24/7, hence the interest in geothermal and nuclear. For starters, the grid was never built, planned, or priced to deliver five nines, and it never will be (link). Five nines is instead always achieved behind the meter. On the second point, the beauty of the grid is that it optimizes multiple different technologies to provide the lowest cost system. This includes cost-competitive clean firm resources but is not limited to them. Fix the interconnection process, and you unlock a spectrum of resources.

Now, back to the reforms. Throughout the early 2020s, increasing volumes of generator requests combined with scarce transmission to create a growing backlog of projects. By the end of 2023, nearly 11,600 projects representing 2,600 GW of capacity (2x current grid size) sat in interconnection queues with timelines from request to commercial operation averaging 5 years. This is up from just two years in 2008. FERC responded by issuing Order 2023 in July 2023, requiring that queue management be updated to a “first-ready, first-served” model. This approach includes more rigorous readiness requirements on projects, such as higher deposits and withdrawal penalties, in exchange for transparent and abbreviated timelines and “cluster studies” that streamline processes and better allocate costs. Things got worse for developers before they got better: ISOs temporary stopped accepting new generation interconnection requests as they looked to rework their processes, costs continued to spiral upwards and projects remained delayed. But there are green shoots and in 2024 the IX queue began to shrink. Over 700 GW of capacity withdrew in 2024, making it a record year for dropouts (Interconnection.fyi). A smaller queue of more viable projects.

A flurry of new actions in 2025 are set to have a more immediate impact. After decades of relative stability in how large customers connect to the grid and pay for electricity, policymakers and utilities are moving quickly to modernize large-load interconnection and tariff rules. The policies focus on two primary goals: (1) reducing speculative interconnection requests to improve load forecasting and queue management by making it much more expensive to remain in the queue, and (2) protecting existing customers from reliability risks or cost increases caused by large new loads. There are at least 65 large load tariffs either pending or in place across the country. No less than 46 of those tariffs were new this year, according to data collected by the Smart Electric Power Alliance (Latitude Media).

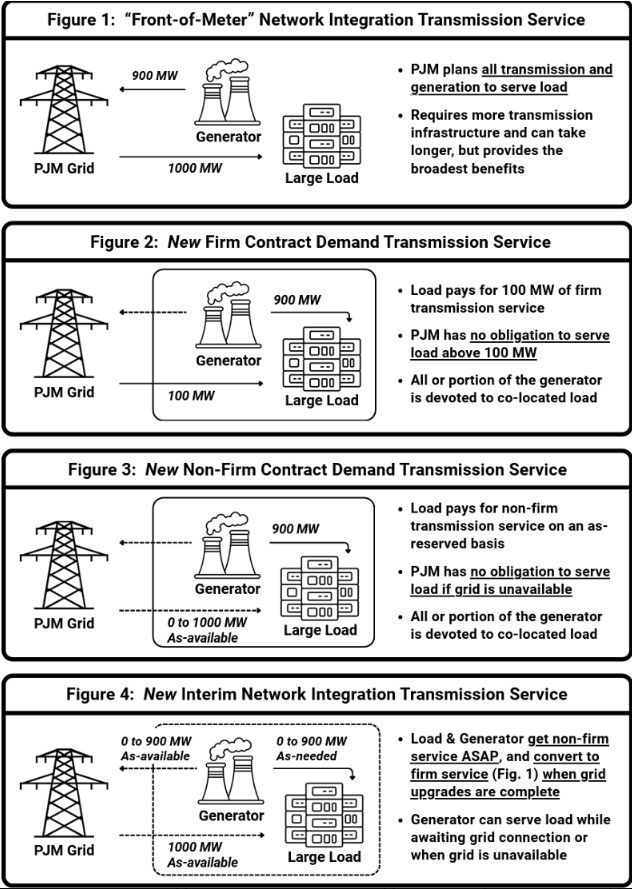

The perception of an existential AI arms race with China has imbued these initiatives with a level of strategic agency unseen in previous eras. Secretary Wright’s ANOPR directing FERC to initiate a rulemaking over the interconnections of >20MW loads has a submission deadline of April 30, 2026; FERC’s December co-location order also set a deadline of January 19, 2026 for PJM to submit an informational report including the expedited IX process. These proposals are not tweaks but are instead often fundamental changes to the way we connect generation and load to the system as the schematic below from the PJM co-location session highlights. Tight deadlines and the alignment on core issues, not just in FERC’s 5-0 vote on co-location of large loads but across the industry, on such complex topics is promising.

Queue jumping

Many of the changes to date have been defensive but in 2026 we expect large load tariffs and IX regulation to focus more on flexibility. Of particular interest is the ability to expedite IX and reduce costs by pairing load, generation and capacity. This does not require (but is complementary to) workload flexibility, is well aligned with decarbonization goals, and addresses issues of affordability.

