Expert view

Why the infrastructure transition needs private credit

Katherine Treuer

Principal, Generate Credit

Where traditional investors have struggled to provide the adaptability needed to navigate turbulent economic landscapes, private credit has offered bespoke, personalized capital lifelines. This flexibility has proved particularly vital for funding solutions aimed at big, complex challenges like the transition to sustainable infrastructure, where much of the hardship lies in mobilizing and scaling physical assets, commercializing emerging technologies and opening new markets. At Generate, we view credit as an essential piece of the sustainability funding equation,...

By the numbers

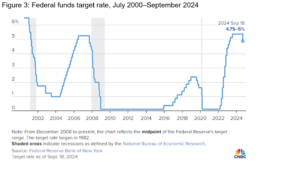

The US Federal Reserve cut interest rates by nearly half a percentage point – from the 20-year high of 5.3% to 4.9%. The move, which is expected to be the first of several rate cuts, signals a return to a more stable economic landscape as inflation rates slow (NYT 🔒). The ten year treasury rate however went up to 3.73%, suggesting the market remains concerned about long term risks, notably inflation.

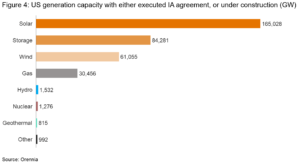

In the first half of 2024, some 27.5 GW of new natural gas power capacity was announced, largely in response to more bullish demand forecasts. If announcements continue at this clip for the rest of the year, it will break recent records for the fossil fuel (Bloomberg 🔒). Tight supply will lead to some new gas build and delays in the retirement of many gas and perhaps even coal assets. Onsite power assets that can be installed relatively quickly look more attractive in this environment. However, securing financing and building new utility-scale thermal asset remains no mean feat in many markets. Even in ERCOT, with soaring forecast demand and a supportive regulatory environment, it took a $5 billion low interest loan and grant program to spur tangible commitments. Newly announced gas projects must also get in line, the start of a multi-year process. Let’s look at the queue: there is 30 GW of gas generation with an executed interconnection agreement or under construction, i.e. at later stages of the process, compared to 310 GW of wind, solar, and storage (Orennia). If you expand the search to earlier-stage projects in the queue, wind outnumbers gas 3:1, and there is roughly 10x more capacity for solar and storage each. Large scale natural gas is clearly having a moment, but it may be a fragile one. In addition to wind, solar and batteries, the first commercial projects for other clean power technologies such as thermal energy storage and geothermal are due online over the next 24 months. They are earlier stage, for sure, but suggest natural gas will face more not less competition in the years to come, especially as interconnection reforms accelerate (Utility Dive).

Two hundred people oversee over $200 billion in annual utility spending. That’s a billion dollars per person. This gem came from a Volt’s podcast on the role that public utility commissions play across the country, and how to change the way they work.

Volvo walked back its commitment to offering 100% EVs by 2030, instead committing to delivering 90% electric or plug-in hybrid vehicles by the end of the decade. CEO Jim Rowan attributed the reversal to market forces, insufficient charging infrastructure, and waning customer demand (Reuters).

Since the passing of the Inflation Reduction Act (IRA) in 2022, the US’s solar module manufacturing capacity has increased 4x to 31 GW (Renewables Now).

BloombergNEF’s latest cost estimate for an electrolyzer in 2050 is 3x what it had forecast in 2022.

Policy & regulatory highlights

The Biden-Harris administration announced $7.3 billion in IRA funding as part of the new Empowering Rural America program to help rural electric cooperatives transition to and distribute clean energy (White House). The administration also announced plans to expand solar programs in disadvantaged communities (DOE) and invest $430 million to upgrade hydropower infrastructure across the US (DOE).

Sixty-six US lawmakers signed a letter to the US Treasury Secretary arguing in favor of upholding the strict rules for the IRA’s 45V hydrogen tax credit (link).

US steelmaker Cleveland-Cliffs’ CEO said he was considering abandoning a $500 million grant from the Biden administration amid industry headwinds, a misalignment in incentives, and a remaining gap between the costs of producing low-carbon commodities and the market’s willingness to pay (PoliticoPro 🔒). Although the company has since released a statement expressing its full commitment to the project, steel is not the standout here: one in four recipients of Biden administration grants to support the US battery supply chain has returned the funds (The Electric 🔒).

