Expert view

The middle-market 0pportunity

Logan Goldie-Scot

VP, Research and Impact

Looking ahead, to meet global climate targets, annual spending across energy, transport, and the built environment needs to increase fivefold through to 2030 (Figure 1). The required scale-up is even greater in areas like industrial processes where investment has yet to really get off the ground. The trillions of dollars of investment both decarbonize and transform the system we know today. This results in a very different deal profile compared to earlier waves of infrastructure investment....

By the numbers

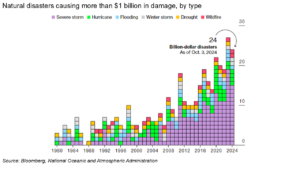

Back-to-back hurricanes Helene and Milton battered the Southeastern US this month, causing more than 240 deaths and prompting debates around climate change, resilience strategies, relief funding, and insurance premiums, especially in the run-up to the US presidential election. Each storm is likely to have caused more than $50 billion in damage, ranking them among the costliest-ever US storms (Fortune 🔒). Ninety-five percent of Hurricane Helene’s damage was not insured (AP), while FEMA spent half its annual budget in just eight days (PoliticoPro 🔒). A Berkeley Lab report estimates that climate change caused Hurricane Helene to have 50% more rainfall in Georgia and the Carolinas and made rainfall more than 20x more likely in these areas (link).

The last month brought a stream of nuclear investment announcements as Big Tech companies’ search for clean power continues. Amazon plans to install four 80 MW small modular reactors (SMRs) near its data centers in Washington state in partnership with Energy Northwest and X-energy. The projects are expected to come online in the early 2030s. Amazon is also leading X-energy’s $500 million funding round (CTVC, Amazon). Google agreed to buy power from seven planned SMRs from startup Kairos Power via PPAs, with targets to generate 500 MW of nuclear power capacity. The projects are expected online between 2030 and 2035 (WSJ). Microsoft signed an agreement to reopen the Three Mile Island nuclear plant through a 20-year 800 MW PPA, with aims to have the plant operational again by 2028 (E&E News).

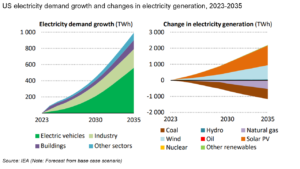

US electricity demand is projected to increase 25% over the next decade according to estimates from the IEA’s new World Energy Outlook, with EV adoption accounting for almost 60% of the demand growth (IEA). Despite their significance for cloud computing providers and prominence in media headlines, the IEA expects data centers to account for a relatively modest share of this electricity demand increase, though their high concentration in certain areas could still cause local grid constraints. Nearly 60% of US electricity generation is expected to come from renewables by 2035, up from 22% last year.

US power plants saw a 7.2% year-over-year decrease in greenhouse gas emissions in 2023, reaching their lowest level since mandatory reporting began in 2010 (EPA). Shortly after the US EPA released these latest data points, the US Supreme Court decided not to block the EPA’s restrictions on power plant emissions, though the rule’s longer-term future is far from certain (Heatmap 🔒).

EV sales in the US grew 11% year-on-year, reaching record highs for both volume and market share (Cox Automotive). My former BloombergNEF colleague Colin McKerracher recorded a great podcast on this earlier this month if you want to know more (Cleaning Up).

PacifiCorp, Oregon’s second-largest electricity supplier, said only about 20% of the load requested by large customers from 2020-2023 materialized. The company released a proposal to protect its ratepayer base from paying more due to inaccurate forecasts from large customers, though the proposal is opposed by Meta and two industry groups (Portland Business Journal 🔒, LinkedIn). These disputes are popping up across the country, such as in Ohio (Utility Dive, Washington Post 🔒).

North American solar PPA prices on average jumped 10.4% year-over-year to $56.58/MWh in the third quarter and rose 5.4% from the second quarter of 2024 (LevelTen, CapIQ 🔒).

Policy & regulatory highlights

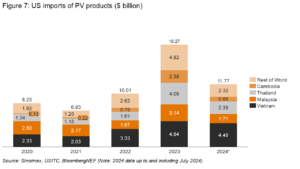

The US Department of Commerce announced new tariffs for solar panels from Southeast Asian countries aimed at preventing Chinese companies operating in Vietnam, Cambodia, Malaysia, and Thailand from circumventing existing US tariffs. Rates ranged from 0.14% (de minimis) to 292.61% (Clean Energy Associates). As we’ve covered in previous newsletters, tariffs have yet to deter the import of solar cells and modules into the US: January to July 2024 saw $12 billion worth of PV imports, higher than full year totals in any year other than 2023.

The Independent Market Monitor released its latest State of the Market report (link), which recommends ending 4CP Pricing. Designed to account for a customer’s electricity consumption during peak demand periods, 4CP can effectively incentivize the adoption of C&I demand response but there are concerns that the setup shifts costs from industrial large-business customers to residential customers and small businesses (Texas Power and Energy Newsletter).

Sticking with ERCOT, analysis from Aurora Energy Research found that that wholesale energy price spikes in 2023 were primarily driven by weather and thermal outages, not ancillary services as previously argued by the Independent Market Monitor (Aurora).