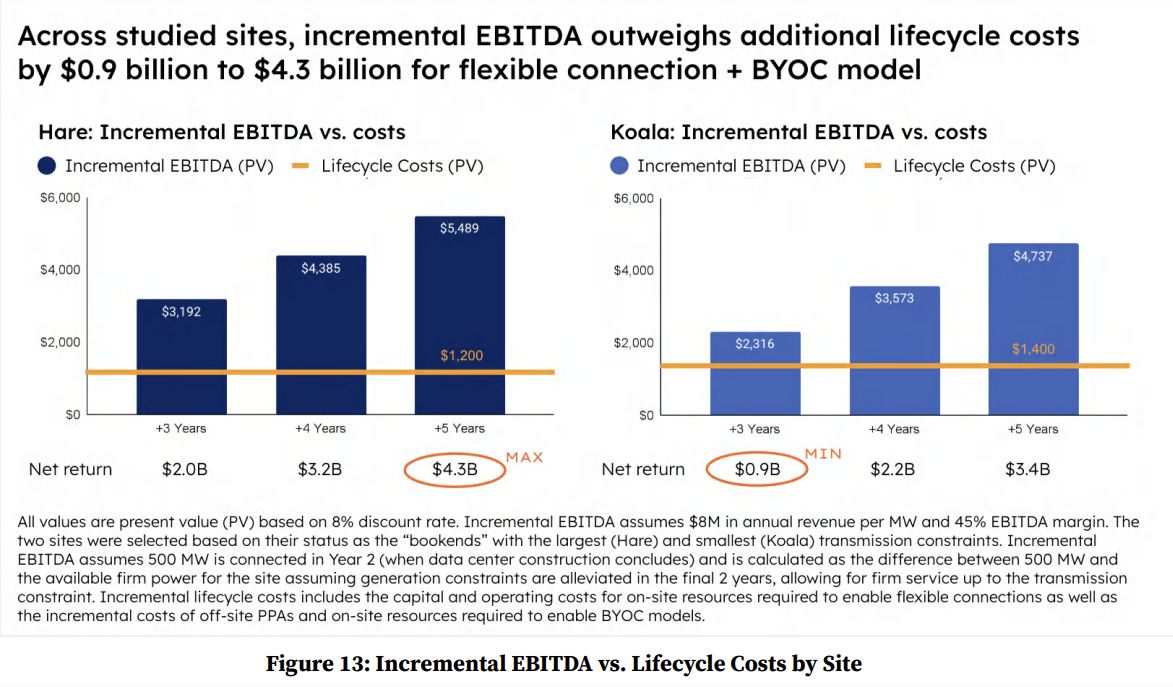

The opportunity was laid out clearly in an impressive study from Camus, encoord, and Princeton University’s ZERO Lab. Real-world transmission data and hourly simulations across six locations show how bring-your-own-capacity (BYOC) and flexible grid connections can accelerate large load interconnection.

- 3–5 years faster access to full power which drives material value creation

- >99% grid availability

- Only 40–70 hours of on-site flexibility dispatch per year

- Mitigation of system buildout and shift of remaining costs onto the data center, reducing risk for other customers

