By the numbers

The opportunity

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

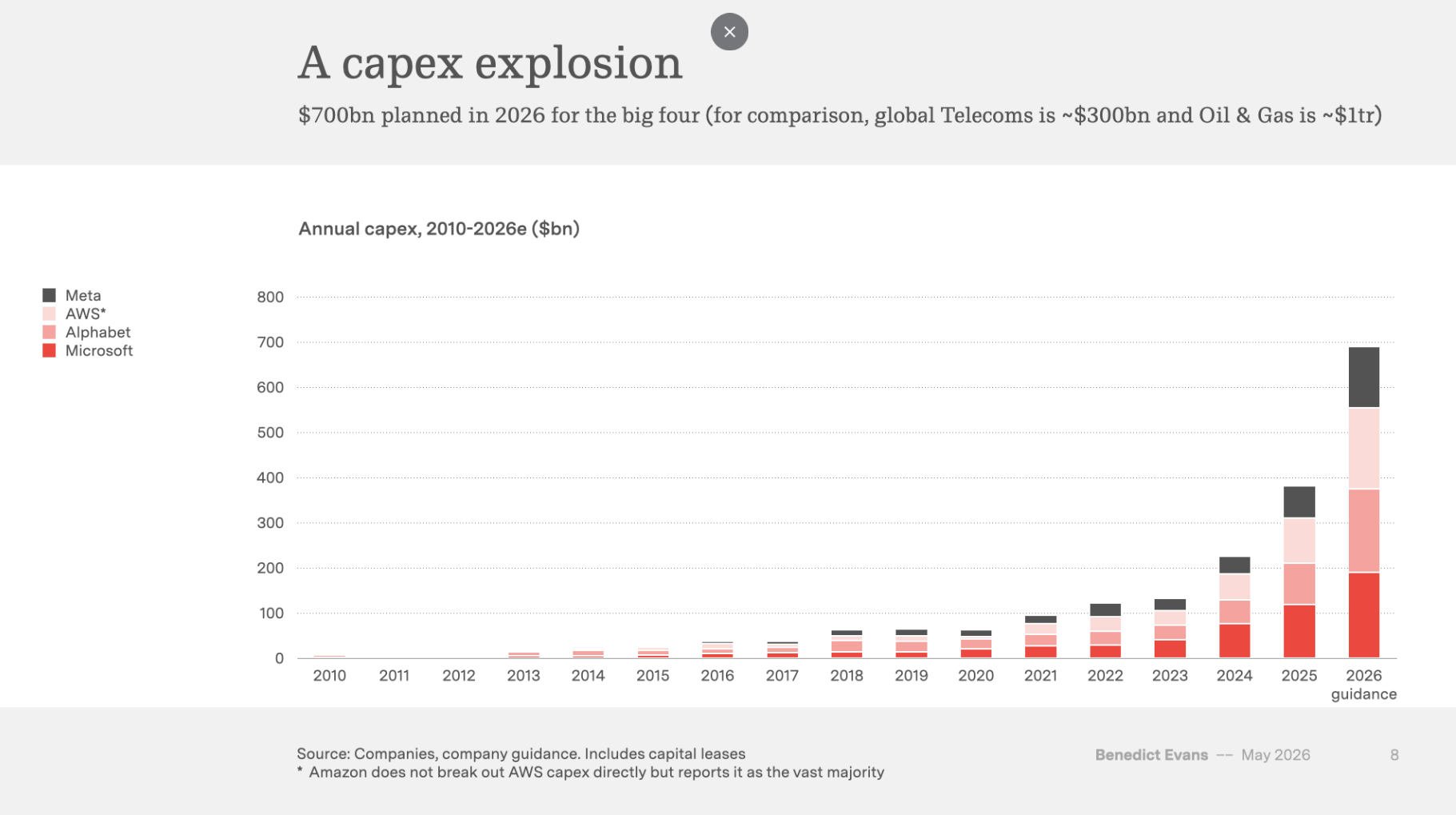

Alphabet, AWS, Meta and Microsoft are planning roughly $700B of capex in 2026, up sevenfold from just five years ago. To support this capex, these firms are raising funds at scale from both the private and public markets. In early June, Alphabet announced an equity raise that was quickly upsized to roughly $85B; a few days earlier, Anthropic closed $65B at a $965B valuation, shortly before filing its draft S-1 for an IPO. That $965B valuation exceeds the combined value at IPO of every venture-backed US listing from 1995 to 2000 (Benedict Evans). OpenAI is moving toward a public listing of its own. These companies are also generating real revenues today. This is still just the beginning as companies continue to assess which use cases have a product-market fit and which don’t.

Data center companies need and prize lasting partnerships on the energy side with people who think, build and innovate alongside them. We see a wide variety of credible ways to generate value in this buildout and that’s partly what makes it so attractive.