California Governor Gavin Newsom enacted a new climate disclosure law that requires companies operating in the state with annual revenues exceeding $1 billion to disclose their Scope 1, 2, and 3 greenhouse gas emissions annually. This adds teeth and accountability to the state’s prior climate disclosure law, as California doubles down despite the SEC’s climate disclosure law being put on what is likely an indefinite hold (ESG Today).

The US Department of Energy announced another $2 billion in funding for 38 grid transmission projects across the country in its third round of awards from the Grid Resilience and Innovation Partnerships Program (DOE). This builds on the $1.5 billion for four transmission projects the DOE announced earlier in the month through the Transmission Facilitation Program (DOE).

In more transmission news, FERC approved CAISO’s interconnection request to limit interconnection entries, with opponents of the measure arguing that it ends open access to California’s electricity market (LinkedIn). Integrating LSEs into the process is not necessarily a bad thing however and if it doesn’t work, in the words of a CAISO rep at a recent conference “This is a privilege that can be taken away.”; the ERCOT Public Utility Commission approved its own reliability plan (Utility Dive), MISO advanced a $21.8 billion regional transmission portfolio (Utility Dive), and California passed a new law requiring utilities to evaluate grid-enhancing technologies at least every two years in transmission planning (Watt-Transmission).

Emerging technologies

The US Department of Interior approved new measures to simplify regulations for the development of geothermal projects on public lands and approved Fervo’s 2 GW next-gen geothermal project in Utah (Infralogic, DOI).

British energy company Drax announced plans to invest up to $12.5 billion in biomass power plants with carbon capture and storage (BECCS) in the US in the next decade. Drax has already secured 11 deals with eight companies planning to purchase carbon removal credits generated from the projects (Carbon Herald).

ExxonMobil signed the US’s largest offshore CCS deal with the state of Texas. The oil and gas company will have access to 270,000 acres of land under the Gulf of Mexico’s surface to sequester and store carbon dioxide (ESG Dive).

The US Department of Energy selected 23 carbon storage projects within its Carbon Validation and Testing program, with a total of $518 million up for grabs (NPM 🔒).

More setbacks for the US green hydrogen market as both Hy Stor Energy and Intersect Power moved to pause or cancel the green hydrogen components of their upcoming projects (Canary Media, NPM 🔒). The market could see clearer signals soon, however. The Treasury Department said it will finalize the long-awaited guidance for the 45V hydrogen tax credit before the end of the year (Heatmap 🔒).

Long-duration energy storage startup Form Energy raised a $405 million Series F funding round for its iron-air battery technology. The company aims to develop projects capable of storing energy for 100 hours, though its technology is in the early stages of commercialization (Canary Media). In another boost, Pacific Gas & Electric (PG&E) issued a request for offers seeking the purchase of long-duration energy storage to provide system-level net qualifying capacity by June 1, 2028 (NPM 🔒).

Low-carbon cement startup Sublime Systems raised $75 million from two of the world’s largest cement producers, CRH and Holcim (Bloomberg 🔒).

The US Department of Energy announced two conditional commitments to sustainable aviation fuel (SAF) producers: Gevo Net-Zero 1 will receive $1.5 billion to help finance a first-of-its kind facility in South Dakota that uses corn starch as low-carbon feedstock (DOE), while Montana Renewables’ $1.4 billion loan will help fund a facility that produces fuel from vegetable oils, fats, and greases (DOE).

What we're reading

Why the transition to net-zero needs more flexible capital, from Generate CEO Scott Jacobs and CalSTRS CIO Scott Chan (link)

Generate’s Christian Okoye on our FOAK problem and whether data can be part of the solution (part 1, part 2, part 3)

Nick van Osdol’s dos and don’ts for how to talk about climate change and weather (link)

RMI’s sustainable aviation fuel market outlook (link)

Drilled: Conspiracies thrive in a crisis (link)

US CCS Ladder (link)

Gregor Macdonald’s Substack on the contrasting approaches and implications to phasing out coal in the UK and the US (link)

International Renewable Energy Agency’s latest report on renewable power generation costs. One key finding: 81% of the new renewable energy capacity added in 2023 produced cheaper electricity than fossil fuels (link)

US DOE’s transmission impact assessment (link). Tldr: more transmission results in more affordable, more reliable and cleaner power.

US DOE: Pathways to commercial liftoff for advanced nuclear (link)

Wood Mackenzie on the demand dilemma facing the US power industry (link)

Climate on the ballot: the stakes of the upcoming U.S. elections. A pair of Baringa reports, the first of which looks at the federal-level implications and the second scores each state’s climate policy credibility and durability (link). h/t Carbon Risk.

Forget repowering… just move into your old turbine (link)

More newsletters

March 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreFebruary 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreJanuary 2026 Newsletter

The U.S. power grid is currently a study in constructive interference, a phenomenon where separate waves meet, their peaks align, and they merge into a single, amplified force. Capacity and generation shortages, the elevation of affordability to the center of politics, community opposition, and concerns about emissions and reliability are powerful dynamics individually. Together they may force long-lasting changes to the U.S. power systems, as proposed wholesale changes across PJM this month illustrate.

Read more