By the numbers

In April AllBirds became an AI company, Fermi America ousted its CEO and co-founder, and a San Francisco homeowner listed his home but only for Anthropic equity (TechCrunch). This month we explore what happens when the data center buildout meets strengthening headwinds, and why firms that properly engage with communities, and take advantage of markets that institutionalize flexibility will be the ones to deliver megawatts.

Data center opposition

Public sentiment is shifting. A November poll of 1,000 US respondents found that people were twice as worried about data centers’ effects on local quality of life as they were about energy costs, though two-thirds still expect a nearby facility to drive up local electricity prices (Axios). In some communities, opposition has turned violent (Heatmap, The Register).

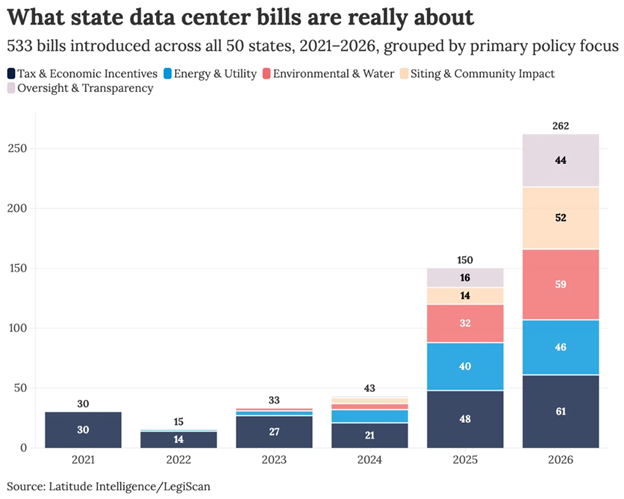

That sentiment is translating into policy. Latitude Intelligence tracked 533 state data center bills introduced across all 50 states from 2021 through today. The most telling finding isn’t the volume — which has increased more than eightfold — but the mix. Tax and economic incentive bills still lead the count, but energy and utility regulation, environmental and water requirements, siting restrictions, and oversight mandates now make up more than three-quarters of all activity. In 2021, they were barely a rounding error. In the most extreme cases, legislatures are reaching for outright bans: Maine Gov. Janet Mills vetoed the bill that would have made her state the first to temporarily ban new data center development, but 12 other states are considering legislative moratoriums on construction (Energy Central, Moratorium Live Tracker).

Demand materializes

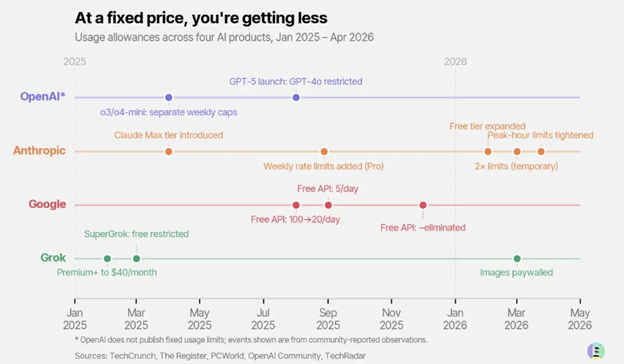

Despite rising opposition, demand for AI products in the US is soaring. This is forcing each of the main AI platforms to throttle usage by introducing more tiers and stricter limits (Exponential View).