Much remains unknown. All AI questions have one of two answers: “No-one knows”, or “What happened the last time that everything changed?” (Benedict Evans) The system is also more sensitive to small inputs than its momentum suggests. This came to mind on a visit last week to the San Francisco Exploratorium. At one of the exhibits, guests were invited to spin a knob and watch how three interconnected pendulums swung. The sign read: “When you set these three pendulums swinging, the motion of each one affects the others. Tiny differences in how you spin it add up to drastically different results. Scientists call such systems chaotic.” This dynamic is one to navigate but supports the need for partnerships between experienced operators.

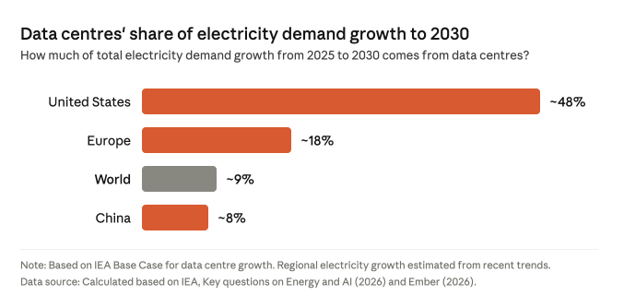

This is a global story but with a strong U.S. tilt, as the share of data centers relative to total electricity demand growth is ≈2.5x the next largest bloc (By The Numbers).

Demand outruns supply

We expect demand for compute to outstrip supply over the coming years, even assuming major efficiency gains. To put the magnitude in perspective: an efficiency gain on the scale of the shift from LSTMs (Long Short-Term Memory) to Transformers, which was roughly a 5x improvement, would still leave the sector compute-constrained (Stanford Frontier System lecture with Amin Vahdat). The supply demand imbalance for power will remain especially tight as 94 gigawatts of coal power plants are set to retire over the next decade (Wood Mackenzie).

