Policy Notes

Tariff Updates: From Chaos to Convention

The future of President Trump’s “Liberation Day” tariffs hit a significant obstacle last week. On May 28, the U.S. Court of International Trade (CIT) struck down core pieces of the so-called reciprocal tariffs, ruling that the President had overstepped his authority under the International Emergency Economic Powers Act (IEEPA) of 1977. Some of President Trump’s tariffs were unaffected by the ruling, including restrictions on auto imports and steel. Many others were significantly curtailed including the 10% baseline tariffs and those targeting fentanyl-related imports from countries like China, Canada, and Mexico.

This still has some way to go before we know how it ends. However, the initial court ruling makes it more likely the U.S.’s approach to trade will ultimately move from the chaos of the last two months to a more conventional process that the industry has a decade-plus experience navigating. This makes for a less volatile investment landscape, even with heightened tariffs compared to January.

House Tax Bill: From Politics to Practicalities

The House passed a sweeping tax bill that includes major changes to clean energy tax credits. It marks a significant step in GOP lawmakers’ efforts to move the tax legislation through Congress, but nothing is final and there is a long way to go before anything is signed into law. The tax bill is now with the Senate, meaning Congress still has time to consider the U.S.’s power needs and design policies accordingly. Policy will be most effective if it includes:

- Meaningful and predictable incentives that help investors make decisions about allocating capital and give developers the certainty necessary to build projects;

- “Commence construction” requirements that give investors certainty around the tax credit’s value prior to allocating capital;

- Flexibility, such as that offered by transferability – that streamline investment processes and maximize uptake.

Our full article looks at the House bill’s implications against the backdrop of the current U.S. power system, where meeting rising demand is an imperative.

At times like these, it is natural for all eyes to focus on Washington D.C. Remember though that investment and procurement decisions are made across the U.S. by companies large and small, based on their needs. A core ethos at Generate is that customers’ needs drive markets. Our expert view this month explores how corporates are making energy and infrastructure business decisions, and what that means for the broader state of corporate decarbonization.

Expert view

Looking beyond the headlines of corporate decarbonization

Gopal Vemuri

VP, Development and Origination

Many of today's headlines about the state of corporate decarbonization paint a bleak picture, in which the world’s most influential companies are pulling back from their net zero ambitions (Harvard Business Review, Financial Times, Reuters). Alongside a broader backlash against ESG, companies who remain committed to decarbonization are also finding the process more difficult than anticipated, due in part to the capital required and the complexity of reducing scope 1 emissions. The Science Based Targets Initiative removed 230...

By the numbers

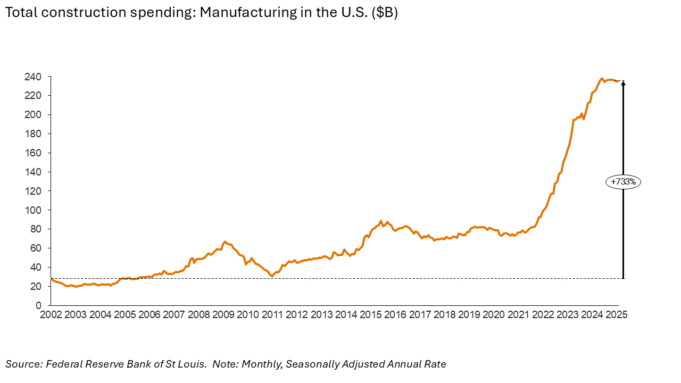

U.S. manufacturing investment is slowing, but still high

Despite some manufacturers across the U.S. pausing or canceling projects amid lingering tariff pressures and federal policy uncertainty, total investment in new plants remains robust. Many projects were already too far along to halt, while others retain conviction in the need for domestic manufacturing. By March 2025, U.S. manufacturing construction spending had climbed to $230 billion, all of which will demand vast quantities of power.

Nat Bullard’s recent Halcyon dispatch teases this out nicely by focusing on one high-profile example: the BlueOval SK battery park, a $5.6 billion joint venture between Ford Motor Company and Korea’s SK Innovation. Sprawling across 1,500 acres and targeting 80 GWh of annual battery output, the plant alone will draw a peak 260 MW in summer and 225 MW in winter once fully built out. It’s not just data centers that need power.