Progress in ERCOT, but more to come

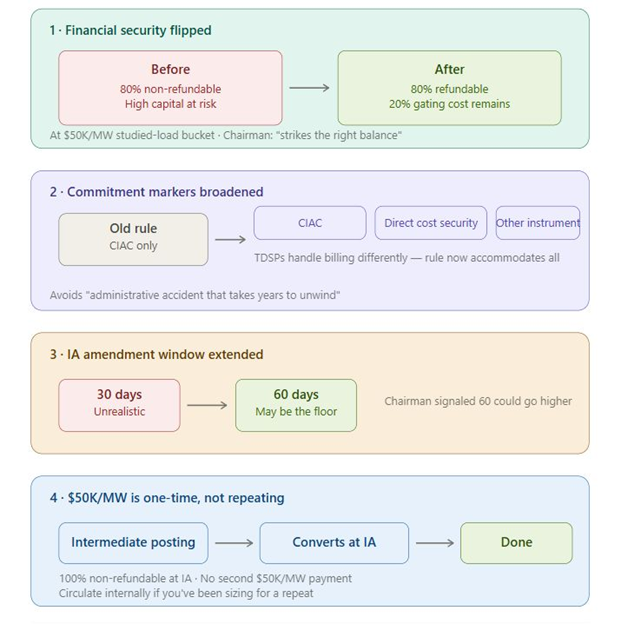

The ERCOT large load queue topped 410GW in April, though at this point the figure says more about the chasm between requests and reality than about actual demand (ERCOT). Recent regulatory developments are working to close that gap. The situation remains fluid, but outcomes from a recent Public Utility Commission of Texas Open Meeting show meaningful progress. Among the key changes: the financial security structure has been revamped, commitment markers are no longer limited to Contribution in Aid of Construction (CIAC) payments, the IA amendment window is expanding from 30 to 60 days, and the $50K/MW financial security requirement is now a one-time obligation (Zero Emission Grid).

The approach to flexibility in ERCOT, as we laid out last month, remains up in the air. Data center flexibility is real, valuable, and heterogeneous, but institutionally fragile. Technical capability does not automatically translate into system value, and whether institutions can bridge that gap is the central policy question (The Knowledge Problem). In ERCOT, that question comes down to how Provisional Controllable Load Resources are treated. For a strong primer on what’s at stake, see Arushi Sharma Frank’s piece here. In short, even large loads that make it into Batch Zero may not receive full capacity until 2033. If the rules are appropriately updated, those willing to accept conditional capacity could instead see projects come online as early as 2028.

PJM opens its doors

The DOE had given FERC an April 30 deadline to finalize a rule on large-load interconnection. FERC missed it, instead issuing an “Order Regarding Intent to Act” on April 16 that pushes the timeline to end of June. This was perhaps a good thing. As Halcyon aptly put it “A rule that affects trillions of dollars of infrastructure investment, has never been previously federally regulated, and has been hotly contested by nearly every major stakeholder group should take longer than six months.”

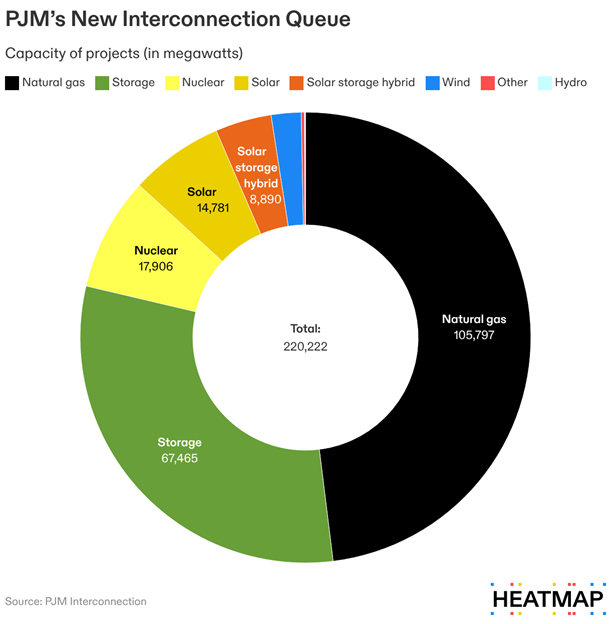

Where FERC did act was on PJM’s interconnection study process, partly approving the latest proposed changes while rejecting tariff provisions governing co-located generating facilities (Utility Dive). Meanwhile, PJM reopened the generator interconnection queue it closed in 2022 to overhaul its study process — and the composition tells its own story. The old queue was dominated by solar; the new one is mostly gas (Heatmap).