A gas build-out

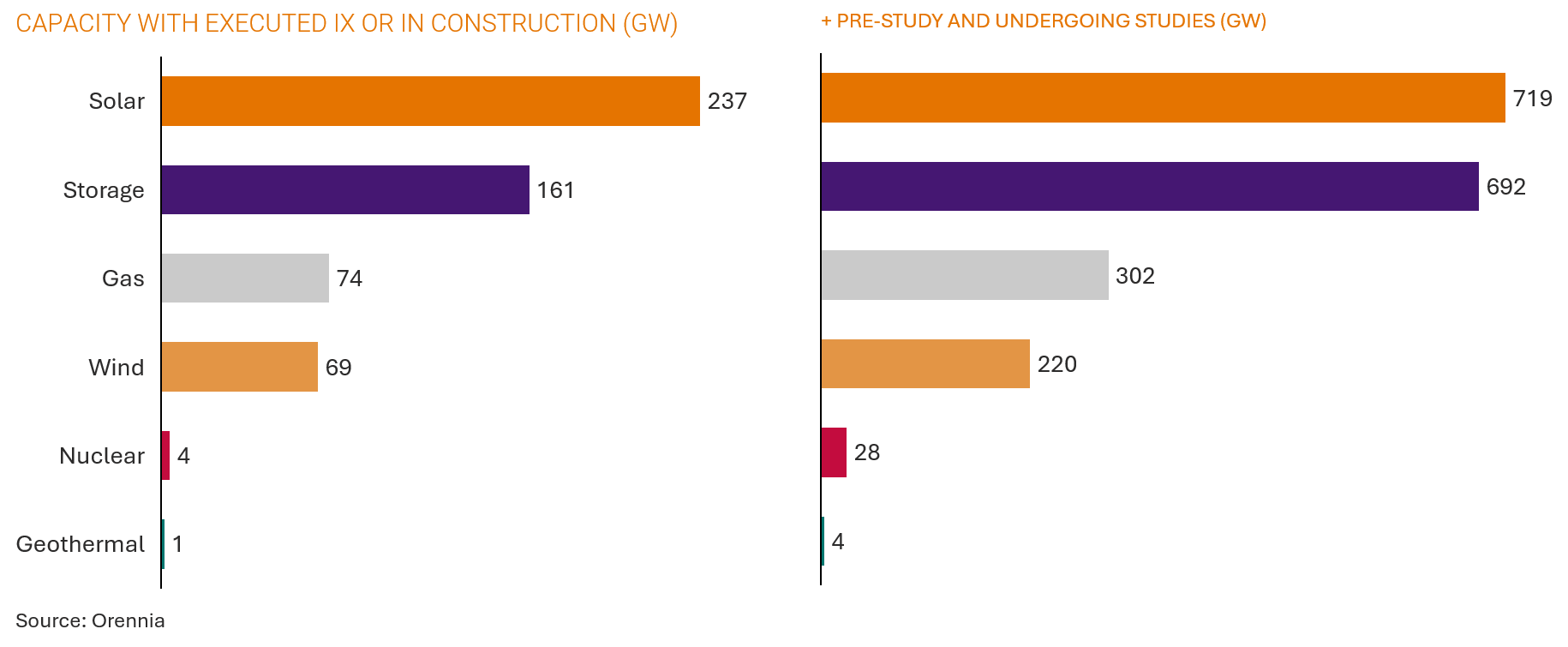

Data center demand is spurring a vast build out of new generation capacity. In Wood Mackenzie’s moderate case, data center demand grows 13% annually which drives 13.2GW of gas additions per year from 2026-35, up from 4GW per year from 2023 to 2025. This time last year, there was only 39GW of natural gas in the late stage IX queue. This has since risen to 74GW.

A clean build-out

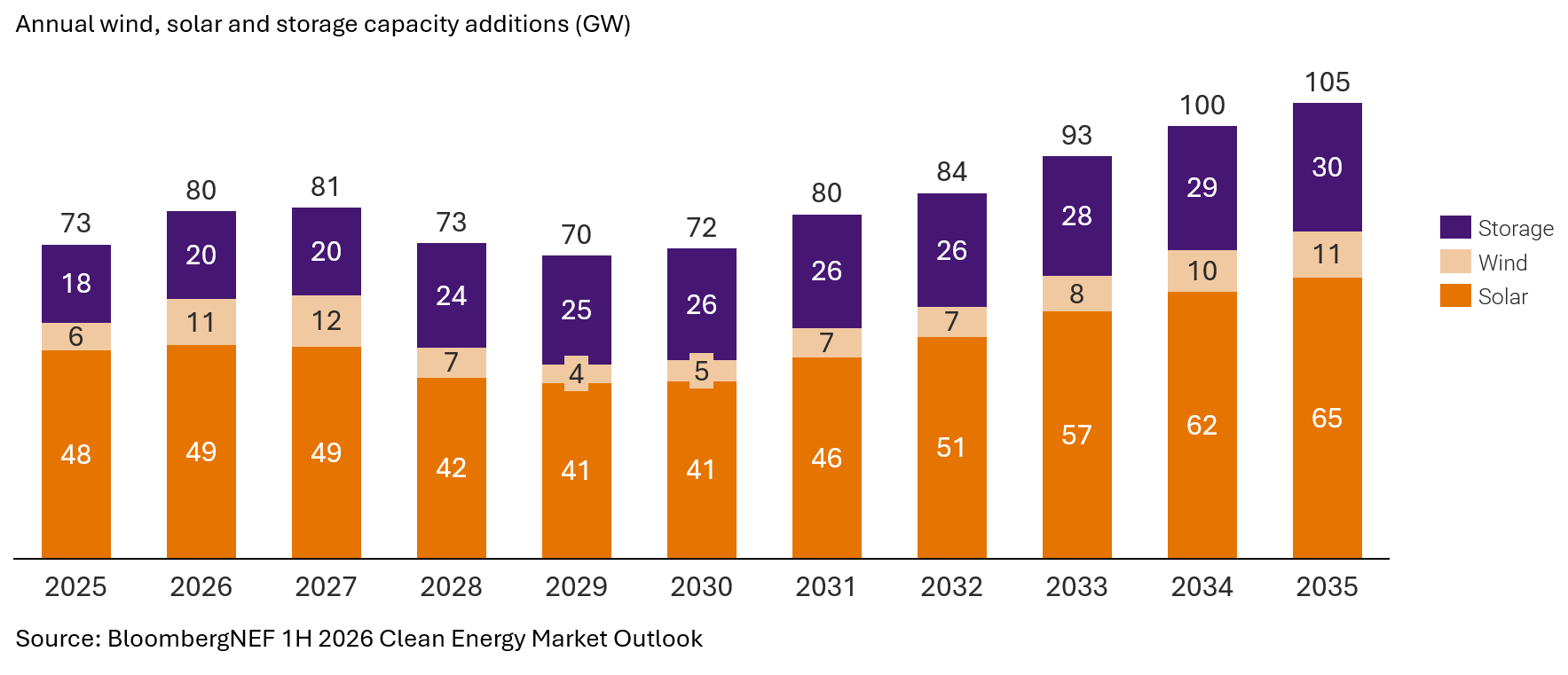

The interconnection queue is also bulging with clean resources. Growing electricity load and generation retirements underpin large and sustained demand for grid-connected clean power, even accounting for a moderate dip in installations from 2028–31, an air pocket left as developers pull projects forward to capture tax credits before they step down (BloombergNEF). There is understandable excitement about clean firm power, evident from the recent IPOs of Fervo (geothermal) and X-energy (nuclear). Battery storage though, is the core enabling technology of this buildout. It makes data centers better neighbours to the grid; it relieves transmission and distribution constraints and opens the door for interruptible load frameworks; it unlocks more clean generation.