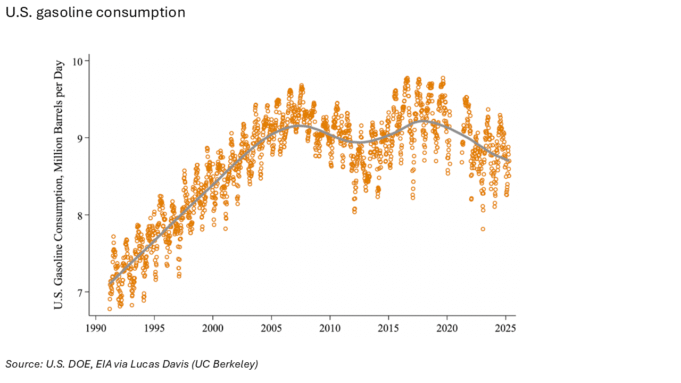

U.S. gasoline sees sustained slowdown

After decades of steady gains, U.S. demand for gasoline is now on a six-year, 5% decline. This is due not only to increasing EV sales, but also the increasing number of hybrid cars on the road and improving fuel economy for combustion engine vehicles (link).

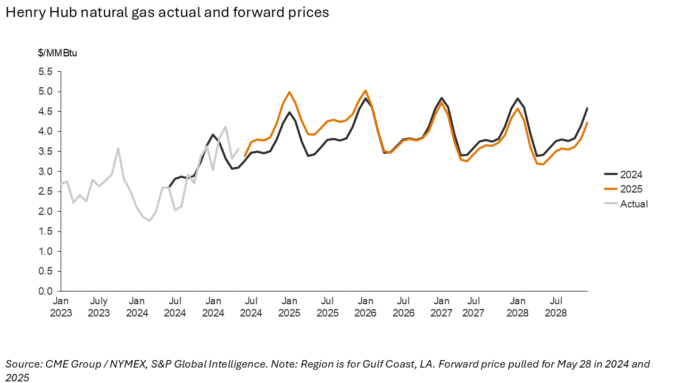

Natural gas industry braces for price volatility

Natural gas analysts at S&P Global Commodity Insights expect volatility in gas prices to increase in the coming years due to a combination of retiring coal-fired power generation capacity, spending discipline among producers, and a change in how gas storage is used. Analysts also raised their US natural gas price outlooks for this year and next on the heels of first-quarter earnings, expecting tighter market conditions because of factors such as rising gas demand and slower production growth.

As of May 15, Henry Hub forwards for the balance of 2025 were $3.93/MMBtu on average, with the 2026 strip at $4.33, according to Platts data. In its latest forecast published May 6, the EIA projected $4.10/MMBtu Henry Hub in 2025 and $4.80/MMBtu in 2026, higher than the $3.10 and $4 gas forecast in January (S&P Global Intelligence).

What we're reading

Harry Benham on oil companies exiting energy (link)

Financial Times: Europe won’t displace US economic power any time soon (link)

Supporting LNG & AI: Embrace the IRA or be prepared to pay (link)

We deliberately didn’t include anything on the blackouts in Iberia since it took place as we were publishing, and there was too much speculation, not enough detail. Now that the dust has somewhat settled, here’s a helpful read on what we know and the implications for the U.S. (link). And here’s one on why the reaction to the blackout was sadly predictable (link).

Swiss Re report on expected US insured losses for 2025 (link)

Why are solar panels and batteries from China so cheap? (link)

How China’s powerslide is driving the global green electricity transition (link)

Insurance costs for EVs (link)

Tariff scenarios for taxing times (link)

Michael Liebreich on decarbonizing the last few percent (link)

The energy boom’s labor bust (link)

Electrotech, not cleantech (link)

More newsletters

March 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreFebruary 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreJanuary 2026 Newsletter

The U.S. power grid is currently a study in constructive interference, a phenomenon where separate waves meet, their peaks align, and they merge into a single, amplified force. Capacity and generation shortages, the elevation of affordability to the center of politics, community opposition, and concerns about emissions and reliability are powerful dynamics individually. Together they may force long-lasting changes to the U.S. power systems, as proposed wholesale changes across PJM this month illustrate.

Read more