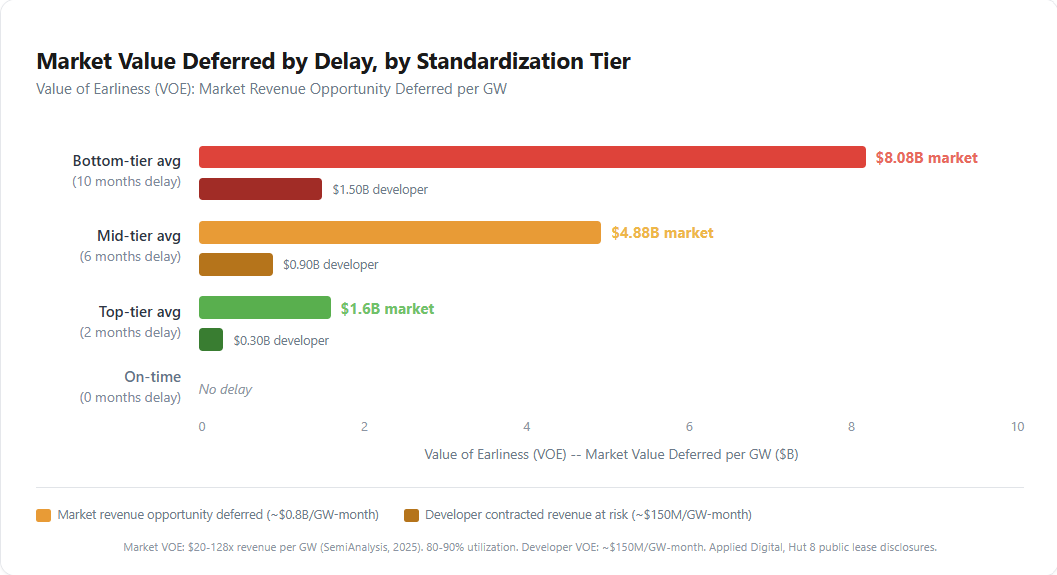

Occam’s Edge

Community and regulatory opposition aren’t the only reasons projects get delayed. Even those that clear the political hurdles face significant execution risk depending on how they’re designed, permitted, and procured. A new whitepaper from Occam’s Edge analyzed 18 islanded power projects — spanning data center microgrids, LNG power islands, and mining hybrids — and found that projects scoring highest on design standardization averaged just 2 months of delay, compared to 10 months for the lowest-scoring projects. The whitepaper estimates each GW-month of delay defers roughly $0.7-0.9 billion of market revenue opportunity.

Operational awareness

The challenges don’t stop once a data center is up and running. The North American Electric Reliability Corp. is in the final stages of preparing a Level 3 essential actions alert related to large computational loads unexpectedly disconnecting from the grid (Utility Dive). The alert, due to be published on May 4, will direct transmission owners, reliability coordinators, and balancing authorities to take a set of essential actions, including changes to the modeling, study, monitoring, and commissioning of large loads. While all eyes are on speed-to-power for now, expect the focus to shift toward ensuring data centers are reliably operated once they’re on the grid.

What we're reading

Sibling Squabble (On.Energy). The gaping disconnect between oil and gas analysts, and power analysts on the outlook for US gas burn.

Lobster boil (h/t Crazy Stupid Tech). An encomium to OpenClaw.

Winning in the Infratech Era (Zero Infinity Partners). “Software ate the world. Now infrastructure is eating the venture world. This is not a reversal. It is the next turn of the cycle – and it is the way innovation has always worked.

Open Grid Works. A free interactive tool to visualize the grid. Courtesy of Brian Bartholomew. Separately, open source power flow tool (Distill)

The Grid (Stepchange). A four hour listen, or see the transcript here.

Shale’s next surge (McKinsey). The piece argues that scale and innovation will sustain the industry despite the depletion of Tier 1 drilling locations.

Selling the Electricity No One is Using (The Money Stuff). A wonderfully droll explainer on “the largest and most brazen frauds in the history of the Federal Energy Regulatory Commission.”

Electrostates v. petrostates. Clarifying a tricky distinction. (ChartBook). Handle these terms with care.

Apple at 50 (The FT). This sits in the other interests category but is a fascinating read about the role Japanese industry and Chinese manufacturing prowess played in the tech giant’s success.

How America Can Put Data Centers in Service of Reindustrialization (Promarket). A demand that data center investments be used to power reindustrialization efforts.

More newsletters

July 2026 Newsletter

The data center industry continues to surprise both in terms of how quickly the status quo can change, and how resolutely many stakeholders assume the current status quo is now fixed. Eighteen months ago, fully islanded projects were more speculative than real, hyperscalers’ decarbonization bona fides were still mostly intact, and permitting was largely a formality if you followed process. Each looked settled right up until it wasn't, and expecting stability now is a curious leap.

Read moreJune 2026 Newsletter - AGM Edition

We hope to see many of you at our AGM this coming week, but in the meantime, here is the latest on what’s happening at the nexus of AI demand and energy. Both Generate and this newsletter have come a long way since our first post in September 2024. Generate is now focused on what our CEO David Crane recently described as “the single defining factor in the future of our industry – AI demand is accelerating faster than the infrastructure needed to support it.”

Read moreApril 2026 Newsletter

After four years, PJM opened back up its generation interconnection queue. Gas is now the dominant technology in the queue compared to solar back in 2022.

Read more