Investor appetite

The importance of power within the data center story shows up clearly in recent deal activity. In May alone:

- DigitalBridge agreed to buy ArcLight Capital Partners for up to $1B.

- NextEra announced a $67B tie-up with Dominion Energy

- Fervo had an upsized IPO with strong aftermarket performance ($12.4B market cap, +42% post-IPO) amid interest in clean firm power.

- Not quite in May, but X-energy, a nuclear company, completed its IPO on April 24 raising just over $1B.

- ERock (formerly Enchanted Rock) filed for a NYSE IPO in an effort to take advantage of public-market interest in scalable onsite power and microgrid platforms serving data centers and other large-load customers.

- GridCare raised $64M in a Sutter Hill Ventures-led round that highlighted the growing interest in tools that unlock grid interconnection.

- SB Energy confidentially filed for IPO with reports suggesting a value of ≈$50B.

Small fish, big pond

Rising electricity demand from data centers also squeezes other buyers of electricity. Much of the recent attention has focused on the impact to residential users, but many large non-data center corporates are also grappling with how to quickly and affordably get access to power. This was a common topic during this year’s CEBA event in Seattle, as energy buyers who were once considered large (nationwide retailers, industrials, banks) reckoned with their new status in the procurement stack. These firms are often innovative and may end up even leading the way on many of the interruptible load frameworks we outline later in the piece (C3). On top of this, we are likely underestimating electricity demand from other major sources such as electric vehicles as forecasters overcorrected their medium-term outlooks in the face of the current administration’s hostility to the sector.

The bottlenecks

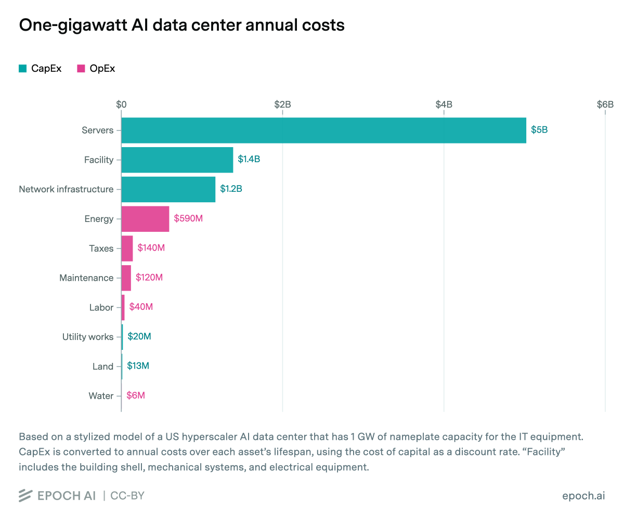

Developments in infrastructure are simultaneously moving at light-speed relative to recent progress within infra, but are positively slovenly relative to demand. This is a well-documented challenge for data center developers since while power may not be the largest dollar cost, it is the gating item for data center revenue. “Power strategy is a way to protect time-to-revenue, tenant SLAs and refresh-cycle economics.” (Epoch)