California’s regular legislative session ended without any progress toward mitigating the state’s utility bill cost crisis (Canary Media).

The US Bureau of Land Management approved two pivotal projects for accelerating renewable energy in Nevada: NV Energy’s Greenlink West transmission project and Arevia’s $2.3 billion solar and battery storage project (Utility Dive).

Emerging technologies

After several downbeat stories on battery manufacturing startups, some positive news: 24M raised $87 million in Series H funding (FINSMES).

Bank of America provided $205 million to North Dakota-based carbon capture plant Blue Flint Ethanol, a subsidiary of Harvestone Low Carbon Partners, in a first-of-its-kind tax credit deal (WSJ).

Direct air capture (DAC) startup CarbonCapture abandoned plans to build its Wyoming-based DAC mega facility. The facility, which was intended to be the world’s largest, was scrapped due to insufficient access to carbon-free energy amid competition for power from data centers (CTVC). In other DAC news, Occidental’s 1PointFive secured up to $500 million in funding from the US Department of Energy (Reuters).

Google is procuring DAC deals at the low price of $100 per ton, made possible in part because Google is using the IRA’s 45Q tax credit and paying for much of the carbon capture upfront. Google has purchased 100,000 tons of carbon removal and storage from Holocene, delivered by 2032 (Latitude Media, PoliticoPro 🔒).

The US EPA launched an enforcement action against ADM in response to a leak at the agriculture company’s underground carbon sequestration facility, the first such facility in the US (PoliticoPro 🔒).

The carbon removal marketplace Nori announced plans to shut down after operating for seven years and raising $17 million from investors. The startup cited challenges with fundraising and slowdowns in the voluntary carbon market (Carbon Herald).

Geothermal company Fervo Energy announced the close of a $100 million bridge loan from X-Caliber Rural Capital to support the development of its Cape Station project in Utah (Utility Dive). Baseload Capital raised €53 million in a Series B funding round to scale up geothermal energy (Sunya).

The Department of Interior will hold an offshore wind energy lease sale for sites along the Gulf of Maine, with a potential capacity of 13 GW (DOI). The Biden-Harris administration approved its 10th commercial-scale offshore wind project (PoliticoPro 🔒). Massachusetts and Rhode Island selected more than 2,800 MW of wind power capacity from three New England projects, a result of the US’s first multi-state procurement collaboration (Electrek). BP is selling its onshore wind business (Bloomberg 🔒).

What we're reading

Brian Potter’s Substack on why America is bad at building ships, but then, it always has been (link, H/t Benedict’s Newsletter)

The Great China Blitzkrieg (link)

Intersect Power CEO Sheldon Cooper’s latest on data centers and decarbonization: Should power go to data centers, or data centers to power? (link)

Lynne Kiesling’s Substack on whether Vaclav Smil is right about the physical limitations to innovation (link, link)

A simplified and clear take by RMI on the primary energy value, by dividing everything into heat or work (link). We’ve gone as far as fire can take us.

Orennia’s Rule of 40 chart (link)

Carbon capture and storage (CCS) is misunderstood (link)

A report on the state of the electric school bus market, which shows California well ahead of the rest of the US in deploying e-school buses (link) as well as Canary Media’s piece on how the country’s largest electric school bus fleet will also feed the grid (link)

McKinsey’s Global Energy Perspectives (link)

Hydrogen Council’s 2024 Insights report (link)

EIA’s latest Short-Term Energy Outlook (link)

A report on how to efficiently connect new generation to the grid (link)

If you’ve made it this far, enjoy this video on fluidized sand. Fluidized beds are used in a number of industrial processes and it is a key storage medium for many thermal energy storage technologies (link). It turns out you can also use it in a hot tub.

More newsletters

March 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreFebruary 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read moreJanuary 2026 Newsletter

The U.S. power grid is currently a study in constructive interference, a phenomenon where separate waves meet, their peaks align, and they merge into a single, amplified force. Capacity and generation shortages, the elevation of affordability to the center of politics, community opposition, and concerns about emissions and reliability are powerful dynamics individually. Together they may force long-lasting changes to the U.S. power systems, as proposed wholesale changes across PJM this month illustrate.

Read more