Expert view

A new way for tax credits to power communities

Ryan Miller

Principal, Private Credit

Though popular, the tax credits were historically cumbersome and complicated, which kept capital on the sidelines. Project developers were required to use complex tax equity structures to monetize these tax benefits efficiently. Tax legislation and guidance led to the emergence of novel financial structures such as the partnership flip, the sale lease-back, and the inverted lease, the execution of which became a core competency for project developers. In 2022, updates to the provisions fundamentally altered...

By the numbers

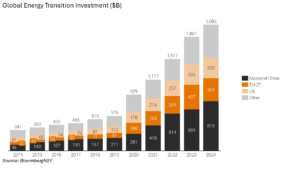

Energy transition investment is growing, albeit unevenly

Global investment in the energy transition hit a record $2.1 trillion in 2024, climbing 11% from a year earlier. But growth was uneven across regions, declining across EU-27 countries and essentially flat in the US.

Rebuilding from the LA fires

At the time of this writing, the Los Angeles fires have resulted in 29 deaths, destroyed nearly 16,000 properties, and led to insured losses of ≈$30 billion (Reuters). Estimates of the total economic losses are as high as $275 billion (AccuWeather). How we choose to rebuild today, accounting for sustainability and resilience, will determine how communities fare in the face of future events.

The beginning of the end for fire insurance?

Who decides where we can rebuild, and who pays the bill? A PoliticoPro 🔒 headline underlined the challenge ahead: “This could be the beginning of the end for fire insurance in California.” The Golden State is not alone: homeowners’ insurance is becoming more costly and harder to procure across America. From 2018 to 2022, the average claim from zip codes with the highest expected losses from climate-related events was $24,000, compared to $19,000 in lowest risk areas (link). For a data rich journey into US homeowner insurance trends, see here.

Frigid weather gives coal a brief respite

Frigid weather across much of the country in January, coupled with high gas prices, led to the highest levels of US coal-fired power production since 2019. Oil-fired power generation also increased 170% compared to January 2024 (Reuters).

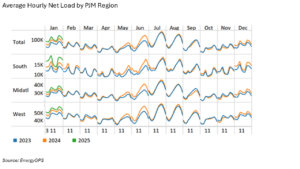

Cold weather + load growth = record peak demand

The combination of extreme cold weather and structural load growth pushed PJM’s peak load to a high of 144.4GW on January 22. Load profiles across the region are also shifting as more solar capacity comes online.

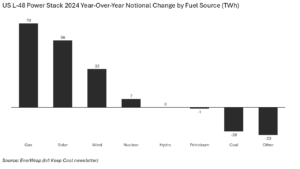

US natural gas generation on the rise

Activity in January clearly only shows a partial picture. Full year 2024 data shows natural gas generation increased more year-over-year than any other power source (Ener Wrap, h/t Keep Cool). US GHG annual emissions remained largely flat, declining just 0.2% year-over-year after steep declines in 2023 (Rhodium Group, Canary Media).

Global LNG dynamics

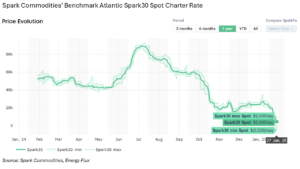

Liquefied natural gas (LNG) liquefaction capacity could expand by 50% from 2024 to 2028, potentially tipping the market into oversupply (see What we’re reading). Meanwhile, the cost of chartering ships for transporting LNG fell to negative $5,500/day due to an influx of modern newbuild vessels entering the market and construction delays at new LNG supply projects, among other things (EnergyFlux). With natural gas having a moment in the US, keeping an eye on global LNG dynamics is advised.

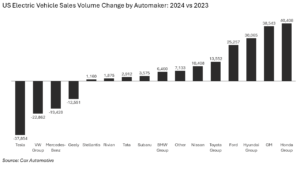

The EV market is no longer Tesla’s alone

US battery electric vehicle sales rose 7.3% year-over-year to 1.3 million (Cox), with another 300,000 or so plug-in hybrids (Argonne National Labs). Tesla remains the market leader, but competition is afoot: Tesla’s annual sales declined in 2024 for the first time in more than 10 years, decreasing 1.1% from 2023 levels (Bloomberg🔒, Heatmap🔒). From a low base, relative sales from Honda, GM, Ford, and Hyundai are, by contrast, up (Bloomberg🔒). Globally, EV sales grew 25% year-over-year, propelled by a 40% increase in sales from China (Rho Motion).

Policy & regulatory highlights

While we continue to believe the core set of incentives that the infrastructure transition relies on remain intact and politically durable, much remains unknown and the new US administration is certainly keeping policy, legal, and regulatory analysts busy. Be forgiving if the below is already out of date at the time of reading.