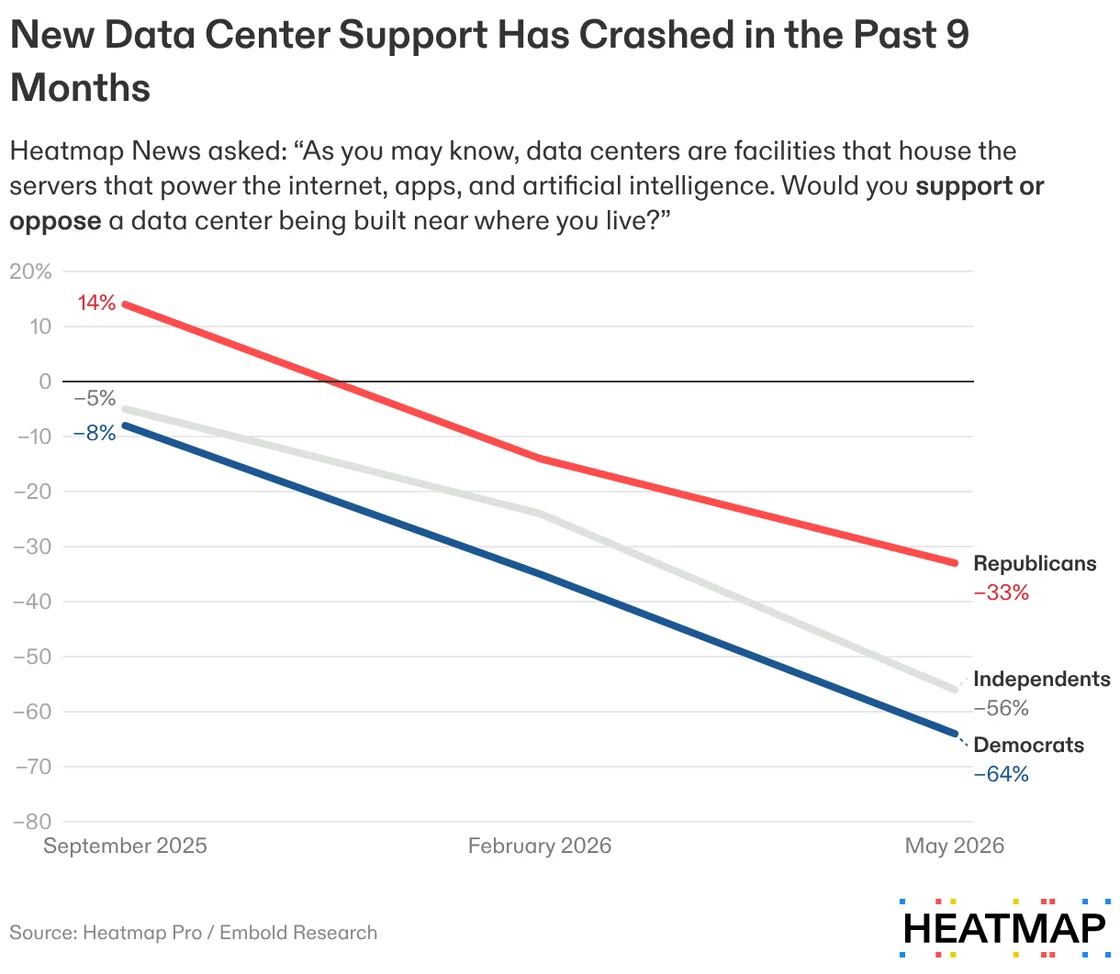

Community opposition to generation, transmission and distribution, and the data centers themselves is another bottleneck. The negative swing in opinion over the last 9 months is striking, and bipartisan (Heatmap).