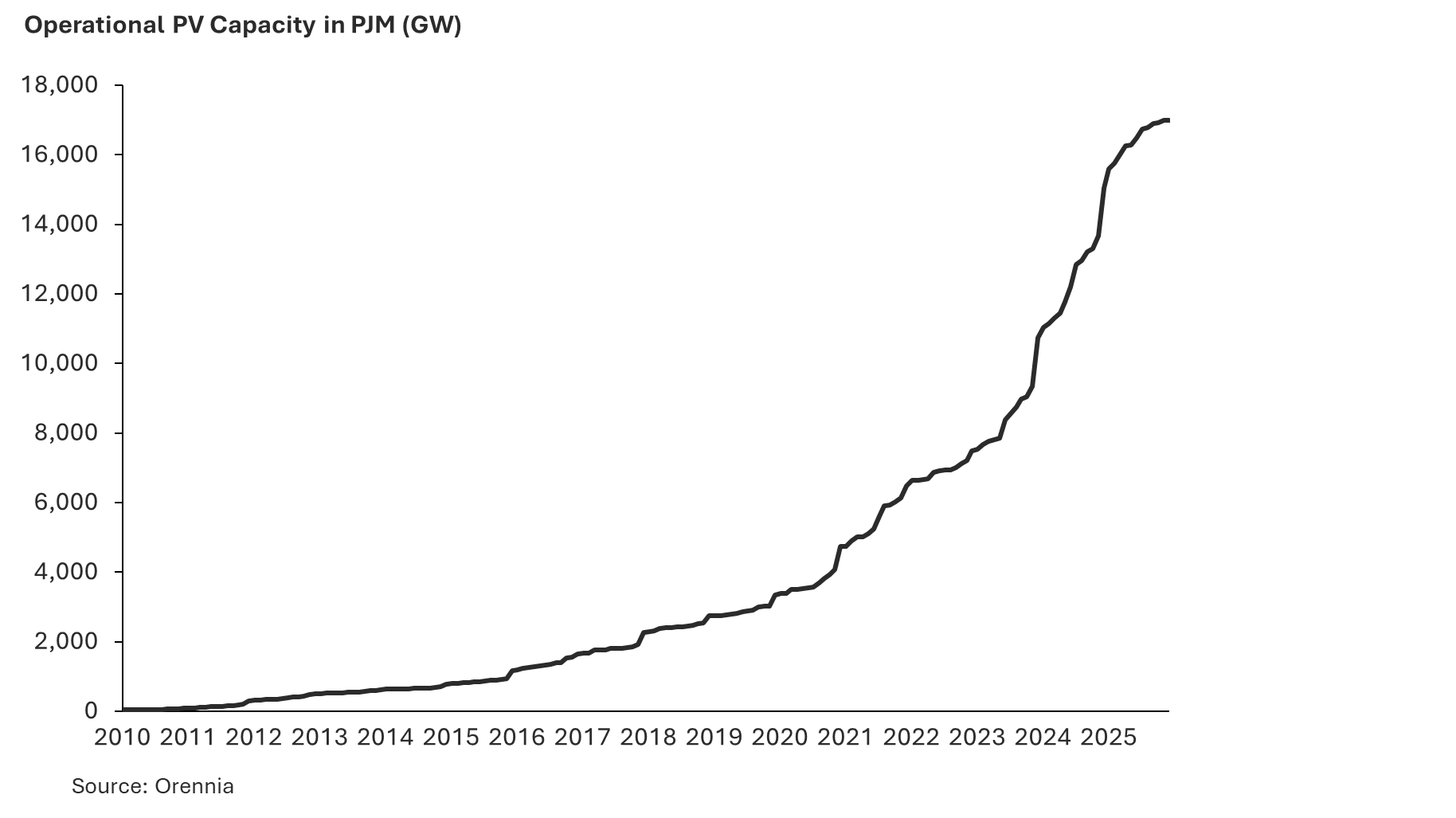

These reforms create a clear demand signal for additional generation and storage capacity. Clean energy accounted for 92% of all new U.S. power additions through November, led by solar, wind, and battery storage (Canary Media). As The Sun Also Rises in the Eastern Interconnection documents, these installations are expanding beyond ERCOT and CAISO into traditional markets like MISO and PJM. However, the pace remains insufficient for large loads, and the current state of OBBBA further muddies the picture. Consequently, major players are taking direct action, evidenced by Alphabet’s $4.75 billion end of year acquisition of Intersect Power.

The best of times, the worst of times

Despite a difficult 2025 defined by legislative hurdles and the correction of mistakes made earlier in the decade, the outlook for 2026 is bright. The industry has made great strides in establishing a new framework for the U.S. power grid that balances clean energy leadership with essential gas support, that solves the bottlenecks that have exasperated the industry for years. As our CEO David Crane laid out in September, these are the moments when opportunity is greatest.

What we're reading

Google’s Tapestry has a new white paper on How agentic AI can help grid operators speed up interconnection (link).

Howard Mark’s Is It a Bubble? memo is a handy guide to understanding and appreciating the good and the bad aspects to bubbles, and the role of debt.

VPP adoption has been a mirage for over a decade. Two papers explore the barriers that still constrain it, and ways to resolve it. Open Markets assesses how utilities continue to block Virtual Power Plants, while Energy Hub introduces the reader to The Huel’s Test: If a grid operator is presented with two resources — one being a traditional peaker plant and the other a VPP — can they tell which is which in operation?

A newly discovered series, called Measured Depth, on the natural gas markets. The author’s review of three recent reports is a good place to start.

DER Task Force annual wrap (link)

AI in 2026: A Tale of Two AIs from David Cahn (Sequoia Capital)

More newsletters

March 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreFebruary 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreJanuary 2026 Newsletter

The U.S. power grid is currently a study in constructive interference, a phenomenon where separate waves meet, their peaks align, and they merge into a single, amplified force. Capacity and generation shortages, the elevation of affordability to the center of politics, community opposition, and concerns about emissions and reliability are powerful dynamics individually. Together they may force long-lasting changes to the U.S. power systems, as proposed wholesale changes across PJM this month illustrate.

Read more