Final 45V ruling, at long last

In the final days of the Biden administration, the US Treasury issued final rules on the 45V hydrogen production tax credits. The final rules marked a loosening of the initial guidance from December 2023 but remain broadly tied to the concept of the three pillars. Some technologies, and specific regions, came out better than others (Canary Media, Treasury, Heatmap🔒). Green hydrogen could still play an important role in the energy transition, but likely a narrower path than envisaged in 2022.

Biden admin’s final funding spree

The Biden administration had a busy final few weeks, and 84% of the Inflation Reduction Act’s allotted funding has now been obligated (Reuters). It remains to be seen whether all these commitments will hold. The latest fundings include $22 billion to help eight utilities across the US with energy infrastructure upgrades (Canary Media); $15 billion to PG&E to support transmission upgrades and renewables development (DOE); $1.8 billion for a long-duration air energy storage system in California (Electrek); and $1.7 billion to SAF producer Montana Renewables (DOE). These bring the Loan Programs Office’s grand total of committed project investment over the last four years to $107.6 billion (LPO).

Out with the old, in with the new

President Trump issued a flurry of energy-focused executive orders in his first weeks (CTVC, Norton Rose Fulbright). Among them, he sought to pause IRA disbursements (PoliticoPro🔒), to withdraw from the Paris Agreement (Axios), and he declared a national energy emergency to bolster domestic energy production (White House, Heatmap🔒, PoliticoPro🔒). The Department of Interior issued a 60-day suspension which largely prohibits its staff from permitting new renewables projects on public land (DOI). Plenty of mixed signals here, or at least actions misaligned with the stated goals (Equal Ventures).

Bipartisan support for data centers

In a rare show of consistency between the two administrations, Trump also announced up to $500 billion in private sector investment for data centers and their energy infrastructure from a joint venture called Stargate, whose founding companies include OpenAI, SoftBank, and Oracle. If the companies involved can indeed fund the project… the data centers will reportedly be powered in part by solar and batteries (TechCrunch). This comes shortly after Biden issued an executive order that opens federal lands to the construction of data centers and requires those data centers to be powered by clean electricity (E&E News🔒, PoliticoPro🔒).

State & local updates

New York state enacted a law that will charge companies for their greenhouse gas emissions, with fines going toward a state fund for sustainable infrastructure projects (AP).

New York City, meanwhile, enacted its congestion pricing policy, which charges drivers up to $9 to enter parts of Manhattan during peak hours to reduce traffic, improve air quality, and fund city infrastructure upgrades (Axios). Real-time congestion trackers indicate the policy is delivering on its promise so far, with some commutes halved within its first week in effect (link, link).

The Public Utility Commission of Texas scrapped its proposed $1 billion performance credit mechanism (aka the Texas Capacity Market). The mechanism would have allowed incentives to power ERCOT generators during peak grid demand periods but has been a dead man walking for some time (Utility Dive).

What we're reading

Generate CEO and Cofounder Scott Jacobs’ open letter to climate and energy transition leaders (link)

Nat Bullard’s annual decarbonization deck (link)

A few of my favorite articles on DeepSeek (link, link, link, link, link)

Sticking on the theme of data centers and AI demand: The power and the glory on data centers (link) and The Hidden Risks of Overestimating AI’s Power Needs (link)

Volta Foundation’s 2024 Battery Report (link)

Grid Status: Batteries have reshaped ERCOT’s ancillary services procurement (link)

But it’s challenging times for many battery suppliers: a summary of the Korean battery industry crisis (link)

Is comparative advantage valid in a geopolitical world? (link)

Peak car revisited, and revised (link), the greenwashing of robotaxis (link)

Sightline Climate’s climate tech VC and growth equity investment trends report (link)

Sizing up the LNG glut, part 1 (link)

Norton Rose Fulbright 2025 Cost of Capital Outlook (link)

Beginning of year predictions already feel an age away, but some highlights in case you missed them. From Equal Ventures (link), Exponential View (link), Michael Cembalest (link), and Professor Galloway (link).

More newsletters

March 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreFebruary 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreJanuary 2026 Newsletter

The U.S. power grid is currently a study in constructive interference, a phenomenon where separate waves meet, their peaks align, and they merge into a single, amplified force. Capacity and generation shortages, the elevation of affordability to the center of politics, community opposition, and concerns about emissions and reliability are powerful dynamics individually. Together they may force long-lasting changes to the U.S. power systems, as proposed wholesale changes across PJM this month illustrate.

Read more