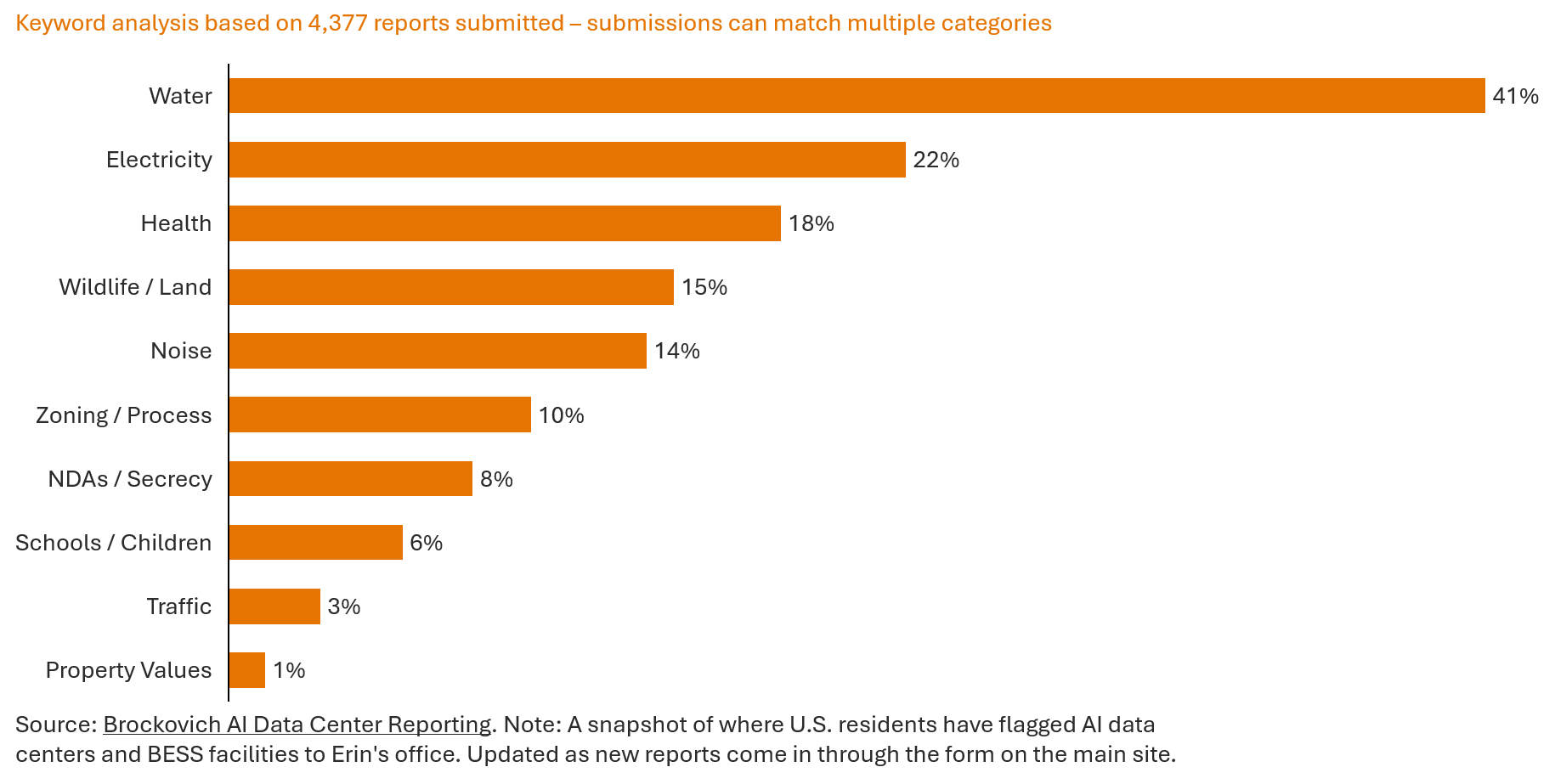

Communities are also worried about a plethora of things, with water usage, electricity / grid and health leading a scoreboard compiled by (Brockovich AI Data Center Reporting).

A narrative shift

The overarching sentiment and the underlying drivers are still forming and there’s still an opportunity to decisively turn the tide here. Effective engagement at the local level, rather than trying to swing national polls, will determine which data centers are built versus those that stall or are cancelled. An Austrian concept to use large statues as transmission towers is one approach but fortunately more is happening (APG, h/t Construction Physics).

As my colleague Jonah Goldman wrote last month:

“Communities that organize with equal seriousness, around what they want from this buildout rather than around whether they want it at all, will end the decade with infrastructure their grandchildren still benefit from. That infrastructure can be clean, affordable, and reliable. Communities that spend the leverage on saying no will get what they always have: whatever is left over after capital sets the terms. Developers that try to undercut productive efforts to build that kind of resilience in communities will end up losing. Both sides need to realize that the relationship can be productive and valuable.”

Hyperscalers and developers are now making a firmly positive, rather than purely defensive, case. Beyond baseline commitments not to shift costs onto other ratepayers such as the Ratepayer Protection Pledge, firms like Google and Microsoft are now demonstrating how data centers can benefit a community rather than simply avoid burdening it: Microsoft Ratepayer Protection Tariff (RPT) in Nevada for instance creates opportunities for large load customers to invest their own capital in the electric system in partnership with their utilities. Translating intentions into tangible change is however no mean feat as Travis Kavulla’s essay on the topic lays out (American Affairs Journal).

Hyperscalers have for some time played a role commercializing clean energy technologies that the rest of industry wasn’t ready for. This continues. In May, Elemental Impact and the four hyperscalers launched the Data Center Innovation Initiative (DCII). The initiative will invest $500,000-$5 million per project in up to 10 technology startups in projects that help pilot new solutions, creating potential pathways for future adoption.

A regulatory shift

Data center growth is also a driver for positive regulatory change. I believe (although other opinions are avaialble) that this will be more catalytic for clean energy adoption than any hard technology breakthrough over the next decade. As we wrote in our Constructive Interference note, data center demand has prompted a long overdue reckoning about our power systems and is driving wholesale changes across the U.S. Before exploring recent developments across PJM, ERCOT and SPP it’s worth remembering the foundations of many of these concepts can be traced back to the start of electricity markets and well before. Insights such as the importance of marginality, of interruptible contracts and priority service and differential reliability require further innovation and new ways of thinking but have a strong foundation in the past (The Power Game).

In May PJM released its conceptual paper on how to drive investment and overcome some of the challenges facing the market. As PJM’s CEO explains, “It is a diagnosis of why the current moment is structurally different to prior periods of tightness, and a framing of the choices – about risk allocation, reliability standards and market architecture – that the region must make explicitly or will make by default.” Of the three high-level pathways PJM proposes to address the challenges, a shift away from capacity to one more focused on energy and ancillary services stands out. Separately, the PJM Interconnection can curtail data centers and other large loads that have backup generation under an emergency order issued by the Department of Energy (Utility Dive). Only large energy consumers with backup generation would be affected. This reinforces a point we’ve made a few times now that the lines between behind-the-meter and front-of-meter are blurring and that there’s no escaping the grid. In a unrelated, relatively small but indicative sign of the potential for behind-the-meter resources to serve wider purposes, Google and Voltus agreed a three-year deal to unlock up to 100MW of new electricity capacity annually in the region under a Bring Your Own Capacity Framework (Voltus).

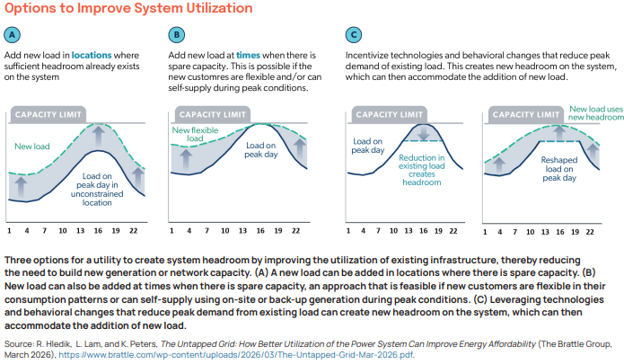

Elsewhere, on May 19 ERCOT’s Technical Advisory Committee (TAC) approved PGRR145, the planning guide revision that establishes the framework for Batch Zero (Texas Energy and Power Newsletter). The framework includes a design change that allows nodal Provisional Controllable Loads (PCLR) to exchange curtailment risk (to use the headroom available today) for earlier grid power while those loads await firm upgrades (Luminary Strategies). ESIG’s Impacts of Large Loads on Electricity Prices (ESIG) paper has a simplified visual on the various ways you can improve system utilization.

The TAC also approved approximately $6.5B in transmission projects in a sign that data centers can encourage both the better use of the grid we have, and can provide the resources and rationale to expand and modernize it. For more background on the latest in ERCOT, Eric Goff’s interview is a good primer as he breaks down what it means to serve “infinite load”.

Alongside ERCOT, SPP is the ISO furthest along in establishing novel pathways that could accelerate large load connections. FERC approved SPP’s HILL and High Impact Large Load Generation Assessment (HILLGA) framework agreement earlier in the year and recent task force decisions show that the details are moving in the right direction. The Consolidated Planning Process Task Force (CPPTF) for instance recently granted relief from the five-year requirement to transition through the regular Generation Interconnection (GI) process (AESL).

As powerful as these reforms could be, they will still take time, which tends to be in short supply in data center circles. Natural gas as a bridge to a grid interconnection is often the best solution here. Depending on the technology, it can then be relocated to another site earlier in development; or it can remain on site but as backup or perhaps as the enabling technology in an interruptible load configuration.

The builders

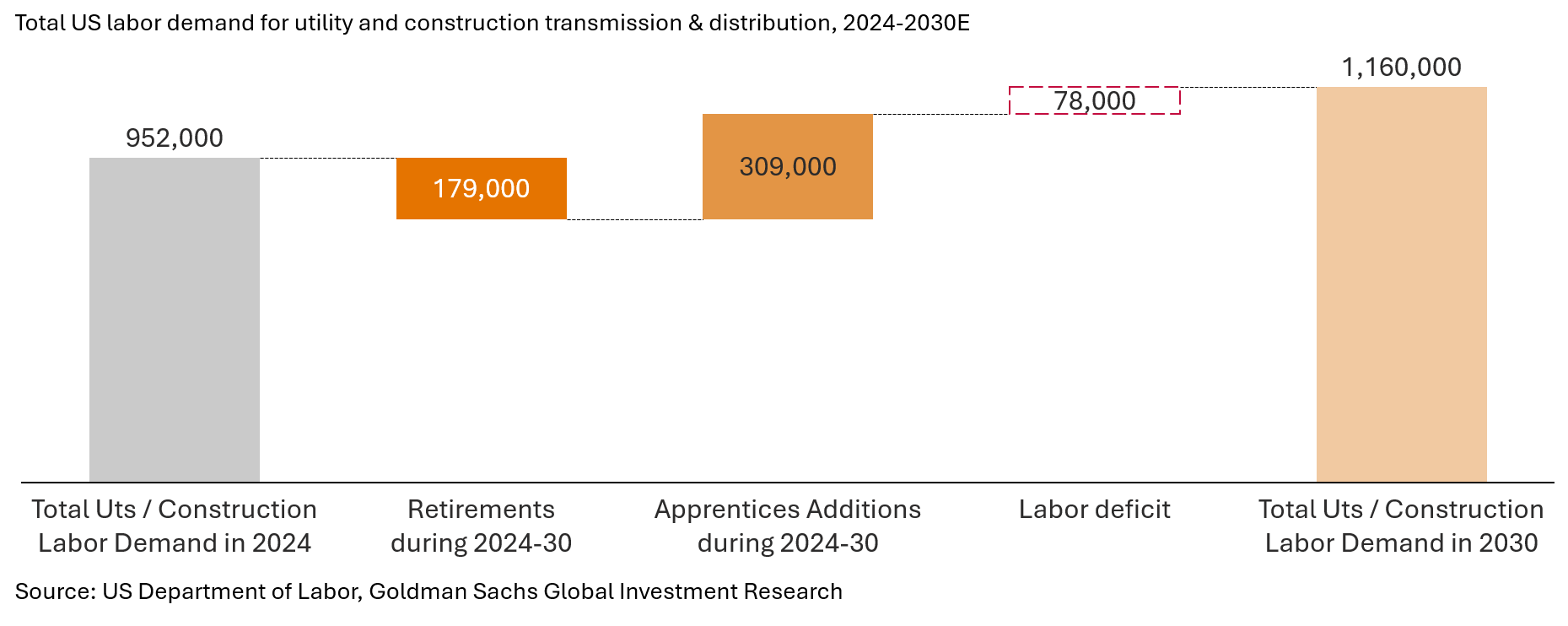

Market reform and bridge generation address how load reaches power but neither addresses who builds it. Labor shortages relating to data centers are increasingly prominent: The Associated Builders and Contractors trade group estimates that the construction industry is short 439,000 workers, mostly among skilled workers (WSJ). This is likely to get worse before it gets better. Goldman Sachs estimates ≈300k manufacturing, construction and operations jobs will be needed to meet power demand by 2030; with an additional ≈200k jobs needed for transmission and distribution. Assuming all energy-related apprenticeships are deployed to T&D, you still end up with a 78k labor gap in T&D. As with the community angle, a nationwide fix is unlikely here and instead availability of labor will be determined by proving yourself as a serious counterparty and thus encouraging workforce allocations your way.

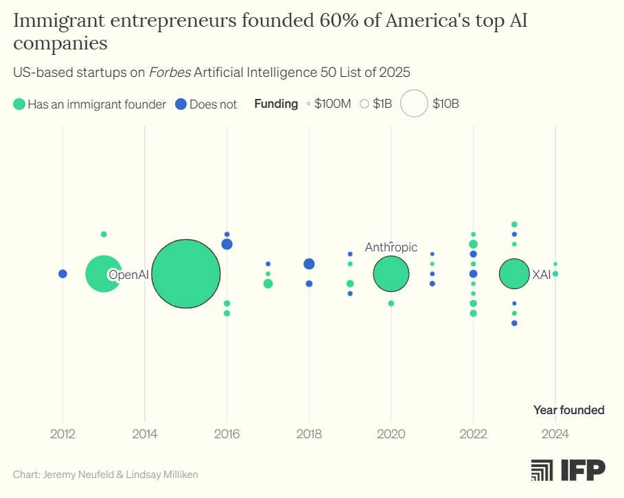

It’s not just construction workers and electricians who may end up in short supply. Last month, the administration called for most foreigners seeking permanent residence to leave the US and apply at American consulates abroad (Bloomberg). The administration has since rowed back on aspects of the announcement but confusion reigns. So, just a reminder that all the biggest U.S. AI companies, and more than half of the top 50 were founded by immigrants (IFP, Noahpinion)

What we're reading

The Triumph of the Average (Market Depth). What is it that links the uniformity of cars, architecture, interior design and a host of other things in the modern economy?

A remarkable story about how Fisker Ocean (a car) owners “organized, reverse-engineered their vehicles’ proprietary software, hacked into CAN bus networks, built open-source tools on GitHub, and effectively stood up a volunteer-run open-sourced car company from the ashes of Fisker.” (Electrek)

The Distributed Future (Texas Energy and Power Newsletter) makes the case that breakthroughs relating to the geographic decentralization of training and Sparse AI could, alongside a shift to more inference applications, undermine the need for gigawatt-scale data centers. This is not yet proven in my mind and I’d welcome a chat with anyone who wants to discuss.

Nick Chaset at Octopus Energy has put together a running google doc that summarizes utility 10Ks to help track the sentiment and priorities of U.S. infrastructure execs. (link)

The Evolution of Corporate Energy Procurement for Technology Loads (Arushi Sharma Frank)

Inside the 800V DC Revolution makes the case that the architectural shift is inevitable since it furthers the tokens per watt (Semi-Analysis). A blueprint on 800V DC from Heron Power.

More newsletters

June 2026 Newsletter - AGM Edition

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

Read moreApril 2026 Newsletter

After four years, PJM opened back up its generation interconnection queue. Gas is now the dominant technology in the queue compared to solar back in 2022.

Read moreMarch 2026 Newsletter

Just over four years after the "ChatGPT moment", February 2026 marked a new inflection point for how many of my peers and I use AI. The constraints switched from model limitations (both perceived and real) and perhaps a lack of creativity and prioritization, to token and inference constraints: "Rate Limit Exceeded", "A bit longer, thanks for your patience." Powering a data center now requires simultaneous execution across three domains that each demand deep, specialized expertise: the grid and interconnection, on-site generation, and policy and regulation. And while AI has come in strides, the limits to scaling compute quickly are intransigent. They are physical, geographic, and increasingly personal.

Read more